Provider-Sponsored Health Plans in 2026: The CFO's Financial Playbook for Making Payviders Work

Why some health systems are winning the payvider bet and others are cutting their losses fast.

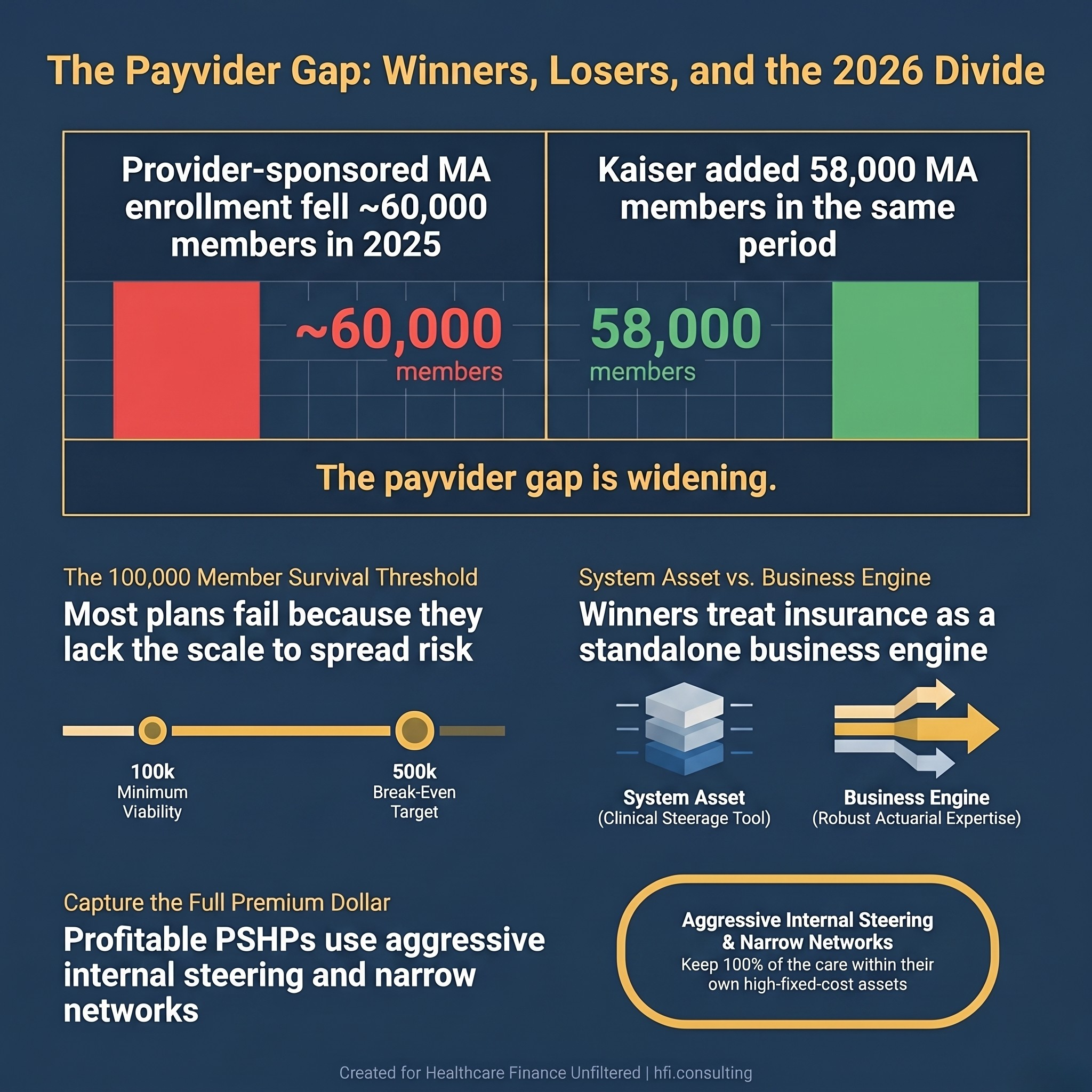

Provider-sponsored Medicare Advantage enrollment dropped by nearly 60,000 members in 2025, while multiple health systems sold or shut down their plans entirely. At the same time, Kaiser Permanente added 58,000 MA members and UPMC's insurance division continues to fund system-wide expansion. The payvider model is not failing. But it is separating organizations that understood what they were getting into from those that did not.

Split stat card showing 60,000 member decline in provider-sponsored MA plans versus 58,000 member gain at Kaiser Permanente in 2025.

What "Payvider" Actually Means for Your Balance Sheet

The term "payvider" gets used loosely, and the imprecision creates real strategic confusion. A payvider is any entity blending payer and provider functions. A provider-sponsored health plan (PSHP) is a specific subset: a health insurance company that is fully or majority-owned by a hospital or health system.

The distinction matters financially. An IDN that participates in value-based contracts is not a PSHP. A health system that launches a capitated Medicare Advantage plan and carries the actuarial risk on its own balance sheet is. That insurance risk sits in a different regulatory, capital, and operational structure than your clinical operations.

Understanding which model you are actually running determines which performance metrics matter, which governance structures apply, and how much capital you need to hold in reserve before a bad claims quarter creates a liquidity problem.

The Current Market: Who Is Exiting and Why

Several significant exits and divestitures have occurred in the past 18 months. Indiana University Health Plan sold to Elevance (Anthem Blue Cross Blue Shield) in January 2025. ProMedica's Paramount Health sold to Medical Mutual of Ohio in May 2024. Carle Health's Health Alliance is winding down individual and employer group plans, retaining only Medicare Advantage. Michigan Medicine announced it will discontinue its health plan at the end of 2025.

These are not small organizations making rookie mistakes. They are large, sophisticated health systems that concluded the capital requirements, operational complexity, and competitive pressure of running a standalone insurance entity outweighed the strategic benefits. If you want the full picture of what the CY 2027 Medicare Advantage Final Rule adds to the pressure on these decisions, that analysis is worth reviewing alongside this one.

According to research from the Advisory Board, the most common failure pattern is a mismatch between expectations and investment. Leadership expects insurance profits but only invests at health-system-asset levels. The resulting undercapitalized, underoperationalized plan cannot compete with national insurers who carry massive actuarial data sets, integrated pharmacy benefit managers, and established broker networks.

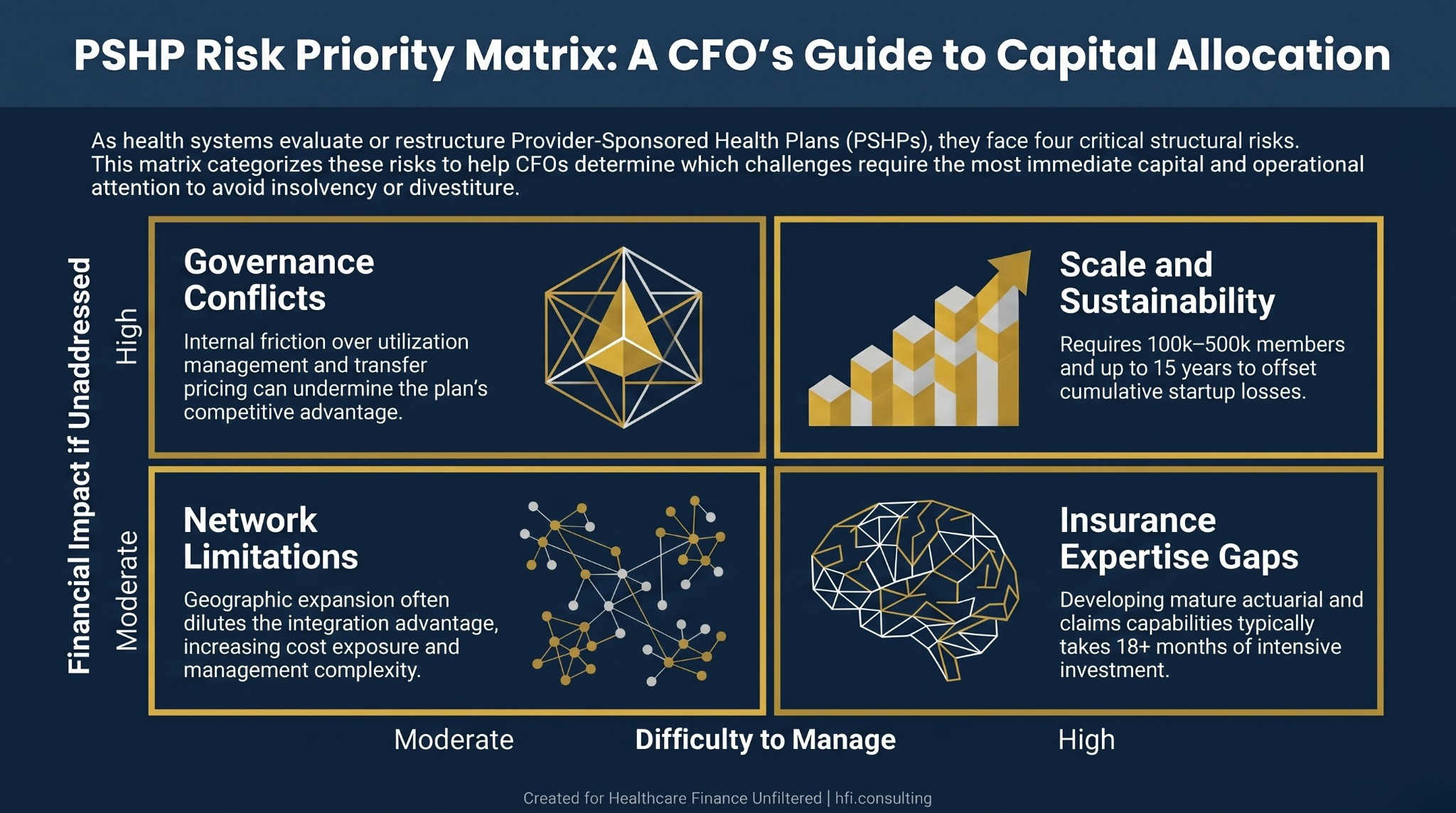

The Four Structural Risks Finance Leaders Must Quantify

Scale and financial sustainability. Industry guidance consistently points to 100,000 members as a minimum viable threshold for spreading risk and overhead, with 500,000 as a more reliable break-even target. Most PSHPs do not come close. Sentara Healthcare's Optima Health Plan required 15 years to offset its cumulative losses from the first decade of operation. That timeline is not an outlier. Newly launched PSHPs routinely report operating losses for the first five years. Any pro forma that projects profitability inside year three needs a fundamental actuarial review.

Insurance expertise gaps. Running a health insurance company requires actuarial pricing, claims administration, risk adjustment, utilization management, network contracting, member services, and sales infrastructure. Most hospital finance teams have limited experience in any of these functions. Setting premiums too low creates insolvency risk. Adverse risk selection, where sicker patients are drawn to the plan due to the health system's clinical reputation, can accelerate that exposure. The Advisory Board estimates that developing mature operational capabilities for key PSHP functions takes 18 months or more.

Governance conflicts between the plan and the provider. This is the internal tension that operational frameworks rarely surface clearly enough. The health plan's financial model depends on managing utilization, which means prior authorizations, care steering, and benefit design decisions that the clinical side may resist as threats to revenue and autonomy. Internal pricing negotiations between the plan and the health system create additional friction. If the plan must pay market-rate transfer pricing to the hospital it owns, the competitive premium advantage disappears.

Network limitations tied to expansion. PSHPs typically start with narrow networks anchored to the owning system. That network depth is a competitive differentiator in the local market. As the plan attempts to grow geographically or increase employer group enrollment, it must contract with external providers, which dilutes the integration advantage and creates new cost exposure. Growth actually intensifies the network management challenge rather than resolving it.

Risk matrix showing four PSHP challenges mapped by financial impact and management difficulty: scale sustainability, governance conflicts, insurance expertise gaps, and network limitations.

Five Financial Strategies Separating Profitable PSHPs in 2026

The health systems that are sustaining and growing their provider-sponsored plans share specific financial execution disciplines. These are not theoretical frameworks. They are the operational moves that show up in improved medical loss ratios, risk-adjusted revenue accuracy, and membership retention.

Strategy 1: Internal steering and narrow network optimization. The primary financial advantage of a PSHP is the ability to capture the full dollar by keeping care within the parent system. CFOs who are executing this well use tiering structures that offer members meaningfully lower out-of-pocket costs when they use owned facilities and physicians. This minimizes leakage to competitors and maintains utilization at high-fixed-cost assets like surgical centers and specialty clinics. The financial test is simple: if the plan's benefits design does not actively reward in-network utilization, you are carrying insurance risk without capturing the clinical cost advantage that justifies it.

Strategy 2: Proactive payment integrity through AI and automation. With medical costs continuing to rise and PSHP margins typically running between 1% and 3%, retroactive claims auditing is too slow and too expensive. The organizations performing well in 2026 are implementing AI-driven payment integrity tools that analyze claims before payment to identify coding errors, potential fraud, and non-covered services in real time. This shifts the operational model from "pay and chase" to pre-payment accuracy. From the payer side at Florida Blue Medicare, the volume of post-payment recovery activity required without these systems is significant. For a deeper look at how this plays out on the provider side, theAI in Revenue Cycle framework covers the full payer take-back dynamic and what finance leaders are doing about it.

Strategy 3: Integrated risk adjustment and clinical documentation alignment. PSHPs with direct EHR access have a structural advantage over national insurers in Medicare Advantage risk adjustment that most are not fully exploiting. National insurers spend heavily on in-home health assessments to capture undiagnosed chronic conditions because they cannot access provider records directly. A PSHP can align its actuarial team with the system's clinical documentation specialists and embed prompts in the clinical workflow to ensure accurate coding before the annual risk adjustment cycle closes. The revenue impact of closing documentation gaps in MA is direct and measurable: more accurate HCC coding produces higher capitation payments from CMS. The compliance dimension of this work deserves equal attention. TheAetna $117.7M False Claims Act settlement is a useful case study in how aggressive risk adjustment practices that cross into unsupported coding create significant legal and financial exposure.

Strategy 4: Direct-to-employer contracting. Finance leaders at maturing PSHPs are increasingly bypassing traditional national brokers to contract directly with regional employers. Direct-to-employer arrangements reduce broker commissions and marketing overhead while securing commercially insured membership that diversifies away from government program volatility. The value proposition to employers centers on care coordination, lower total cost of care, and customized benefit designs featuring the health system's clinical capabilities. The Advisory Board's research notes that employers typically require a 15% premium discount to switch from a national plan to a narrower regional network. That hurdle is achievable for PSHPs that have demonstrable cost and quality advantages, but requires rigorous actuarial support to price sustainably.

Strategy 5: Prospective value-based payment structures within the system. PSHPs that continue paying their owned provider groups on fee-for-service terms are structurally undermining their own MLR performance. The move to prospective bundled payments or per-member-per-month capitation within the system shifts provider incentives toward prevention and efficiency. When the clinical side has skin in the game, unnecessary utilization decreases, and the plan's claims cost trajectory improves. This internal restructuring is often more complex politically than operationally. The broader challenge ofwhy value-based care contracts fail to pay out as planned is directly relevant here: the same contract design problems that undermine external VBC arrangements show up inside integrated systems too.

If you are currently working through a PSHP financial model or evaluating whether your health system's insurance strategy needs restructuring, I work with finance teams on exactly these questions. You can learn more about that work at hfi.consulting.

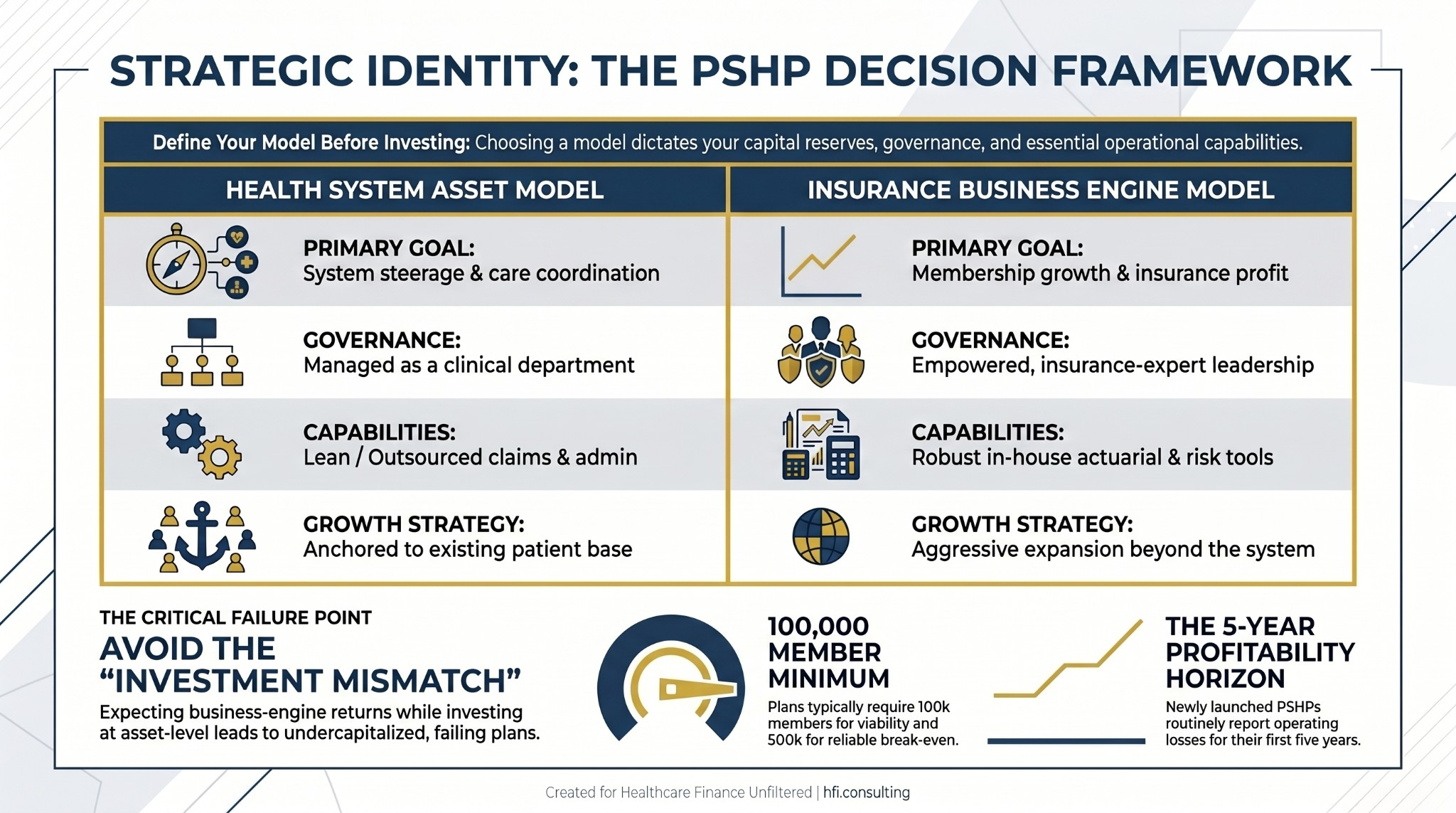

The Identity Question Every PSHP Board Must Answer

The Advisory Board's 2026 research surfaces a distinction that finance leaders often avoid because it is uncomfortable: Is your PSHP a health system asset or an insurance business engine?

A health system asset model accepts break-even or modest losses in the plan if the broader system benefits through steerage, quality improvement, and integrated care coordination. It uses lean insurance operations, often outsourcing claims administration, and measures success primarily in system-level clinical outcomes.

An insurance business engine model requires robust in-house actuarial, claims, and network contracting capabilities, empowered plan governance with insurance-experienced leadership, and ambitious membership growth goals beyond the system's existing patient base.

The critical failure point is operating in both models simultaneously. Leadership that expects business-engine returns but invests only at health-system-asset levels consistently produces undercapitalized plans that cannot compete and eventually exit. Clarity about which model the organization is building is a prerequisite for sound capital planning, governance design, and performance measurement. The Kaiser Permanente $9.3B profit analysis is instructive here: even the most successful PSHP in the country faces scrutiny when the nonprofit mission and insurance profitability appear to be pulling in different directions.

Comparison table showing differences between health system asset and insurance business engine PSHP models across governance, capabilities, and growth strategy dimensions.

Building the Financial Foundation: What the Successful Plans Did First

The PSHPs that have scaled into major regional insurers share a consistent staged development path. They started by self-funding employee health benefits, which provided early claims management experience without direct insurance risk. They then entered Medicare Advantage or Medicaid managed care, leveraging well-understood revenue levers like risk adjustment and Stars quality bonuses. Commercial expansion came later, after the plan had developed actuarial pricing, broker relationships, and utilization management capabilities that the commercial market requires.

Peak Health, owned by WVU Health System, Marshall Health Network, and Valley Health, articulated the financial logic clearly. Leadership noted they could not improve health outcomes while managing expenses without true financial alignment, which drove the eventual decision to take on full insurance risk. That sequence matters: the clinical proof points came first, followed by the insurance structure to commercialize them.

For CFOs evaluating a PSHP launch or assessing an existing plan's trajectory, the capital planning question is not whether the plan will eventually reach break-even. It is whether the organization has the reserves and the board patience to sustain the operating losses while building the operational infrastructure that sustainable scale requires.

The Honest CFO Assessment

Not every health system should own a health plan. The premium dollar that PSHPs aim to capture requires active total cost of care management to actually realize. Without prior authorization structures, care steering incentives, and utilization management capabilities, launching a health plan adds operating expense without capturing the margin benefit.

In my work observing both payer and provider organizations, the most common gap is governance, not strategy. The clinical vision for integration is usually sound. The financial accountability structures that would actually enforce that integration across the plan-provider divide are typically underdeveloped.

Before your next board meeting on PSHP strategy, five questions are worth putting to the table:

Do we have the capital and organizational stamina to sustain early operating losses, potentially for five or more years?

Can we acquire or develop the actuarial, claims, and utilization management expertise that competitive plan operations require?

Are we prepared to implement care management structures that may create friction with our own clinical revenue?

What specific value will our plan offer that existing regional or national insurers do not?

Is leadership unified in support of this model with the patience to measure success over multiyear horizons?

If any of those questions produce hesitation, the strategic work is not yet complete.

What is your health system's current relationship with a provider-sponsored plan, whether you are operating one, considering launching one, or recently exiting? Hit reply and tell me where you are in that evaluation. I read every response.

P.S. Whether or not a PSHP makes sense for your system, the underlying question it forces is the right one: How does your health system create financial alignment between care delivery decisions and cost accountability? That question has answers outside the PSHP model too. What structure is your organization using to address it?