The Payvider Promise Doesn't Add Up: What Healthcare CFOs Need to Know Before the Model Reshapes Your Market

Integration looked like the answer. The financial reality is more complicated than the headline.

More than half of all Medicare enrollees are now in a Medicare Advantage plan. That single fact is quietly restructuring every contract, care model, and capital decision in your market. The payvider model, which promises to solve the friction between payer and provider by merging them into one organization, is the industry's current answer to that pressure. Before you buy the pitch, there are some things you should know about how it actually works once the press release is filed.

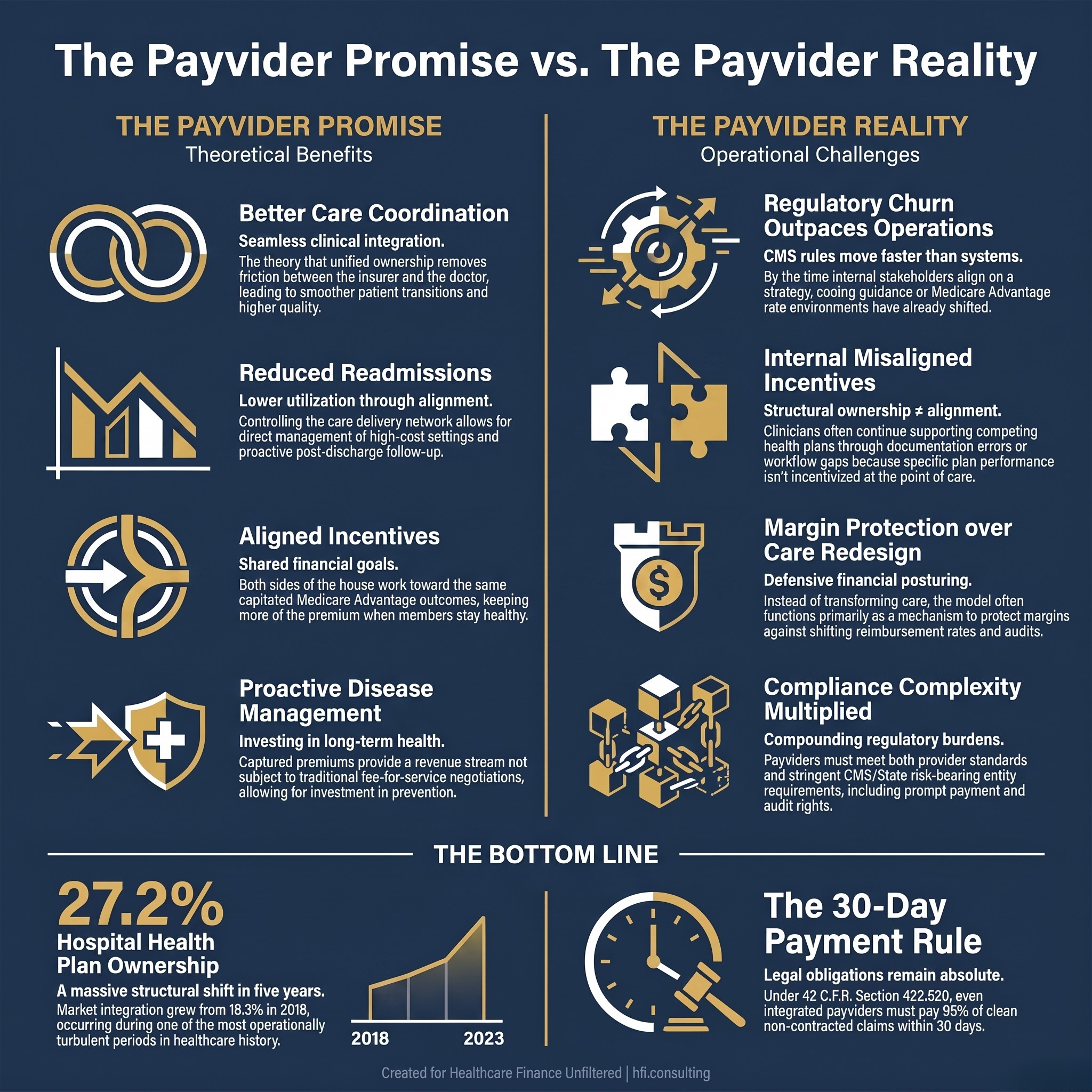

Side-by-side comparison of payvider promises versus operational realities for healthcare CFOs evaluating payer-provider integration models.

What a Payvider Actually Is (And Why the Definition Is Already Slipping)

The term "payvider" is a portmanteau of payer and provider. It refers to organizations that combine insurance and care delivery under one roof. Think Kaiser Permanente, UPMC, Geisinger, and Intermountain Health on the health system side. Think UnitedHealth Group's Optum network, Humana's CenterWell, CVS Health's Oak Street Health, and Elevance Health's Carelon on the insurer side.

The concept predates the term. Kaiser was doing this in 1945. But the term itself only gained real traction in the last decade, and even now, as a recent Becker's Hospital Review analysis noted, the definition has become so elastic that many healthcare organizations could technically qualify. That definitional murkiness matters for CFOs because loose language in a market trend often signals loose thinking in the strategy rooms where capital decisions get made.

The payvider model generally takes three forms: provider-sponsored health plans (health systems that launch their own insurance products), insurer-owned care delivery (large payers that employ physicians directly), and joint ventures between the two. The regulatory obligations attached to each form vary significantly, and that variation has direct financial consequences.

According to a May JAMA letter, the percentage of U.S. hospitals owning or jointly owning a health plan increased from 18.3% in 2018 to 27.2% in 2023. That is a meaningful structural shift in a five-year window. It is also a window that included the COVID-19 pandemic, multiple Medicare Advantage rate cycles, and the beginning of the prior authorization reform era. The organizations that launched or expanded payvider models during that period were doing so into one of the most operationally turbulent periods in recent healthcare history.

The Financial Logic That Made This Seem Like a Good Idea

The core financial thesis behind payvider integration is straightforward. Under a capitated Medicare Advantage model, you receive a fixed monthly payment per member. If your members stay healthy, use fewer services, and avoid high-cost settings, you keep more of the premium. If you control both the insurance function and the care delivery function, you can theoretically align every incentive toward that outcome.

For payer CFOs, the appeal is obvious: owning the care delivery network means you can manage utilization directly rather than relying on prior authorization and claims adjudication to hold the line. For provider CFOs, the appeal is equally clear: capturing the premium dollar gives you a revenue stream that is not subject to fee-for-service rate negotiations, denial rates, or the endless cycle of underpayment disputes.

This logic held up well in the boardroom. It has proven considerably harder to execute on the ground.

For a deeper look at how payer-side financial incentives have reshaped provider contracting environments, the article What Payer CEO Pay Ratios Tell Healthcare CFOs About the Claims Environment They're Actually Navigating breaks down what the compensation data actually signals about plan behavior.

Where the Operational Reality Diverges from the Financial Model

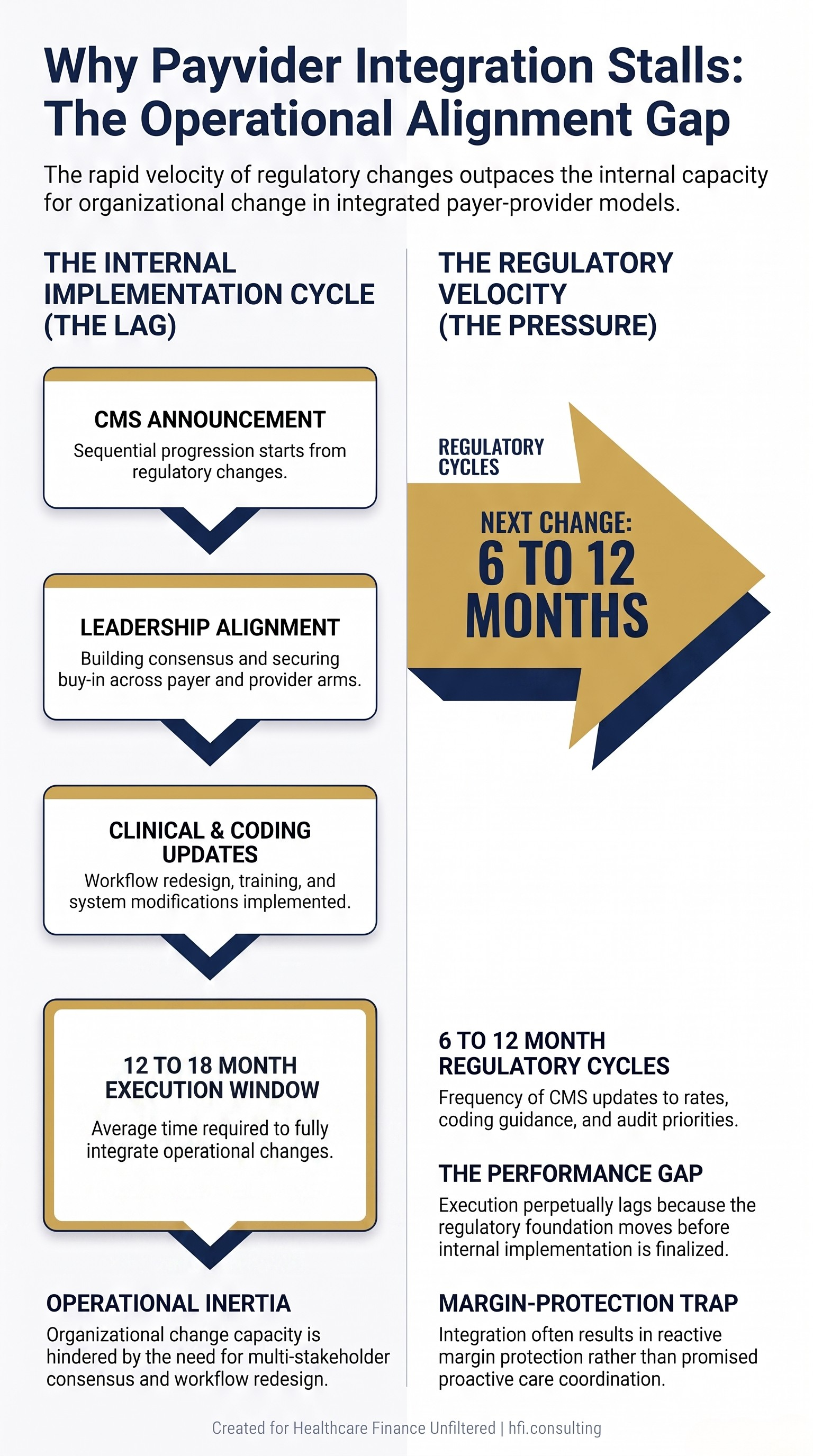

Here is what the integration thesis tends to underestimate: the speed at which CMS changes the rules relative to the speed at which large organizations can change their operations.

From my time in payer operations, the payvider model did not primarily deliver better care coordination or meaningfully reduced costs. What it delivered, more often, was a margin-protection mechanism. And the reason it fell short of the care redesign promise was not bad intentions. It was that the regulatory environment moved faster than the organization could align. By the time internal stakeholders agreed on what actions were needed, the rate environment had shifted, the coding guidance had changed, or a new audit priority had emerged. The integration promise kept getting deferred because the operational foundation kept moving.

This observation is consistent with what industry analysts are now documenting more publicly. Allison Rizer, chief growth and innovation officer at ATI Advisory, has noted that many smaller payviders struggle because employed clinicians and staff may continue supporting competing health plans. At smaller organizations, physicians may complete coding and documentation activities that benefit competing Medicare Advantage plans while overlooking similar efforts for their own organization's health plan because incentives are not aligned. Simply owning both a health plan and a provider organization does not create meaningful integration unless incentives, operations, and organizational goals are coordinated.

That last sentence is worth reading twice if you are currently evaluating a payvider strategy or a joint venture with a payvider.

Flow diagram showing the misalignment between Medicare Advantage regulatory change timelines and payvider operational implementation cycles.

The Regulatory Obligations Most CFOs Underestimate

Whether or not a payvider holds a formal insurance license, the regulatory obligations that attach to assuming financial risk for patient populations are substantial. This is a point that the provider-friendly branding of many payvider arrangements tends to obscure.

When a payvider operates a licensed health plan or contracts with CMS as a Medicare Advantage organization, it must be organized and licensed by a state as a risk-bearing entity and certified by CMS under 42 C.F.R. Section 422.2. That is the same standard that applies to every other MA plan, regardless of whether the organization started as a hospital system or an insurer.

For provider organizations that accept capitated or risk-based payments from payviders, the compliance obligation does not disappear just because another entity holds the MA contract. Physician groups, IPAs, and ACOs that accept capitated payments are first-tier or downstream entities under 42 C.F.R. Part 422. The payvider retains ultimate CMS compliance responsibility, but federal law requires key protections to flow down to all contracted entities, including audit rights, enrollee protections, and prompt payment obligations.

California has gone further, now requiring any entity assuming global risk for both institutional and professional services to obtain a Knox-Keene health plan license. That change was prompted by risk-bearing organization insolvencies that left providers unpaid. That is not a hypothetical risk. It is a documented one.

For provider CFOs who are downstream entities in a payvider arrangement, the article The Denial Loop Is Breaking Healthcare: What Both Sides Are Paying and What Has to Change covers the claims environment context that makes these contract terms so consequential.

The Incentive Misalignment Problem That Doesn't Get Fixed by Org Charts

One of the most persistent misconceptions about payvider integration is that structural ownership resolves incentive misalignment. It does not.

The incentive misalignment in a payvider is not primarily a governance problem. It is an operational problem. When a clinician employed by a payvider sees patients who are enrolled in three different MA plans, that clinician's documentation and coding behavior affects revenue across all three plans. Without explicit workflow design, real-time data feedback, and direct financial accountability tied to the payvider's own plan performance, the clinician has no practical reason to prioritize one plan's risk adjustment accuracy over another's.

In my work consulting on contribution margin analysis across health system service lines, I have seen a version of this same dynamic play out in how organizations track payer-specific performance. The data exists. The accountability structure to act on it often does not. Payvider integration adds a layer of complexity to that accountability gap without automatically resolving it.

The financial consequence is real. Missed coding and documentation opportunities in risk adjustment translate directly to lower risk adjustment factor scores, which translate to lower per-member premium payments. For an organization that made a capital commitment to a payvider model on the premise that it would optimize those scores, the gap between projection and performance can be significant.

The article Medicare Advantage 2026: The Payer CFO Playbook for the Most Challenging Year in Plan History covers the rate environment pressures that make risk adjustment accuracy a make-or-break financial variable in the current MA cycle.

What CFOs on Both Sides of This Should Actually Be Planning For

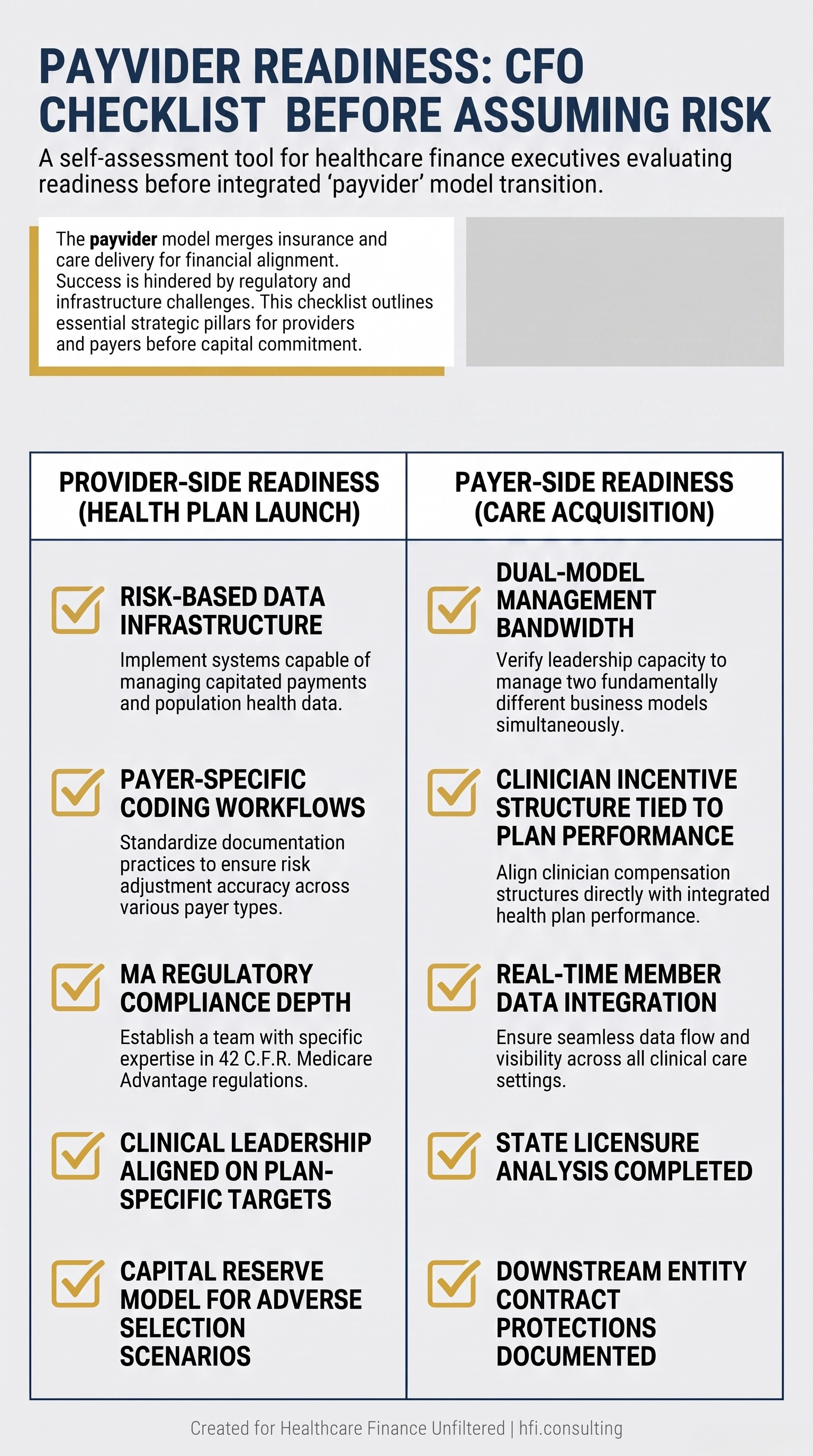

The payvider model is not going away. Payer-provider integration is likely to continue growing, particularly in Medicare Advantage and Medicaid managed care, where some states encourage or require provider-owned health plans. But the organizations that will make it work financially are not the ones that launch with the most ambitious press releases. They are the ones that do the operational work before the capital commitment.

For provider CFOs evaluating whether to launch a health plan or enter a risk-bearing arrangement with a payvider, the financial planning questions that matter most are not about the premium revenue potential. They are about the operational infrastructure required to capture it: the data systems, the coding workflows, the clinical performance feedback loops, and the compliance infrastructure that must be in place before the risk dollars can be realized.

For payer CFOs evaluating whether to acquire or develop care delivery assets, the question is whether the organization has the management bandwidth and operational discipline to coordinate two fundamentally different business models under one financial accountability structure. The integration does not simplify operations. It multiplies the variables that leadership must manage simultaneously.

Payvider readiness checklist for provider CFOs evaluating health plan launch and payer CFOs evaluating care delivery acquisition decisions.

The Contracting Rights That Often Get Overlooked

One financial risk that tends to get underweighted in payvider strategy discussions is the downstream contracting position of providers who are not part of the integrated structure. As large payviders expand their footprint, smaller and independent providers face growing challenges navigating negotiations, reimbursement pressures, and evolving expectations around value-based care.

Provider-friendly branding does not insulate a payvider from the legal and regulatory obligations that attach to assuming financial risk for patient care. Providers contracting with payviders have enforceable rights regardless of the ownership structure. If a payvider withholds capitation, miscalculates shared savings, over-expenses costs, or underpays claims, that is a breach of contract, regardless of the payvider's provider identity.

For Medicare Advantage arrangements, 42 C.F.R. Section 422.520 requires payment of 95% of clean non-contracted claims within 30 days. State remedies, including prompt payment statutes and unfair claims practices acts, provide additional enforcement tools. In Florida, the Statewide Provider and Health Plan Claim Dispute Resolution Program offers binding arbitration for underpayment and denial disputes, which can be a lower-cost alternative to litigation.

This is not a theoretical risk for CFOs to file away. It is an active contracting issue as payvider market share expands and independent providers find themselves negotiating with organizations that are also their competitors in care delivery.

If your organization is navigating a payvider contract, a risk-bearing arrangement, or evaluating whether to launch a provider-sponsored plan, HFI Consulting works with health system and payer finance teams on the financial modeling, contribution margin analysis, and payer strategy questions that sit underneath these decisions. You can reach out directly at hfi.consulting

The Bottom Line for Healthcare CFOs

The payvider model made a promise: integrate payer and provider, align the incentives, and the financial and clinical outcomes will follow. The promise was not wrong. The timeline was.

The organizations that have made payvider integration work, Kaiser Permanente and a small number of others, built their operational infrastructure over decades. They did not bolt insurance operations onto provider organizations and expect the incentives to align themselves. They built the data systems, the clinical accountability structures, and the management discipline that the model requires before they scaled it.

The current wave of payvider expansion is moving faster than any of those precedents. The regulatory environment is changing faster still. For CFOs on both sides of this model, the financial planning imperative is to separate the structural premise, which has real merit, from the operational assumption, which requires proof of concept before capital commitment.

"At the end of the day, you have to think like an insurer," as one industry advisor recently put it. That is exactly right. And thinking like an insurer means planning for adverse scenarios, not just the margin optimization case.

The payvider thesis is not broken. But it is not a shortcut, either.

For a deeper framework on how provider-sponsored plans have approached the financial planning challenges of integration, the article Provider-Sponsored Health Plans in 2026: The CFO's Financial Playbook for Making Payviders Work is the companion read to this one.

P.S. I'd like to hear from CFOs who have been through this from either side: did the payvider model in your market deliver on the integration promise, or did the operational reality look different from the financial projection? Hit reply and tell me what you actually saw.