The Compliance Tax: How CMS Administrative Burden Became a Hidden Line Item Every Healthcare CFO Is Funding

CMS keeps adding reporting layers to prove compliance, then rewrites the rules. Here is what it is actually costing you.

CMS does not intend to raise the cost of care. But every reporting mandate, every revised cost report worksheet, every interoperability requirement backed by a condition of participation carries a price tag that lands on your operating budget before it ever reaches a patient. If you have not quantified what compliance administration is actually costing your organization, you are almost certainly underestimating it.

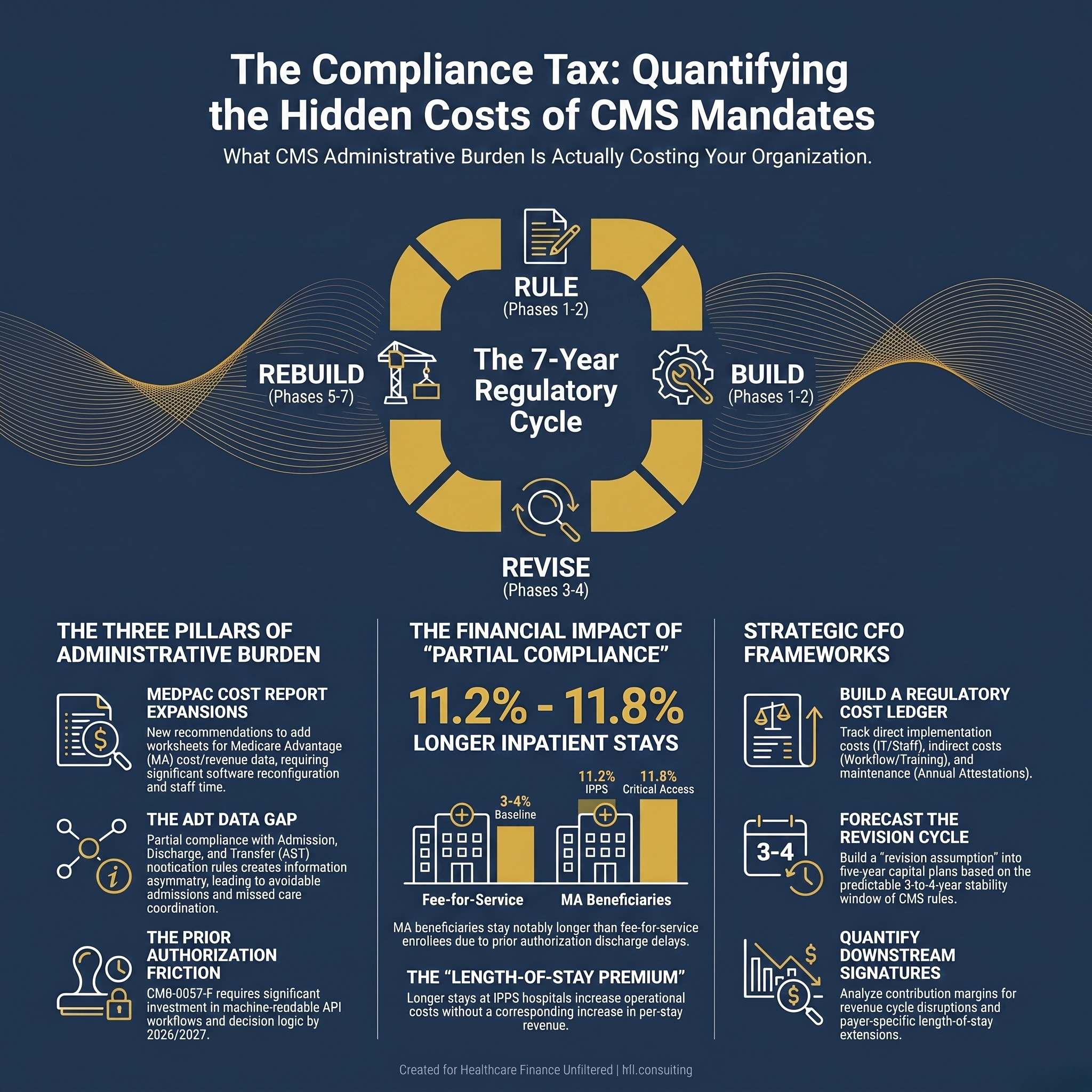

Circular diagram showing the CMS regulatory burden cycle: rule finalized, infrastructure built, rule revised, rebuild required, with title "The Compliance Tax"

The Compliance Architecture Is Not Designed for Efficiency

There is a pattern that every healthcare finance leader eventually recognizes. A federal agency identifies a problem, whether that is fraud in Medicare Advantage, insufficient discharge data, or inadequate cost visibility. CMS responds with a reporting requirement. Hospitals and health plans spend two to four years building the infrastructure to meet that requirement. Then CMS revises the methodology, expands the scope, or replaces the framework entirely.

The people who absorb that cost are not regulators. They are your cost report team, your IT department, your compliance staff, and the revenue cycle managers trying to reconcile new requirements against operational systems that were not designed with the latest rule in mind.

The American Hospital Association put it plainly in their regulatory burden analysis: the scope and pace of regulatory change is outstripping many providers' ability to absorb it. That is not a complaint. It is a financial fact that belongs in your budget model.

What MedPAC Just Handed CFOs to Read

The Medicare Payment Advisory Commission released its June 2026 report to Congress with a chapter on Medicare Advantage and hospital finances. The headline finding drew attention: there is no statistically significant association between MA enrollment growth and hospital all-payer operating margins.

That conclusion is important context. But buried inside the same chapter is something every CFO needs to read more carefully.

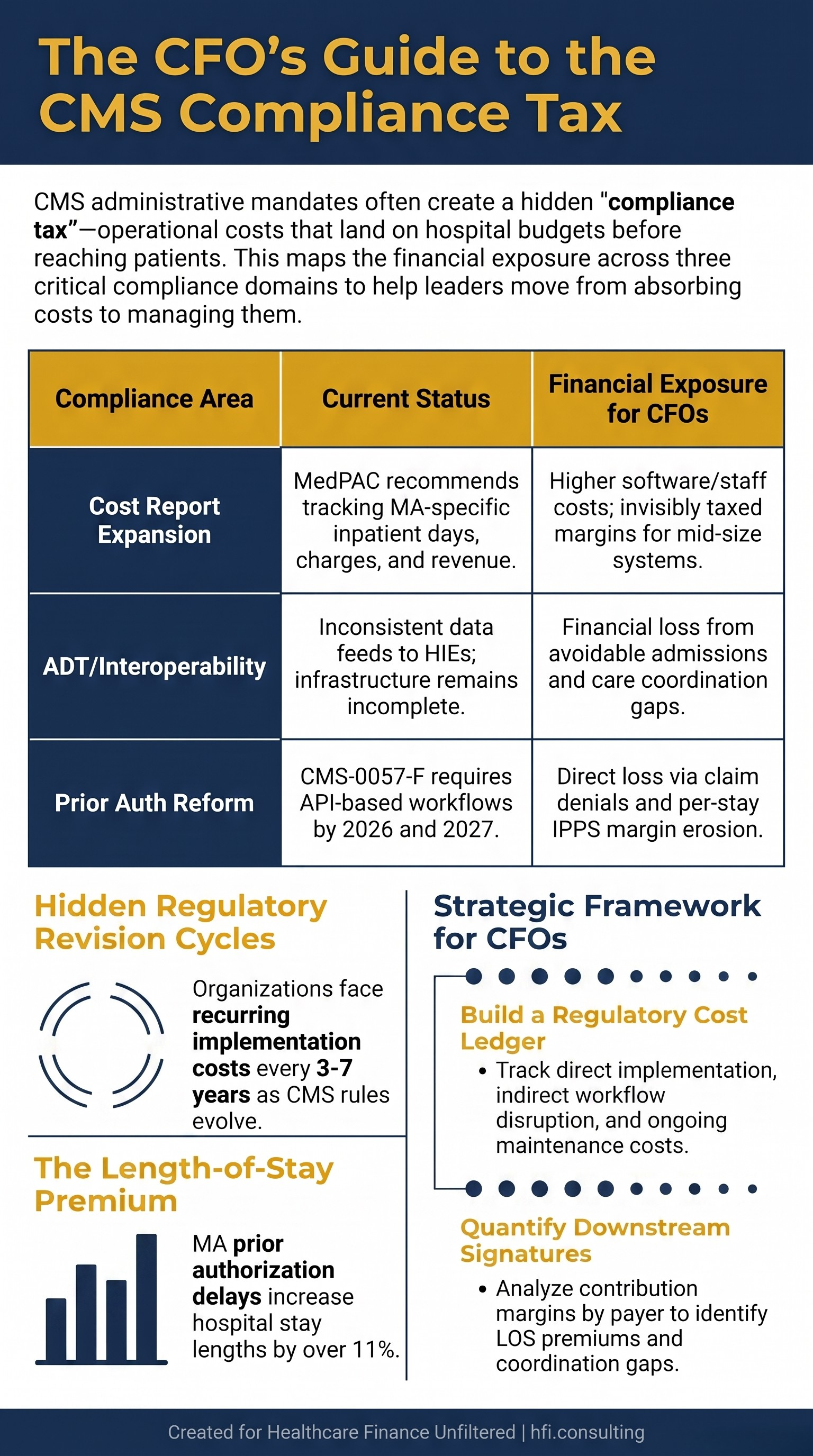

MedPAC recommended adding worksheets to hospital cost reports to capture MA-specific cost and revenue data. Those inputs would include MA inpatient days and MA charges by cost center, with revenue detail covering beneficiary cost-sharing, claims-based payments, and other payments.

The commission then acknowledged something worth underlining: its recommendations could raise the administrative burden on hospitals.

Read that again. A federal advisory body is recommending a new cost report expansion and flagging, in the same breath, that it will add administrative work. That acknowledgment is rare. The underlying dynamic is not.

Current hospital cost-reporting principles have limitations that would confound comparisons of FFS Medicare and MA margins. Administrative costs that stem from MA operations, for example, would not be captured.

In other words, the reporting expansion is designed to fix a data gap. But the data gap exists partly because the original cost report structure was not built for the MA environment. CMS is now proposing a solution that creates its own administrative cost without solving the underlying visibility problem.

The ADT Problem Is the Same Pattern at a Different Layer

While MedPAC focuses on cost report structure, a parallel compliance gap is playing out in real-time data exchange. The 2020 CMS Interoperability and Patient Access Rule created conditions of participation requiring Medicare and Medicaid-participating hospitals to send electronic ADT notifications for patient admissions, discharges, and transfers.

The requirement exists. The infrastructure is incomplete. And the data still does not flow consistently to the parties who need it.

Florida is a useful case study. CRISP Shared Services took over operations for the Florida Health Information Exchange in July 2026, replacing the prior vendor and expanding capabilities for real-time ADT alerting. Major health systems in major markets are still not consistently feeding ADT data into the statewide HIE. That means payers like Florida Blue, the largest insurer in the state, are operating care management programs with incomplete event notification feeds.

This is not a technology failure in isolation. It is a compliance architecture problem. The federal mandate targets ADT notifications to treating providers for care coordination purposes. It does not universally require hospitals to feed statewide HIEs or direct payer connections. So hospitals comply with the minimum. Payers receive incomplete data. Care management programs operate with gaps. And nobody has a clear cost estimate for what that information asymmetry is producing in avoidable admissions, delayed discharges, and missed care coordination opportunities.

The administrative burden is not just the cost of complying. It is also the cost of operating in an environment where compliance is partial and the downstream financial effects are invisible.

Prior Authorization Is the Third Leg of This Stool

The prior authorization environment sits at the intersection of administrative burden and revenue integrity. CMS-0057-F, the Interoperability and Prior Authorization Final Rule, requires payers to implement API-based prior authorization workflows by 2026 and 2027. The goal is to reduce turnaround times and improve transparency.

From the payer side, the implementation cost is significant: new APIs, vendor integrations, staff retraining, and governance structures to manage decision logic that must now be machine-readable. From the provider side, the benefits are real but delayed. The workflow changes require EHR configuration, staff process changes, and monitoring to verify that automated approvals are functioning as intended.

Meanwhile, prior authorization activity remains a source of direct financial exposure. MA concerns for hospital leaders include issues with claim denials, payment downgrades, and administrative costs, along with delays in discharges to skilled nursing facilities and other post-acute care settings.

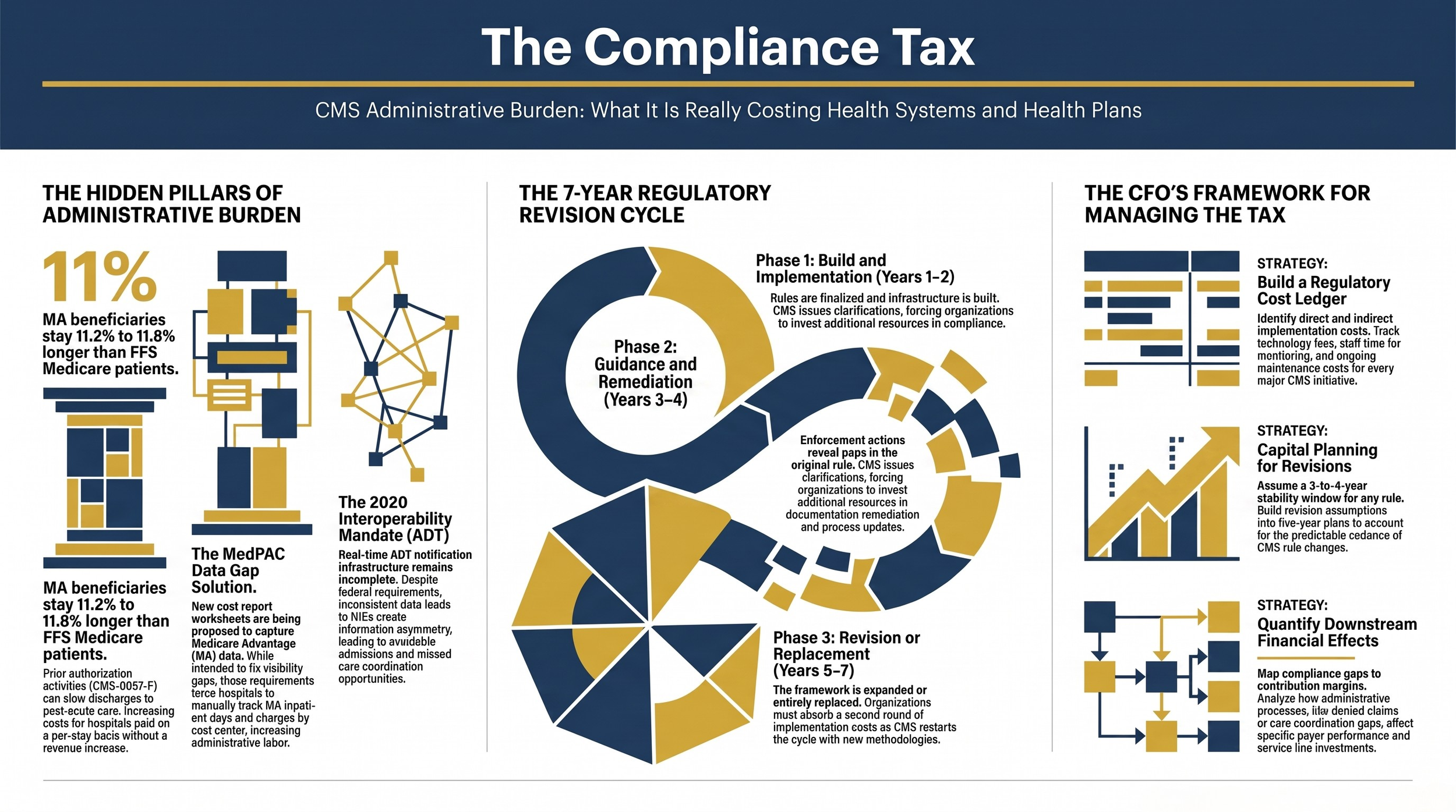

MA beneficiaries stay in inpatient settings for notably longer periods than comparable enrollees in fee-for-service Medicare. Average length of stay was 11.2% longer at IPPS hospitals and 11.8% longer at critical access hospitals after controlling for the discharging hospital, services received, comorbidities, and intended discharge site.

The length-of-stay premium is not random. MA plans, through prior authorization activities, can slow beneficiary discharges to post-acute care and therefore increase the average time beneficiaries stay in hospitals. At IPPS hospitals paid on a per-stay basis, longer stays increase costs without a corresponding revenue increase.

That is a direct financial loss produced by an administrative process. It is not captured on a cost report. It does not appear in a compliance filing. But it shows up in your contribution margin analysis.

Three-row comparison table showing CMS compliance areas, their current implementation status, and financial exposure for hospital and health plan CFOs

What the Regulatory Cadence Actually Costs

Here is the sequence that repeats across almost every CMS initiative:

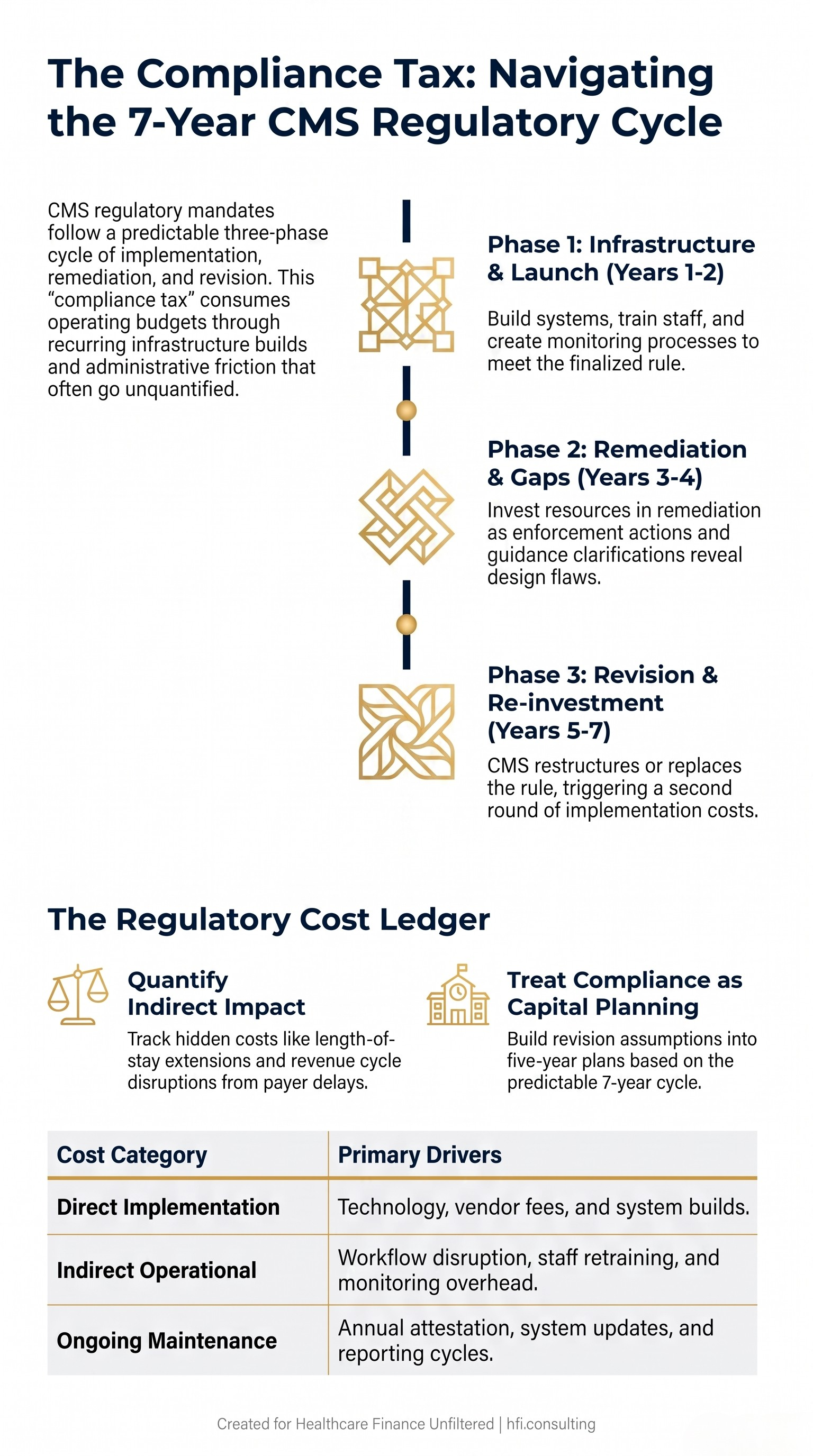

Phase 1 (Years 1-2): Rule is finalized. Organizations build infrastructure, train staff, update systems, and create internal monitoring processes to demonstrate compliance.

Phase 2 (Years 3-4): CMS issues guidance clarifications, enforcement actions reveal gaps in the original rule design, and organizations invest additional resources in remediation or expanded documentation.

Phase 3 (Years 5-7): CMS proposes revisions. Sometimes the original rule is expanded. Sometimes it is restructured. Sometimes a new framework replaces it entirely. Organizations absorb a second round of implementation costs.

The AHA's regulatory burden documentation is consistent on this point. Federal regulations are intended to ensure safe, high-quality care. Providers prioritize compliance as a core operational function. The problem is the pace and volume of change, not the principle behind it.

Vertical timeline diagram showing the three-phase CMS regulatory cycle from initial rule to revision, with cost implications at each phase labeled for healthcare CFOs

From my time in payer operations, the cycle is equally visible from that side of the table. A health plan builds out a utilization management program to meet CMS standards. Those standards shift. The plan rebuilds. That rebuild requires actuarial reassessment, vendor renegotiation, and staff retraining. The cost lands in the MLR, which flows through to premium pricing, which affects competitive positioning. None of that chain shows up in a single line item that reads "regulatory compliance cost."

What Finance Leaders Can Actually Do About This

The compliance tax is real, but it is also manageable if you treat it as a budget category rather than a background operating assumption. Three frameworks help.

Build a regulatory cost ledger. Every major CMS initiative should have an associated internal cost estimate: direct implementation costs (technology, staff time, vendor fees), indirect costs (workflow disruption, staff retraining, monitoring overhead), and ongoing maintenance costs (annual attestation, system updates, reporting cycles). In my work at Ascension across seven hospitals, the difference between organizations that managed regulatory cost well and those that absorbed it invisibly came down to whether someone owned that ledger. Without it, regulatory burden remains invisible to your board and your CFO peers.

Track the revision cycle as a capital planning input. If a CMS rule has been in place for three to four years, begin estimating the probability and scope of revision. IPPS updates, MA rate adjustments, and interoperability rule expansions follow predictable patterns. Building a revision assumption into your five-year plan is more accurate than assuming the current compliance state is stable.

Quantify the downstream financial effects, not just the direct compliance costs. Length-of-stay extensions from MA prior authorization delays, care coordination gaps from incomplete ADT feeds, and revenue cycle disruption from denied claims under shifting documentation requirements all have financial signatures. If your contribution margin analysis is not capturing those effects by payer, you are missing a material piece of your revenue picture.

If you want a structured framework for mapping regulatory costs to service line and payer performance, that is exactly the work I do through HFI Consulting. The organizations that have done this analysis consistently find the number larger than they expected.

Navy background image with bold title "The Compliance Tax" and subheading about CMS administrative burden costs for healthcare CFOs

The Cost Report Expansion Illustrates the Broader Problem

Return to the MedPAC recommendation on cost reporting. The commission wants better MA financial visibility, which is a legitimate goal. The current cost report structure cannot isolate MA margins from FFS margins, which means CMS is making policy decisions about a program that now covers 54% of Medicare beneficiaries without clean financial data from the provider side.

The solution proposed is to add worksheets. Those worksheets require hospitals to track MA inpatient days separately, allocate charges by cost center for MA patients, and detail revenue streams that current systems may not be designed to separate.

For a large health system with robust cost accounting infrastructure, this is an operational challenge. For a critical access hospital or a mid-size community health system, it may require a new software configuration, a revised data collection process, and additional cost accounting staff time.

MedPAC acknowledged the burden. That acknowledgment does not reduce it.

The deeper issue is that CMS and its advisory bodies are designing reporting requirements based on what data they need, without a full accounting of what it costs to produce that data. That asymmetry is a policy problem. It is also a budget problem for every organization reading this.

Where This Leaves CFOs and VP Finance Leaders

The compliance environment is not getting simpler. MA enrollment now covers the majority of Medicare beneficiaries, and CMS is actively working to improve its visibility into how those patients are affecting hospital and health plan finances. That means more reporting requirements, not fewer.

Prior authorization reform is moving through implementation with genuine operational complexity on both sides. ADT data infrastructure is improving but remains inconsistent. Cost report expansion is on the table. Each of these represents a budget line that does not yet exist in most five-year operating plans.

The CFOs who are best positioned are not the ones who have minimized their compliance costs. They are the ones who have made those costs visible, tracked them accurately, and used that visibility to make better decisions about payer contract terms, service line investment, and operational capacity.

That visibility starts with treating regulatory compliance as a financial management discipline, not a back-office function. The compliance tax is real. The question is whether you are managing it or absorbing it.

Learn more about building a regulatory cost framework for your organization at hfi.consulting.

P.S. Which CMS compliance initiative has created the most unexpected operational cost in your organization over the last 18 months? Hit reply and tell me. I want to know if ADT infrastructure, prior authorization API builds, or cost report revisions are hitting finance teams hardest right now.

HFI Consulting works with health systems, medical groups, and payer organizations on contribution margin analysis, payer performance assessment, and regulatory cost mapping. If your organization is trying to quantify what CMS administrative burden is actually costing you, that is a conversation worth having.