Retail Health Partnerships: The CFO's Guide to What Works, What Failed, and What's Coming Next

Amazon One Medical is winning. Walgreens lost $5.8B. CVS owns Aetna. The financial model explains everything.

Retail health is not a trend anymore. It is a structural shift in how primary care gets delivered, and your health system is going to be asked to take a position on it. Four of the largest retail and pharmacy brands in the country spent a combined tens of billions of dollars trying to crack this model. The ones still standing did not get lucky. They built a financial structure that could actually survive.

The ones that failed had the same access story. They just never solved the economics behind it.

The Access Problem Is Real, and Retail Moved Faster Than Health Systems Did

Physician shortages, long wait times, and geographic gaps have made access one of the defining operational challenges for health systems in this decade. Retail platforms saw this before most health systems did, and they moved at a pace that healthcare organizations rarely match.

Amazon One Medical has built a specialty care referral network connecting approximately 20 health systems across the country to its primary care membership model. Amazon handles primary care access and membership. When patients need specialist services, surgery, or inpatient admission, they are referred into the health system partner's network.

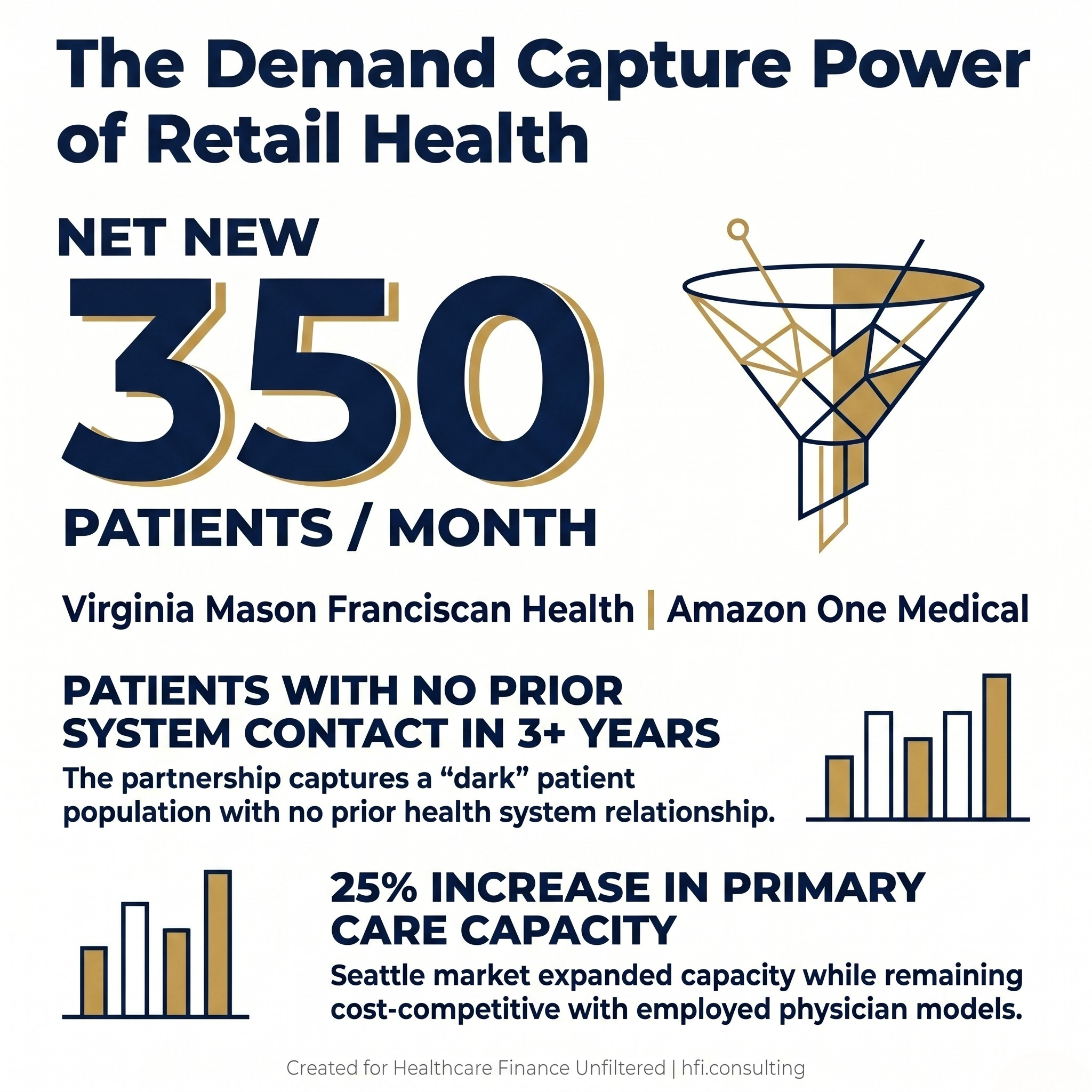

The results are real. Virginia Mason Franciscan Health in Seattle works with roughly 35 One Medical primary care providers and brings in approximately 350 net new patients per month, patients who had not used the health system in the previous three years. That partnership has increased total primary care capacity in the Seattle market by more than 25% while remaining cost-competitive with the system's employed physician model.

Rush University System for Health in Chicago launched its Amazon One Medical partnership on January 1 and received more than 20 specialty care referrals from One Medical patients within the first weeks. Rush's chief strategy officer described the arrangement as augmenting their existing strategy, noting that not every patient wants to access care the same way.

That framing is the right one. The health systems finding success in these partnerships are treating them as demand capture tools, not substitutes for their core delivery model.

Infographic showing Virginia Mason gaining 350 net new patients per month through Amazon One Medical

CVS Has an Advantage No One Else Can Copy: It Owns the Insurer

CVS operates more than 1,000 MinuteClinic locations across 40 states, and more than 65% of those locations now offer adult primary care through affiliations with health systems and payers. On the surface, this looks like a distribution partnership. Under the surface, it is a fundamentally different financial structure than anything Walmart or Walgreens attempted.

CVS owns Aetna.

That is not a minor detail. Because CVS controls a major insurance carrier, it can incentivize Aetna members to visit a MinuteClinic at low or zero copay. The insurer saves money by keeping the patient out of an expensive emergency room. CVS captures the pharmacy revenue when the prescription is filled twenty feet from the exam room. The downstream dollars do not escape. They circulate inside the same corporate structure.

This is what the healthcare industry calls a payer-provider loop, and it is the single most durable competitive advantage in retail health. Without an insurance engine driving patients to the door and capturing the downstream revenue, a retail clinic bleeds cash. With it, the math works. For a deeper look at how health systems are evaluating whether to build this loop themselves, see the full analysis of provider-sponsored health plans at hfi.consulting.

The Hartford HealthCare partnership, effective May 7, adds in-network adult primary care services at all 20 Connecticut MinuteClinic locations, with same-day and next-day appointments, evening and weekend hours, and care coordination through a shared EHR. MinuteClinic patients who need hospitals, specialists, diagnostic services, or advanced imaging are referred into Hartford HealthCare's system.

The Mass General Brigham partnership takes the model further, proposing to transform 37 MinuteClinic locations into MinuteClinic Primary Care sites placed inside Mass General Brigham's provider network and payer contracts. The Massachusetts Health Policy Commission published a 66-page analysis in April projecting that the arrangement could raise annual healthcare spending by $40 million after the first three years. Both CVS and Mass General Brigham have pushed back, arguing the analysis does not account for longer-term reductions in total cost of care.

That dispute is a preview of the regulatory friction these arrangements are going to face at scale.

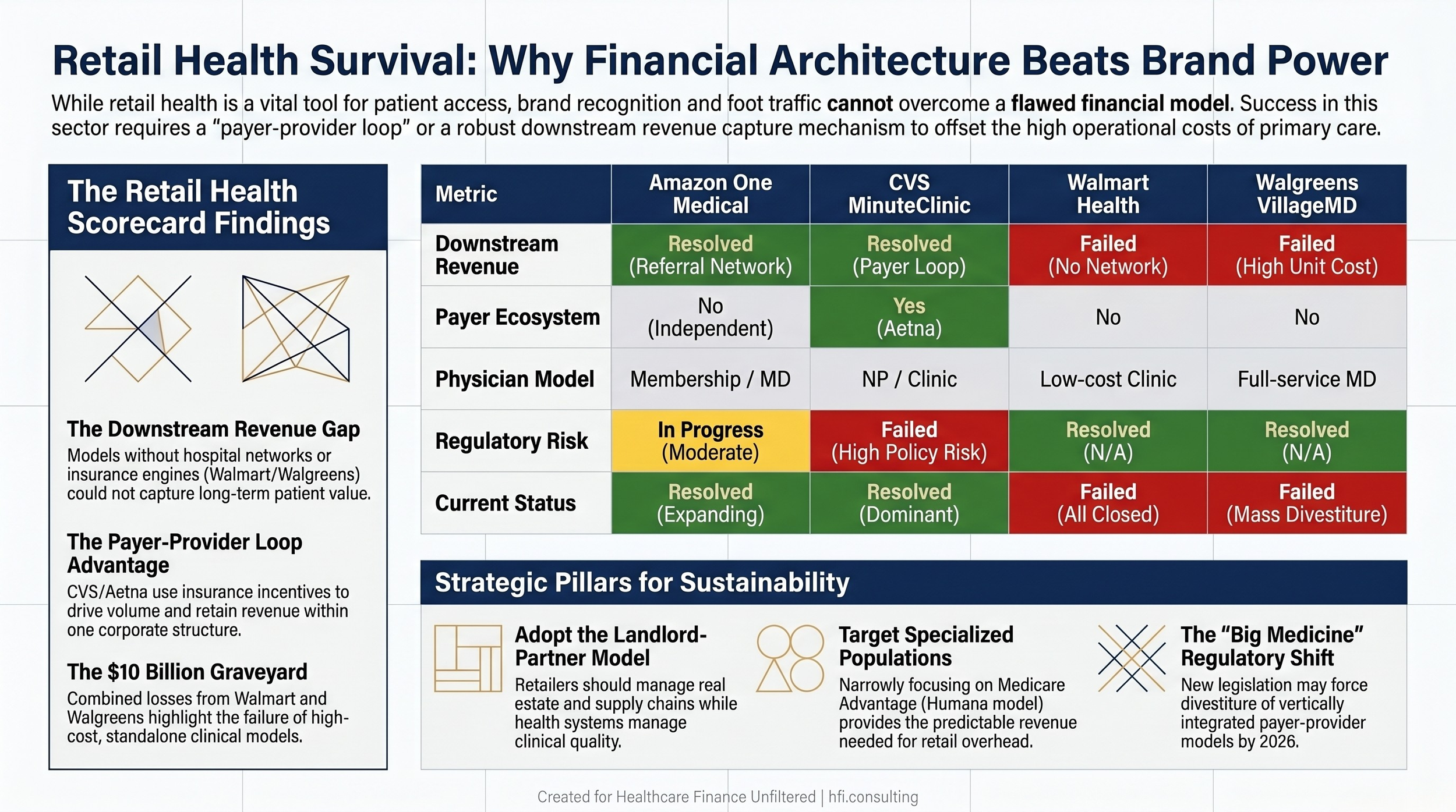

Scorecard comparing Amazon One Medical, CVS MinuteClinic, Walmart Health, and Walgreens VillageMD across five financial and operational dimensions

The Political Horizon: Breaking Up Big Medicine

Health system CFOs need to track one more variable that most retail partnership analyses ignore: the regulatory environment around vertical integration is shifting.

A bipartisan coalition of Senators Elizabeth Warren and Josh Hawley introduced the Break Up Big Medicine Act, targeting the vertical integration that gives companies like CVS and UnitedHealth their structural advantages. The bill reflects a broader policy consensus that the combination of insurer, pharmacy benefit manager, and care delivery under a single corporate roof creates financial conflicts that drive up costs and limit patient choice.

The regulatory pressure is already moving through multiple channels simultaneously. Federal PBM reform embedded in the 2026 Appropriations Act mandates delinking, requiring PBMs to base fees on flat service charges rather than a percentage of drug list prices. If that incentive structure changes, the financial rationale for owning both a PBM and a retail pharmacy weakens. The FTC settlement with Express Scripts has already forced structural changes to how that PBM handles drug pricing, requiring patient out-of-pocket costs to be calculated on net drug cost rather than inflated list price. Expansions of any-willing-provider laws at the federal and state level are targeting the patient steering that makes owning both the PBM and the pharmacy network so valuable.

If sweeping legislation passes, the framework experts propose looks like a healthcare Glass-Steagall: a company could own only one of three things. An insurer. A pharmacy benefit manager or distributor. Or a care provider. Companies holding entities in more than one category would be legally required to divest.

That scenario changes the CVS competitive advantage calculation entirely. Finance leaders evaluating long-term retail health partnerships need a scenario in their planning model that accounts for regulatory-forced structural change, not just current market conditions. The full analysis of the DOJ antitrust crackdown and its implications for payer contracts is available at hfi.consulting.

This section is not an argument for or against the policy direction. It is a planning input. The financial logic of a ten-year retail partnership agreement looks different if the payer-provider loop that makes it work becomes legally untenable in year five.

The Three Things That Make Retail Health Actually Work

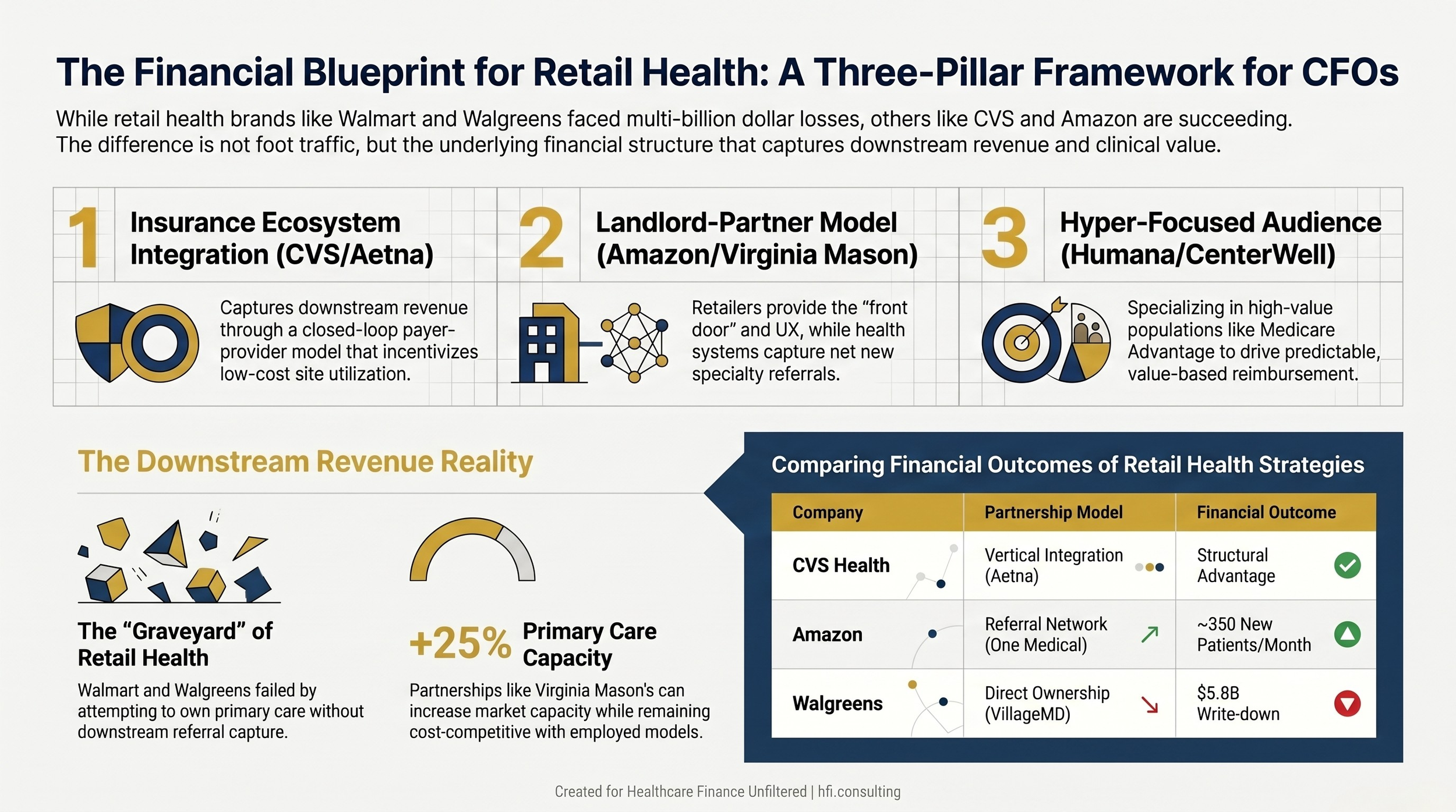

The wreckage of Walmart and Walgreens and the success of Amazon One Medical and CVS point to the same three structural requirements.

The first is insurance ecosystem integration. A retail clinic cannot survive on cash payments or standard, low-margin insurance reimbursements alone. The CVS model works because Aetna drives the patient volume and captures the downstream savings. Without that loop, or a health system partner that provides an equivalent downstream revenue capture mechanism, the numbers do not work.

The second is accepting the landlord-partner model. Retailers are excellent at supply chains, real estate, and consumer convenience. They are consistently poor at managing physicians, medical billing, and clinical quality. The winning play for retail players is leasing space to trusted regional health systems, capturing guaranteed lease income and foot traffic without the medical liabilities. The health system gets a highly visible front door to capture new patients. Virginia Mason and Rush are operating inside this model. Walmart and Walgreens were trying to be the healthcare provider themselves.

The third is a hyper-focused target audience. Trying to serve everyone, from toddlers with ear infections to complex diabetic patients, is a financial nightmare in a retail footprint. The models that survive are specialized. Humana's conversion of the Walmart spaces into Medicare Advantage-focused senior primary care clinics works because value-based care for a defined senior population produces predictable per-member revenue that can support the overhead of a retail space. For a full breakdown of value-based payment model economics, including how CFOs should evaluate per-member fee structures, see the VBC framework at hfi.consulting.

Three-pillar framework for retail health partnership financial viability showing insurance integration, landlord-partner model, and hyper-focused audience requirements

For health system finance teams currently evaluating or negotiating retail partnership agreements, building the financial model before signing is not optional. At HFI Consulting, I work with health system CFOs on partnership economics, including downstream revenue modeling, payer mix impact analysis, and regulatory scenario planning for partnerships that cross payer and provider lines. If this is on your planning agenda, reach out at hfi.consulting.

The Bottom Line

The access story behind retail health partnerships is real. Virginia Mason is adding 350 net new patients per month. Hartford HealthCare is extending primary care capacity across Connecticut. These are not marketing results. They are volume metrics with downstream revenue implications.

But the financial model underneath the access story has to work independently of the brand name on the building. Walmart had more foot traffic than any health system in the country. Walgreens invested more than most health system capital budgets on physician-based primary care. Neither of them solved the downstream revenue problem.

The health systems winning in retail partnerships understood the financial structure before they signed. The ones evaluating proposals right now need to apply the same lens.

Model the downstream revenue first. Assess the payer mix implications. Build the regulatory scenario. Then decide whether the access story is worth telling.

Want a financial model template for evaluating retail health partnership economics? Subscribe to Healthcare Finance Unfiltered at hfi.consulting.

P.S. Has your health system been approached by a retail health platform, or are you watching a partnership competitor take shape in your market? I would like to hear how CFOs are thinking about the downstream revenue question. Hit reply and let me know.