Physician Enterprise Finance: What the Consolidation Wave, ASC Boom, and POH Legislation Mean for Healthcare CFOs

82% of physicians are now employed. The financial infrastructure hasn't caught up. Here's where the margin is hiding.

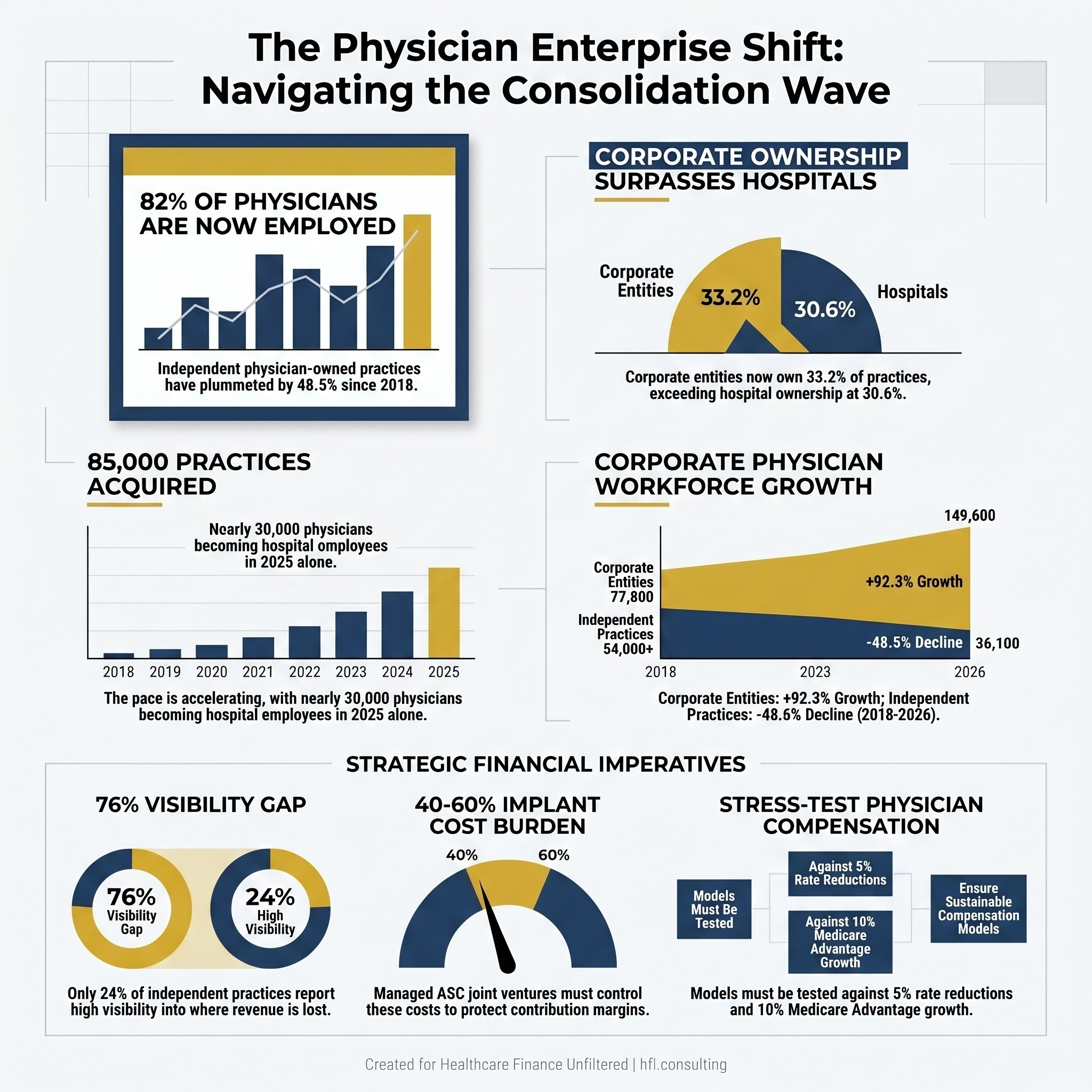

The American Medical Association tracks this data so no one can claim ignorance: 82% of practicing physicians in the United States are now employed by hospitals or corporate entities. Independent physician-owned practices have dropped by 48.5% since 2018. The profession has been restructured, absorbed, and financially reengineered — and the pace is not slowing.

For CFOs managing health systems, payer organizations, or medical groups, that consolidation wave creates both significant financial exposure and significant opportunity. The question is whether your financial framework has kept pace with the structural reality on the ground.

Side-by-side comparison showing physician employment shift from 2018 to 2026, with 82% now employed by hospitals or corporate entities.

The Numbers Your Board Should Already Know

According to a 2026 report from the Physicians Advocacy Institute and Avalere Health tracking eight years of consolidation data, the numbers are stark: just 36.1% of practices remain physician-owned. Hospitals and corporate entities acquired 85,000 physician practices between 2018 and 2026. Corporate entities, including insurers and private equity firms, grew their physician workforces by 92.3%, from roughly 77,800 to 149,600.

The pace is accelerating, not moderating. Since 2024 alone, 48,100 physicians left independent practice and 13,900 additional practices were acquired. In 2025, 29,600 physicians became hospital employees in a single year. In rural markets, independent physicians fell below corporate-employed physicians for the first time in 2024 — a threshold that signals how far the structural shift has extended beyond urban tertiary centers.

Corporate entities now own more physician practices than hospitals do: 33.2% versus 30.6%. The payer-provider vertical integration story — Optum, Humana, CVS absorbing primary care groups in high Medicare Advantage markets — is no longer a strategic trend to monitor. It is the operating environment.

What Employment Models Actually Cost Your Health System

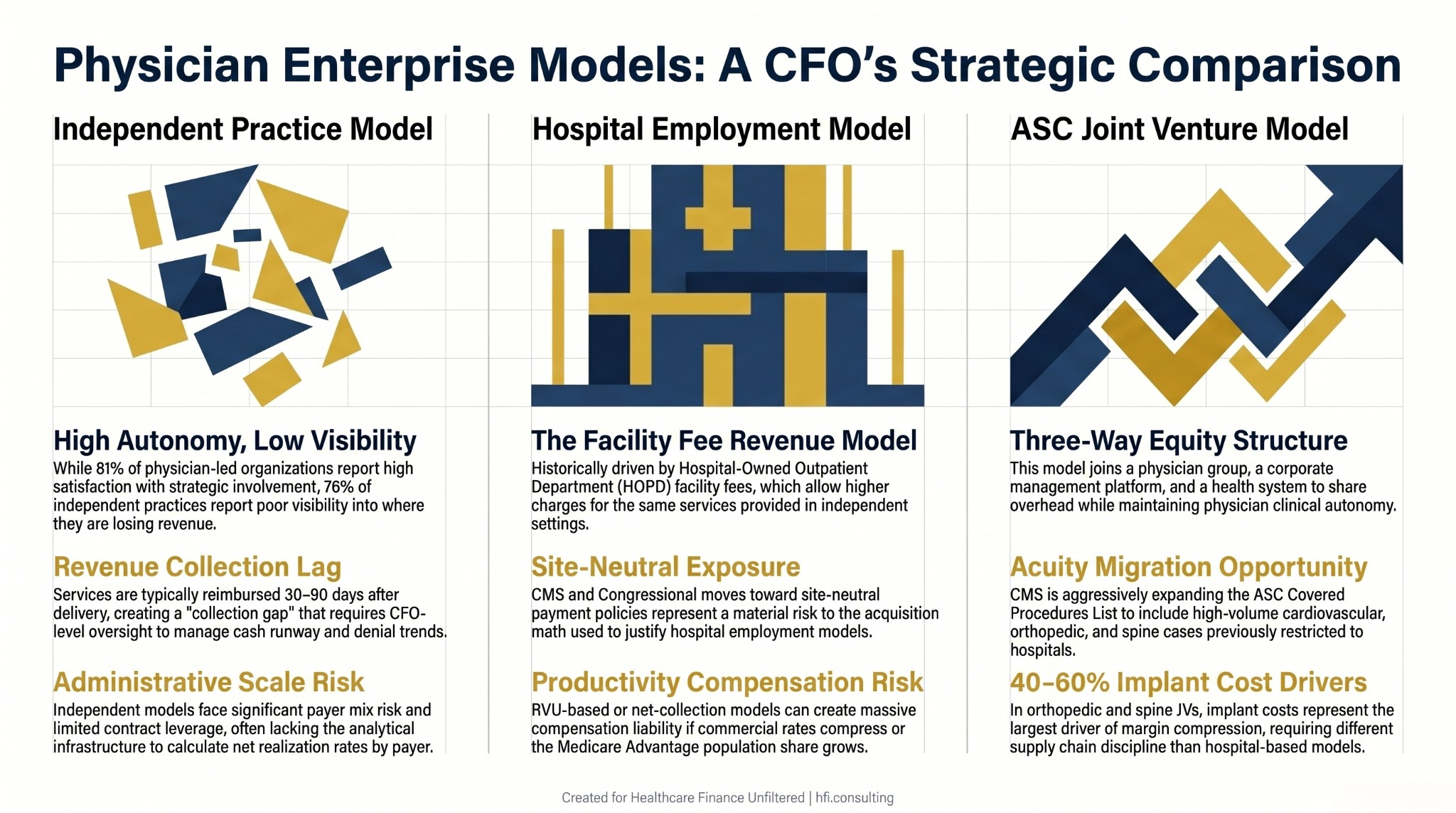

The headline narrative around physician consolidation focuses on strategic rationale: alignment, referral volume, network integrity. What receives less attention is the financial mechanics that follow an acquisition or employment model and whether CFOs are stress-testing the right assumptions before signing.

The structural problem is reimbursement asymmetry. Hospital-Owned Outpatient Departments can charge facility fees for the same services performed by a physician in an independent office setting. That revenue capture model is what made practice acquisition financially attractive to health systems for over a decade. It is also what Congress and CMS have been systematically eroding through site-neutral payment policies.

As a CFO, the acquisition math changes materially depending on how aggressively site-neutral policy advances. A practice generating favorable revenue under the HOPD facility fee model today may need to be re-underwritten entirely if the legislative landscape shifts. This is the scenario planning exercise most boards have not demanded yet.

Beyond reimbursement policy risk, physician compensation modeling is one of the most undermanaged financial risks inside a growing medical group or health system. When a practice brings on mid-level providers — NPs, PAs, additional physician partners — designing a compensation structure based on productivity, net collections, or Relative Value Units requires financial engineering the clinical leadership team is not built to do alone. If the model is too generous, it erodes margin. If it is too restrictive, the top performers leave.

Three-column chart comparing financial characteristics of independent practice, hospital employment, and ASC joint venture models for healthcare CFOs.

The ASC Opportunity Your CFO Team May Be Undermodeling

While the debate over physician-owned hospitals captures policy attention, the real financial opportunity in the physician enterprise space is playing out in Ambulatory Surgery Centers. And most health system CFOs are not modeling it aggressively enough.

ASC growth is being driven by two intersecting forces. First, CMS has continued expanding its ASC Covered Procedures List to include procedures that previously required hospital-level settings. High-volume cardiovascular procedures — electrophysiology studies, ablations, even percutaneous coronary interventions — have joined complex orthopedic and spine cases on the approved list. The acuity migration into the outpatient setting is no longer theoretical. It is CMS policy.

Second, the ownership model has evolved. The old 100% physician-owned ASC is giving way to three-way joint venture structures: a physician group, a corporate ASC management company or private equity platform, and a local health system. This model allows physicians to retain clinical control and equity upside while the enterprise partner absorbs payer contracting, supply chain management, and compliance infrastructure.

For health system CFOs, the JV structure deserves financial modeling on two fronts. First, as a strategic retention tool: physicians with ownership stakes in an ASC affiliated with your system are financially aligned in a way that employment alone cannot replicate. Second, as a direct revenue and margin play: the contribution margin profile of a well-structured ASC joint venture, particularly in orthopedic and cardiac service lines, can outperform the equivalent inpatient or HOPD model.

The implant cost dynamics inside an ASC are also worth specific attention. In orthopedic and spine cases, implant costs frequently represent 40-60% of total case cost and are the single largest driver of contribution margin compression. The financial discipline required to capture and manage implant costs at the ASC level is different from hospital-based supply chain management — and most JV governance structures underinvest in it at launch.

For a deeper framework on service line contribution margin and implant cost management, see Implant Costs Are a Contribution Margin Problem, Not a Billing Problem and Service Line Financial Assessment: The CFO's Framework for Capital Decisions That Actually Hold Up.

The Physician-Owned Hospital Legislative Environment: What CFOs Should Be Modeling Now

The political environment around physician-owned hospitals is more active than it has been in over a decade, and the TEAM model is the accelerant.

ACA Section 6001, enacted in 2010, effectively froze new physician-owned hospitals from billing Medicare and severely restricted expansion of grandfathered facilities. Because Medicare represents roughly half of inpatient days nationally, building a hospital without Medicare billing is financially non-viable. Physician-owned hospitals did not disappear; they redirected capital to the outpatient setting. But the legislative prohibition has remained in place.

Two bills are now in committee that would change that. HR 2191, the Physician Led and Rural Access to Quality Care Act, would allow physician ownership of rural hospitals more than 35 miles from a main campus or critical access hospital. HR 4002, the Patient Access to Higher Quality Health Care Act, takes a broader approach: repeal of the Stark physician self-referral whole hospital exception in its entirety. The American Medical Association led a sign-on letter with 90 co-signers urging passage.

The opposition is organized. The American Hospital Association argued in July that HR 4002 would result in additional gaming of the Medicare program and damage the safety-net provided by full-service community hospitals. The cherry-picking argument — that physician-owned facilities select healthier, higher-margin commercial patients and offload complex cases — has been the central objection for fifteen years. The AMA counters with a 2005 CMS study finding no consistent evidence that referrals were driven primarily by financial gain, and a 2019 Medicare data analysis finding total payments 8-15% lower at physician-owned hospitals for the most expensive diagnostic groups.

The more immediate signal is what CMS embedded in the proposed 2027 Hospital Inpatient Prospective Payment System rule: a formal request for information on physician-owned hospital participation in the Transforming Episode Accountability Model (TEAM). That RFI is not legislation, but it signals that CMS is at least stress-testing a world where physician-owned entities participate in mandatory bundled payment models. Public comments closed June 9.

For CFOs at full-service health systems, the scenario worth modeling is not whether HR 4002 passes this cycle, but what the market looks like if physician-owned competition re-enters your service area for high-margin elective surgical lines while you remain obligated to absorb uncompensated care, behavioral health, and trauma. That asymmetry is the real financial exposure.

For the TEAM model's direct financial implications, see Value-Based Payment Models 2026: Health System CFO Strategy Guide for TEAM and CJR-X.

The Independent Practice Financial Gap: Why 76% Cannot See Where They Are Losing Revenue

Despite the scale of consolidation, a countercurrent is emerging. A 2024 Bain survey found that 81% of physicians in physician-led organizations reported satisfaction with involvement in strategic decision-making, compared with just 50% in hospital-led practices. Some physicians are returning to ownership models specifically because of concerns over autonomy, compensation control, and burnout.

But the financial infrastructure of independent practice has not kept pace with clinical intentions. According to a March 2026 report from healthcare technology company Veradigm, only 24% of independent physician practices report high or complete visibility into where they are losing revenue. 54% said financial pressure increased over the prior 12 months.

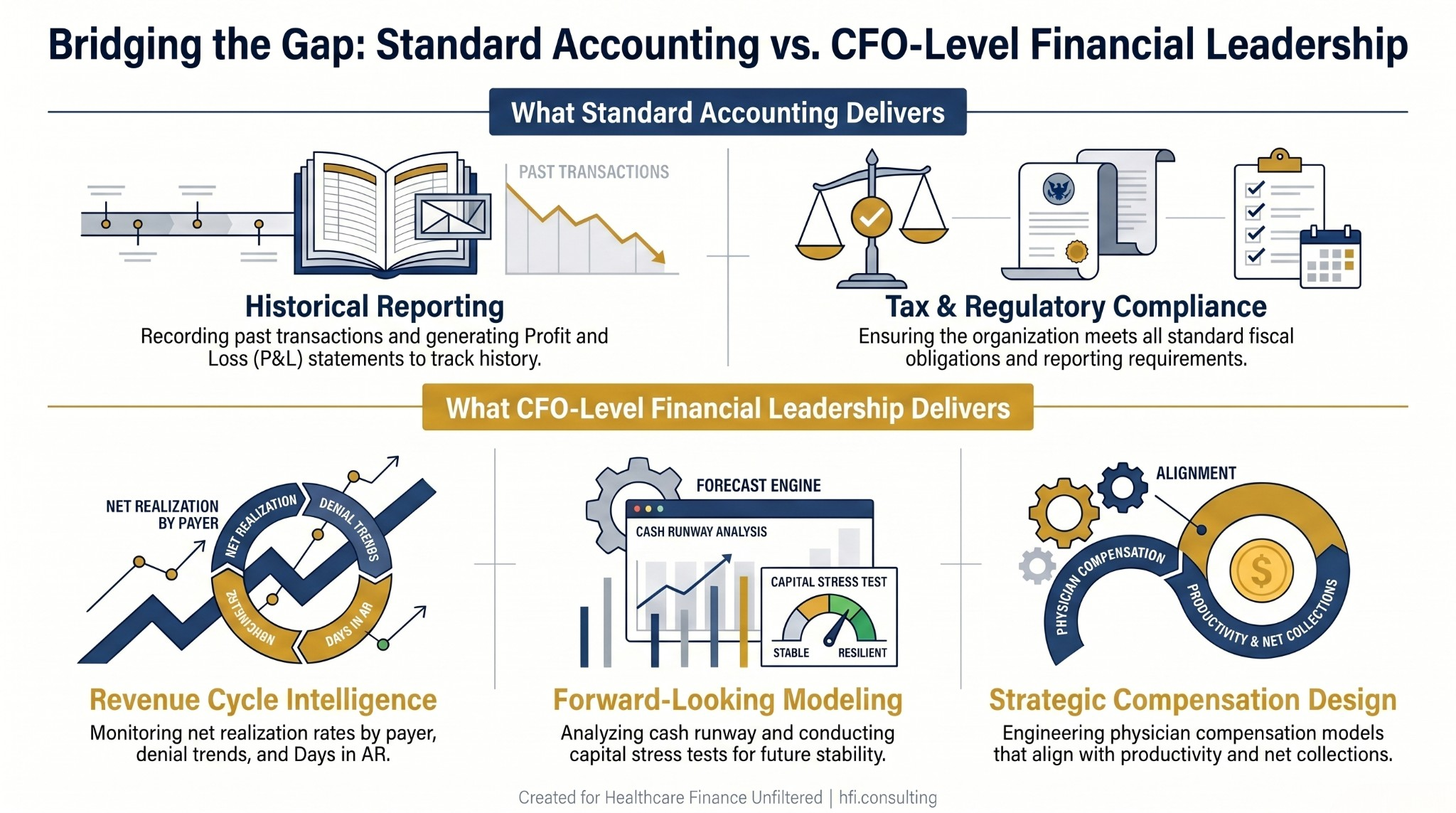

That gap between clinical independence and financial visibility is not primarily a technology problem. It is a financial leadership problem.

The structural difference between what a CPA provides and what a CFO-level function provides matters acutely in healthcare. A CPA records past transactions and manages tax compliance. A CFO-level function looks forward: cash runway modeling, net realization rate by payer, denial trend monitoring, Days in Accounts Receivable as a leading indicator of collection risk, and compensation modeling when a practice adds partners or mid-levels.

In a medical practice, services are delivered today and reimbursed — partially, conditionally — 30 to 90 days later, after a gauntlet of prior authorizations and denial cycles. Without CFO-level oversight of that lag, a practice can grow its patient volume and shrink its cash position simultaneously. Finance leaders who have worked on the payer side understand this dynamic directly: the collection gap is not a glitch in the system. It is how the system was designed.

The fractional CFO model has become the operational solution for independent groups and mid-size medical organizations that cross the $2-3 million revenue threshold where standard accounting is no longer sufficient. Engaging a specialized healthcare CFO for 15 to 25 hours monthly on a retainer basis provides access to forward-looking financial modeling, payer contract analysis, and boardroom-ready reporting without the overhead of a full-time executive salary.

For practices that cannot yet justify a full-time finance leadership position, this model is not a compromise. It is a structural advantage: the same analytical capability, aligned to what the practice actually needs at its current stage of growth.

Two-track diagram comparing standard accounting functions versus CFO-level financial leadership capabilities in healthcare organizations.

The CFO Action Framework: Four Questions for the Current Environment

Whether you are inside a health system managing physician enterprise strategy, a payer evaluating vertical integration, or a medical group finance leader trying to build visibility into revenue performance, the consolidation data reframes the same four questions.

1. What is your net realization rate by payer, by service line? Gross charges tell you almost nothing. Net realization rate by payer — the actual cash collected as a percentage of charges — tells you which contracts are sustainable, which need renegotiation, and which may need to be exited. Most practices and physician enterprise divisions do not have this data in a format that leadership can act on.

2. Is your physician compensation model stress-tested against payer mix shifts? If your RVU-based or net collections model was calibrated in a higher-reimbursement environment, and commercial rates compress or your MA population share grows, the model may produce compensation liability that no longer aligns with actual margin. This is not a hypothetical — it is a recurring problem in health system physician enterprise divisions.

3. Have you modeled the ASC JV contribution margin at the case level? A joint venture that looks favorable at the aggregate revenue line may be producing margin compression at the case level if implant costs, anesthesia arrangements, and post-discharge spending are not disaggregated. TEAM model bundled payment exposure extends 30 days post-discharge. Your JV contribution margin model needs to extend there too.

4. What is your physician enterprise strategy if HR 4002 passes or CMS expands TEAM to include POHs? Even in a low-probability scenario, the scenario planning exercise has value: it identifies which service lines carry the most payer mix and margin concentration, and which are most exposed to physician diversion to a competing ASC or ownership model.

"The financial operating system of healthcare is fundamentally different from any other sector. Physicians deliver a service today and hope to collect a fragmented portion of it 30 to 90 days from now, after fighting a gauntlet of prior authorizations and denials. That lag, unmanaged, is how practices grow themselves into financial distress."

For more on medical group revenue cycle infrastructure in the high-deductible era, see Medical Group Revenue Cycle: CFO and Director Strategies for the High-Deductible Patient Era.

The Structural Shift Is Not Going to Reverse. The Financial Leadership Has to Catch Up.

The consolidation wave is well-documented. The legislative environment around physician-owned hospitals is live and moving. The ASC opportunity is real and currently undercapitalized by most health systems' JV frameworks. The independent practice financial gap — 76% of groups without adequate revenue visibility — is producing exactly the downstream failures the data predicts.

What is less documented is how few finance teams have recalibrated their frameworks to match the environment they are now operating in. The physician enterprise is the most financially complex and highest-growth segment of most health systems' operating structures. It deserves analytical infrastructure to match.

If your organization is building or restructuring a physician enterprise division, entering an ASC joint venture, or navigating the financial infrastructure of a growing medical group, the financial modeling and payer contract analysis work requires a specific kind of operational expertise. HFI Consulting works with health systems, payers, and medical groups on the financial frameworks that make these structures sustainable. Start at hfi.consulting.

Practical Starting Points for Finance Leaders This Quarter

The four-question framework above produces a near-term action list. For most finance leaders, the implementation sequence looks like this.

Start with revenue visibility. If you do not have net realization rate by payer in a format you can present to the CFO or board, that is the first gap to close. Your billing system has the data. The question is whether it has been organized into a framework that drives decisions rather than just reports history.

Then move to compensation model review. Pull your physician and advanced practice provider compensation model and stress-test it against two scenarios: a 5% reduction in your dominant commercial rate, and a 10-point increase in Medicare Advantage share. If either scenario produces unbudgeted compensation liability, you have a structural problem that is better addressed now than when payer negotiations are already underway.

Then set a calendar item for your managed care contracting team. Not the annual contract review cycle. A quarterly clause-level briefing that includes anti-steering language, tiering restrictions, and any provisions that may carry antitrust exposure. The DOJ enforcement environment has made that a CFO-level risk question.

Healthcare Finance Unfiltered publishes weekly operational analysis for CFOs, VPs of Finance, and healthcare finance leaders navigating the strategic and operational challenges of the current environment. If this framework was useful, subscribe at rachelbarksdale.substack.com for weekly analysis delivered to your inbox.

P.S. For health system CFOs, payer finance leaders, and medical group directors: where is your organization in the physician enterprise financial infrastructure conversation? Are you ahead of the structural shift, or still working from frameworks built for a less consolidated market? Hit reply and tell me — the patterns across organizations often point to the next piece worth writing.