Medicare Advantage 2026: The Payer CFO Playbook for the Most Challenging Year in Plan History

V28 is fully phased in, Part D liability just tripled, and utilization isn't retreating. Here's how finance leaders protect margins now and position for 2027 and beyond.

Every Medicare Advantage finance leader knew 2026 would be difficult. Few modeled just how difficult. The full phase-in of V28, the Inflation Reduction Act's Part D redesign, and a utilization baseline that refuses to normalize have converged into a single fiscal year — and the CMS Advance Notice offered a 0.09% payment increase in response.

If your 2026 budget was built on more favorable assumptions, the second half of this year is not a waiting game. It is the planning window for 2027 and beyond.

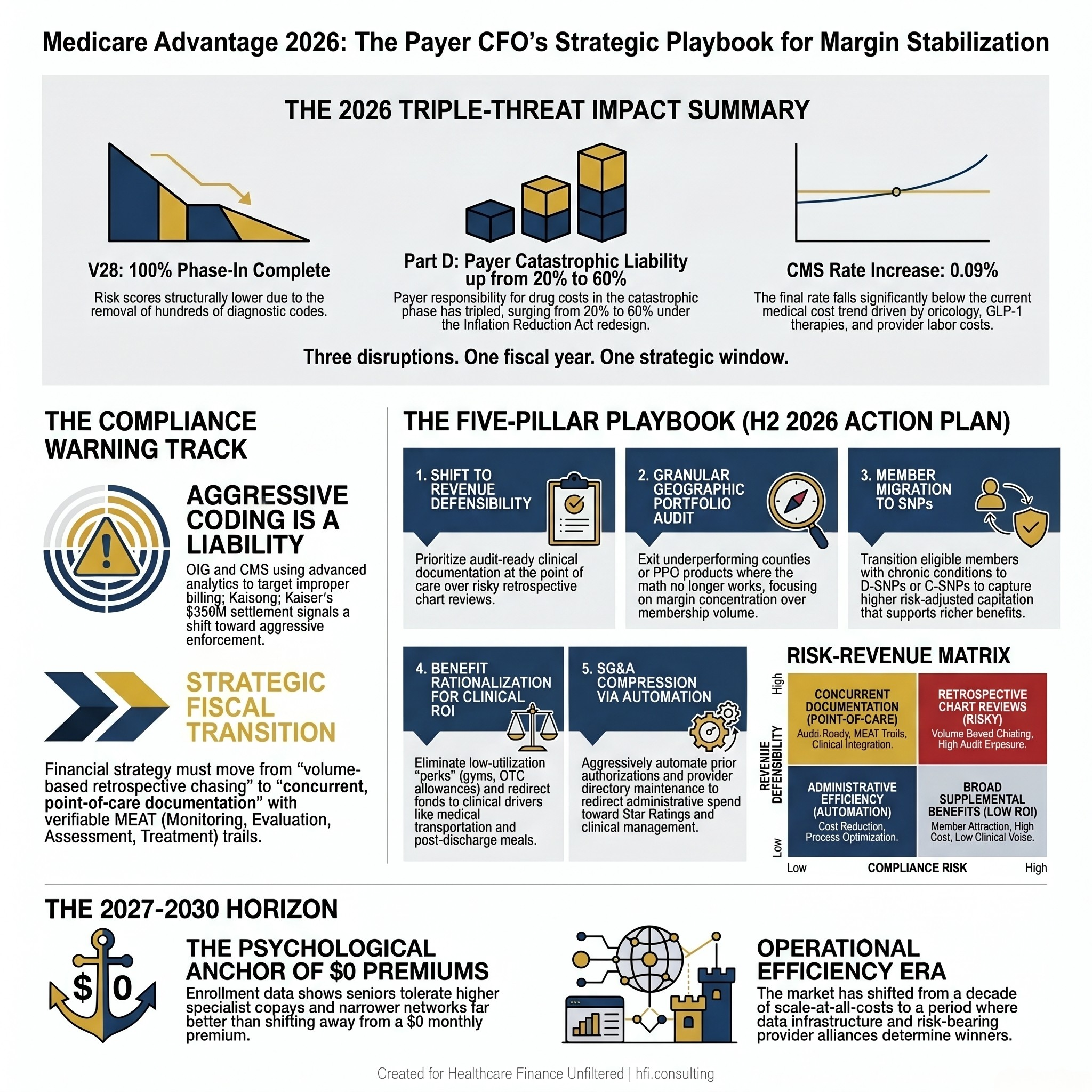

Infographic showing three 2026 Medicare Advantage financial pressures: V28 full phase-in, Part D liability increase from 20% to 60%, and 0.09% CMS payment rate increase

Why 2026 Is Structurally Different

The pressure MA plans face in 2026 is not a single-variable problem. It is three concurrent disruptions compounding simultaneously on the same income statement.

The first is the complete phase-in of the CMS-HCC V28 risk adjustment model. This year marks the end of the multi-year transition, meaning V28 now dictates 100% of risk scores. By eliminating hundreds of diagnostic codes and restructuring hierarchical categories, V28 has structurally reduced average risk scores across the industry. Retrospective chart reviews no longer generate predictable revenue lifts without underlying clinical documentation to support them.

The second disruption is the Part D redesign driven by the Inflation Reduction Act. The 2026 benefit design imposes a strict annual out-of-pocket cap for beneficiaries, which is a genuine win for seniors. The financial trade-off for plans is significant. Payers are now responsible for 60% of drug costs in the catastrophic phase, up from 20% in prior years. That shift alone has caused national average Part D bids to surge and compressed the premium rebates historically used to fund supplemental benefits.

The third pressure is utilization. Post-pandemic normalization did not happen. Payers are managing surging pharmacy costs from oncology and GLP-1 therapies alongside provider rate renegotiations driven by health system labor and supply-chain expenses that have not retreated. As Steve Mongelli, president at mPulse, noted in a recent HIMSSCast: "Medical costs are running above historical norms." The CMS Advance Notice confirmed what plan actuaries already knew. The proposed rate came in below the medical cost trend.

That combination is what makes 2026 different. Any one of these factors is manageable. All three arriving simultaneously, in a single fiscal year with a flat rate increase, is a structural compression event.

What This Means for Your P&L

Plans that built their 2026 budgets on V27-era revenue assumptions, modest catastrophic drug exposure, and utilization trends reverting toward pre-pandemic norms are now operating on a fundamentally incorrect financial model. The gap between projected and actual margin is not recoverable through traditional levers in the second half of the year.

The realistic target for 2026 is stabilization, not restoration. Your strategic energy belongs in the planning work that determines where your organization lands at the start of 2027.

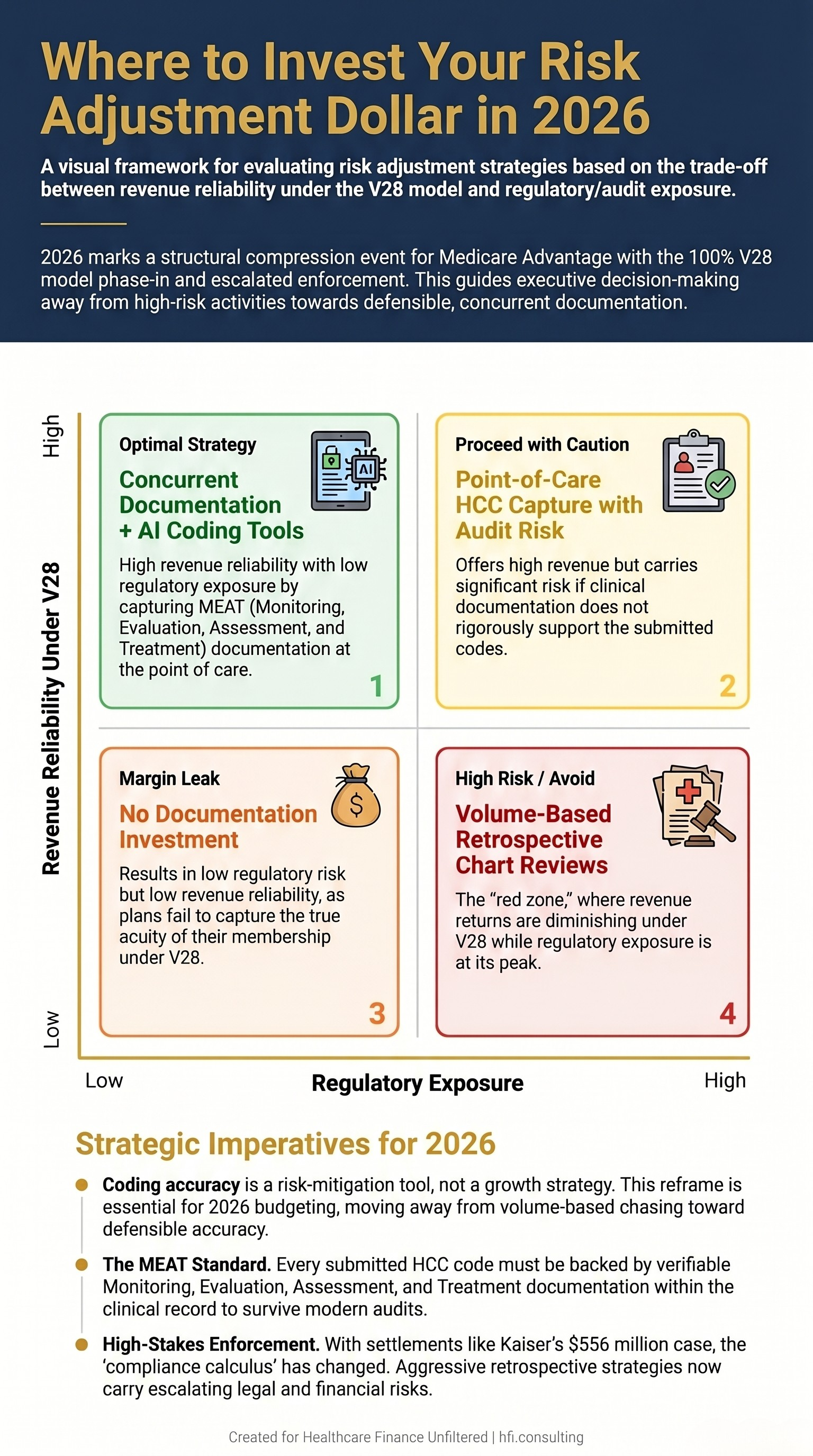

This is also the year CMS and the Office of Inspector General are most aggressively auditing plan-year risk adjustment data. Two nine-figure settlements in the past eighteen months, including Kaiser's $556 million settlement, have changed the compliance calculus for every finance leader in the room. You can review that enforcement trajectory in detail here: When to Sound the Alarm: What Kaiser's $556M Medicare Advantage Settlement Teaches Finance Leaders About Risk Adjustment Fraud.

The practical implication is that aggressive retrospective coding strategies carry both diminishing revenue returns under V28 and escalating regulatory exposure. Those two dynamics together create a clear directional signal for where investment should go.

2x2 risk-revenue matrix showing Medicare Advantage risk adjustment investment strategies, from concurrent documentation tools (optimal) to retrospective chart reviews (high regulatory exposure)

The Five-Pillar CFO Playbook for the Second Half of 2026

The second half of 2026 (H2) is the planning and repositioning window. These five areas represent where finance leaders have actual leverage before 2027 bid cycles close and benefit structures lock.

1. Shift From Revenue Maximization to Revenue Defensibility

The strategic reframe that matters most right now is this: coding accuracy is a risk-mitigation tool, not a growth strategy. CMS and OIG are using increasingly sophisticated data analytics to identify patterns that correlate with improper billing. If their analytics surface something before your internal audit does, you have lost the ability to address it on your terms.

Shift risk adjustment investment away from volume-based retrospective chart chasing. Move toward concurrent, point-of-care documentation technologies that build an audit-ready trail from the encounter forward. Every submitted HCC code needs verifiable MEAT documentation — Monitoring, Evaluation, Assessment, and Treatment — tied to the clinical record. That is not just a compliance posture. Under V28, it is also the most reliable path to defensible revenue.

2. Execute a Granular Geographic Portfolio Audit

The era of chasing membership volume in every county is over. Scale is not a margin strategy when the counties generating the scale are also generating adverse selection and premium erosion.

The work for H2 2026 is a rigorous, county-level margin-integrity audit. Identify which geographies are structurally profitable at 2026 rate levels and which require a benefit structure that cannot be sustained. Prepare exit scenarios for unprofitable counties or underperforming PPO products before the next bid cycle requires a decision. The Medicare Advantage Network Contraction 2026 article covers how national plans have already started this process and what the downstream member impact looks like for your planning assumptions.

UnitedHealthcare's decision to exit underperforming markets, projecting a drop of over one million members, illustrates the calculation clearly. Protecting margin concentration in profitable HMO networks now is more valuable than defending market share in counties where the math does not work.

3. Migrate Eligible Members to Special Needs Plans

Standard MA enrollment growth is slowing. Enrollment in Dual-Eligible SNPs and Chronic Condition SNPs is growing. There is a financial reason for that divergence that belongs in your capital allocation conversation.

SNPs receive significantly higher, risk-adjusted capitation payments from CMS under V28 because of member acuity. That additional revenue allows plans to sustain rich, targeted supplemental benefits for that sub-population without relying on rebate-funded perks that are no longer financially viable for a general enrollment population. If a portion of your current standard individual MA membership has undiagnosed or undocumented qualifying chronic conditions, an active screening and migration program is both a care coordination investment and a revenue strategy.

4. Rationalize Supplemental Benefits Around Clinical ROI

The rebate-fueled race to fund $0 premiums and broad supplemental packages is unsustainable at current Part D liability levels. The financial logic of offering large over-the-counter cash allowances, general gym memberships, or utility assistance to a general enrollment population has deteriorated significantly.

The benefit design work for 2027 bid cycles should start now. Reduce or eliminate benefits with low utilization rates and no documented clinical return. Redirect that budget toward benefits with measurable impact on Star Ratings and medical cost management: medical transportation, post-discharge home meals, targeted health risk assessments, and chronic disease management programs. CMS now requires publicly posted eligibility criteria for Special Supplemental Benefits for the Chronically Ill. Use that requirement as a filter for evaluating every supplemental dollar you are currently spending.

5. Compress SG&A Through Automation

As gross margins tighten, internal cost structures have to follow. Prior authorization processing, provider directory maintenance, and routine member services are high-friction administrative functions that are candidates for automation in H2 2026. Partner with your CIO to identify the implementation timeline and expected FTE reallocation toward clinical management and Star Ratings capabilities.

The plans that emerge from 2027 in a stronger position will not be those that cut spending across the board. They will be those that redirected administrative spend toward the functions that drive revenue defensibility and member retention simultaneously.

From my time on the payer side at Florida Blue Medicare, the pattern I observed most consistently was this: plans that invested in data infrastructure and member engagement between bid cycles outperformed those that reacted to rate changes after the fact. The 2026 H2 window is exactly that interval. The decisions made between now and the next bid cycle will determine the 2027 and 2028 operating position.

If your plan is working through the 2027 final rule implications for benefit design and bid strategy, the full framework is here: CY 2027 Medicare Advantage Final Rule: What MA Finance Leaders Must Plan For Now.

Healthcare Finance Unfiltered publishes practitioner-level MA finance analysis every week. If you are working through benefit design decisions for 2027, payer contract strategy, or risk adjustment compliance frameworks, subscribe to get the full analysis as it publishes.

Subscribe to Healthcare Finance Unfiltered

The Retention Challenge: Keeping Members While Shifting Costs

The financial logic of compressing benefits and raising cost-sharing is straightforward. The enrollment logic is more complicated.

Seniors have shown consistently that they will tolerate higher specialist copays and narrower networks far more readily than they will tolerate a plan that moves from a $0 monthly premium to any premium at all. Studies on enrollment behavior confirm that the headline premium functions as a psychological anchor in a way that downstream cost-sharing does not. Plan actuarial and bid teams that understand this are absorbing cost shifts through specialist copays and out-of-pocket maximum adjustments while protecting the $0 premium at the front end.

This is not a marketing insight. It is a financial architecture decision that needs to be reflected in how benefit design and bid strategy teams are communicating across your organization. The finance team that understands the enrollment behavior implications of cost-sharing choices will produce more accurate membership projections for budget planning.

The second retention tool that belongs in the 2027 planning conversation is value-based provider alliances. Plans that shift clinical financial risk to risk-bearing primary care groups — through capitation arrangements with groups structured to manage utilization at the point of care — create a member experience that reads as high-touch clinical engagement rather than prior authorization friction. When the provider is the one managing care coordination, the plan's utilization management posture becomes less visible to the member and less likely to drive voluntary disenrollment during the Annual Enrollment Period.

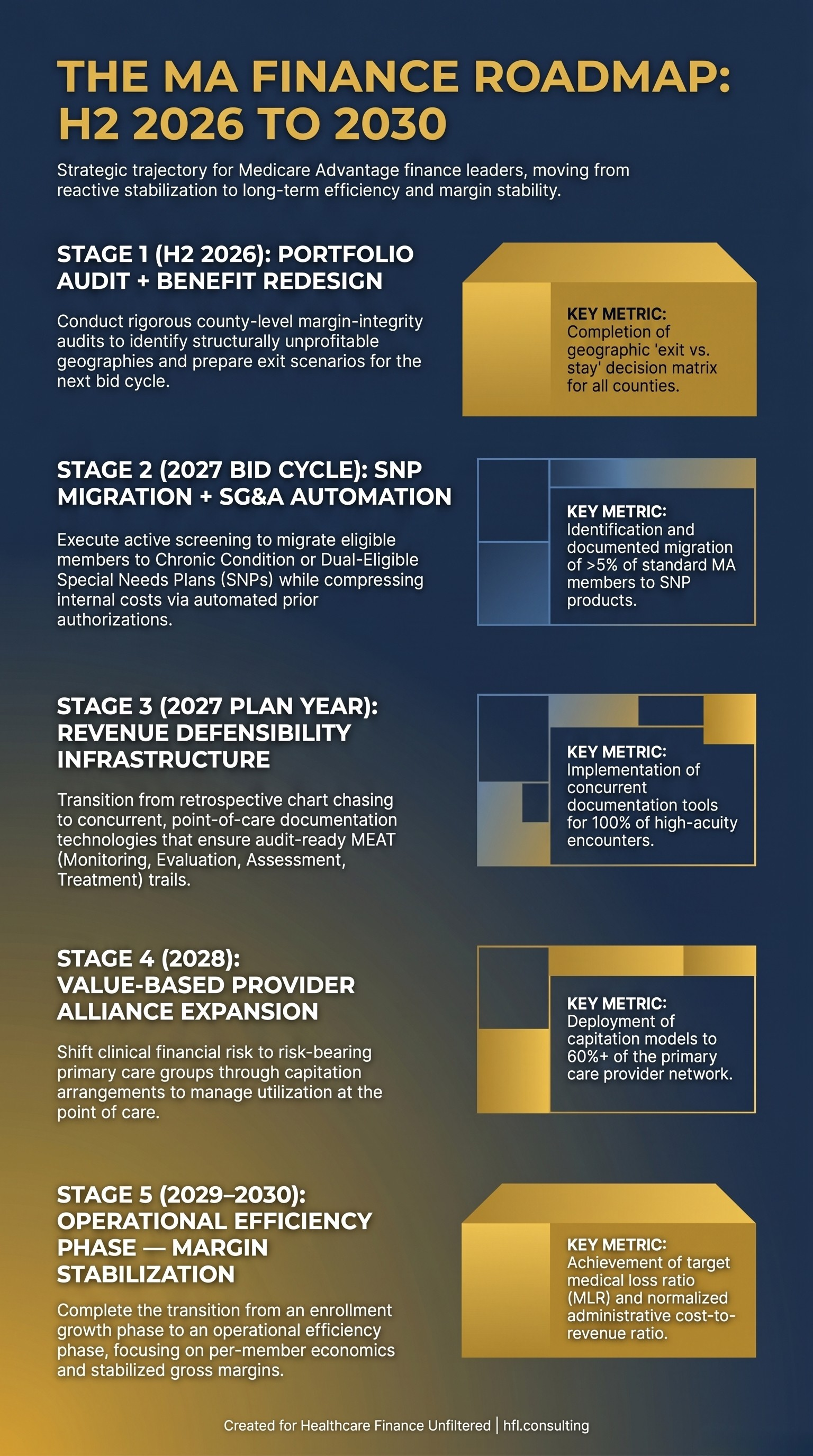

Timeline showing Medicare Advantage finance leader roadmap from H2 2026 portfolio audit through 2030 margin stabilization across five strategic stages

The 2027-2030 Horizon

The broader structural signal coming from the MA market is a transition from an enrollment growth phase to an operational efficiency phase. The plans that used the previous decade to scale membership at the expense of per-member economics are now being forced to rationalize. The plans that used it to build data infrastructure, strengthen provider relationships, and develop accurate actuarial models for high-acuity sub-populations are entering this period in a fundamentally stronger position.

Regional plans have a specific structural advantage worth noting. Because regional Blue Cross Blue Shield plans cannot exit markets without damaging multi-line brand equity across commercial, employer, and ACA exchange books, their strategic playbook is different from national carriers. Instead of exiting counties, they are using deep, decades-long provider relationships to create lower-cost care models that shield members from cost shifts at the primary care level. For regional plan finance teams, that provider relationship investment is not a social mission — it is a margin strategy.

The CFOs who will look back on 2026 as the turning point in the right direction are those who treated the second half of this year as a planning window, not a waiting game. The bid cycle closes. The benefit structures lock. The member enrollment decisions follow.

The analysis you produce between now and the end of 2026 is the foundation for every financial outcome your organization will report in 2027 and 2028.

If you found this framework useful, forward it to a colleague working through benefit design or bid strategy. And if you are a payer CFO or VP of Finance who wants to dig into a specific aspect of the 2027 planning cycle — risk adjustment compliance, SNP migration strategy, or SG&A compression analysis — hit reply. I read every response.

Subscribe to Healthcare Finance Unfiltered | hfi.consulting

P.S. Which of the three 2026 disruptions — V28 full phase-in, Part D liability shift, or utilization trends — is creating the most pressure in your current budget? Hit reply and tell me. I am building the next analysis around what finance leaders are actually navigating right now.