The Most Underpaid, Underappreciated Role in Hospital Finance: Who Should Be Running Your Medicare Cost Report

The shifting rules on allowable costs are making the cost report a seven-figure risk management function.

CMS just tightened its documentation guardrails on organ acquisition costs again. MAC auditors are scrutinizing executive compensation against regional benchmarks. And the gray areas around telehealth infrastructure, GME site eligibility, and what counts as a "reasonable" administrative cost have never been more contested. If your Medicare Cost Report is sitting with someone who views it as an annual filing exercise, your health system is carrying a compliance and revenue risk that your board has probably never been briefed on.

Infographic showing four financial risk categories tied to the Medicare Hospital Cost Report for health system CFOs

The Cost Report Is Not a Tax Return. Stop Treating It Like One.

Every Medicare-certified hospital files Form CMS-2552-10 annually with its Medicare Administrative Contractor within five months of fiscal year end. Most CFOs know this. What far fewer CFOs have fully mapped is what the cost report actually controls.

It is the mechanism for final reimbursement reconciliation. Uncompensated care and DSH adjustments flow through it. Direct and Indirect Graduate Medical Education funding is calculated from it. Cost-to-Charge Ratios are built from it, and CMS uses those ratios nationally to translate hospital charges into actual costs when setting MS-DRG relative weights.

This is not a filing. It is a multi-million-dollar federal negotiation that happens once a year, gets audited for up to two years, and requires a CFO or Chief Administrator to certify it under penalty of federal law.

That scope deserves a different level of ownership than most health systems are currently providing.

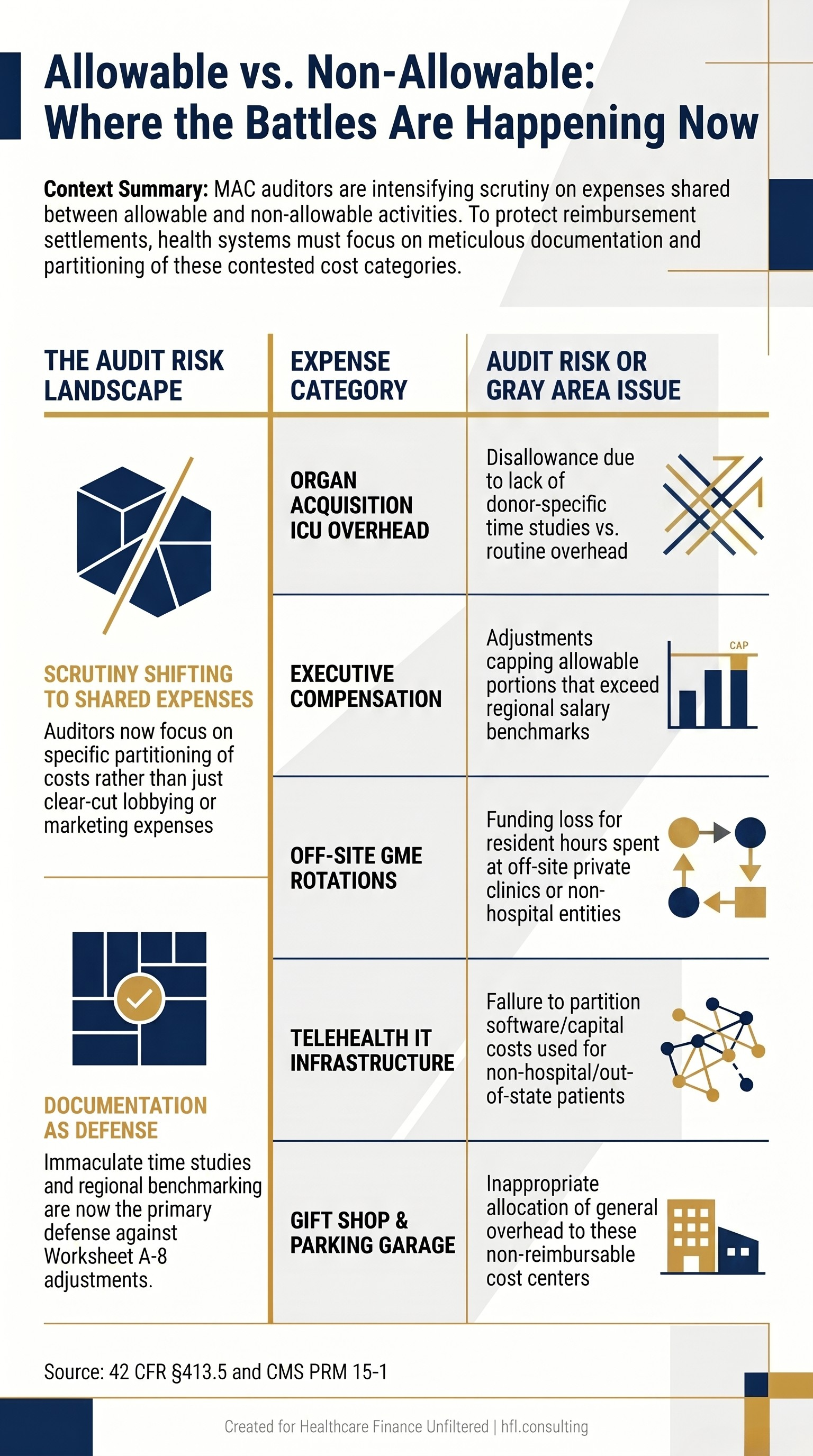

What Is Actually Changing on the Allowable Cost Side

The line between what Medicare will reimburse and what it will not has always required technical precision. What has changed is the volume and specificity of scrutiny coming from MAC auditors.

A few years ago, the bigger battles were over marketing expenses, lobbying costs, and physician private practice overhead. Those lines are well-established. The areas where enforcement is intensifying involve expenses that are genuinely shared between allowable and non-allowable activities.

Organ acquisition is one of the clearest examples. CMS reimburses organ procurement on a cost basis to encourage transplantation. But if a hospital cannot produce immaculate time studies separating donor-specific ICU costs from routine hospital overhead, the MAC will disallow the reimbursement. The documentation burden has increased substantially, and the financial stakes at transplant-designated facilities are significant.

Executive compensation is another active battleground. MAC auditors use regional salary benchmarks. A rural facility paying a compensation package more consistent with a major academic medical center will see Worksheet A-8 adjustments that cap the allowable portion. That is not a hypothetical. It is an adjustment that shows up in settlements.

Teaching hospital GME funding carries its own complexity. Resident hours must be documented to specific allowable care sites. A rotation through an off-site private clinic or hours spent on administrative functions for a non-hospital entity removes those hours from the calculation. Diluting your resident count has a direct funding impact.

And then there is telehealth. The clinical delivery of telehealth is folded into standard payment models, but the IT infrastructure behind it is not. Software licensing, remote monitoring equipment, and capital costs for platforms used heavily for out-of-state or non-hospital clinic patients must be carefully partitioned. If that partitioning does not happen, the MAC will do it for you at audit.

Comparison table showing Medicare cost report allowable vs. non-allowable expense categories and current audit risk areas for hospital CFOs

What This Role Actually Requires

The person managing this function is operating across four dimensions simultaneously.

They are doing technical compliance work: maintaining Worksheet A, executing the step-down allocation through Worksheet B, calculating Cost-to-Charge Ratios on Worksheet C, and ensuring Worksheet A-8 adjustments are both complete and defensible.

They are doing audit defense work: building the documentation record that a MAC auditor will review over the next two years, knowing federal statute well enough to counter proposed adjustments, and having the executive presence to negotiate outcomes.

They are doing strategic revenue work: understanding how changes in wage index, geographic CBSA classification, special designations, and annual IPPS rule updates will affect net revenue over a three-to-five-year horizon.

And they are doing internal education work: translating cost report implications into language that a CFO can brief to a board, a service line director can act on, and a compliance team can implement.

That is a materially different job description than "files the cost report."

HFMA recognized this gap when they launched the Certified Hospital Cost Report Specialist (CHCRS) designation in partnership with Forvis Mazars. The program is designed specifically to build the next generation of cost report professionals, and it reflects an industry-wide acknowledgment that this expertise has been systematically undertrained for years. The CHCRS covers all primary cost report worksheets, Medicare special designations, wage index, clinic strategies, and the settlement process.

The fact that the designation was new enough that Sam Antonios, MD, became its first certificant in late 2024 tells you something about how long this gap has existed without a formal credential pathway.

Why a Former Hospital Cost Accountant Is One of the Best Fits for This Role

This transition is more natural than most finance leaders realize, and it is worth naming explicitly because the pipeline for this role needs to be wider.

A hospital cost accountant already understands Worksheet B at a structural level. They have spent years building relative value units, conducting time studies, and allocating administrative, dietary, and housekeeping overhead to clinical service lines. The logic of the step-down method is not foreign to them. They have been living it from the inside.

They know how the hospital breathes. They understand how clinical departments consume resources, how general ledger data flows into management accounting structures, and how systems like Epic and StrataJazz surface the underlying cost information that feeds the cost report. That operational fluency is not something you can teach in a CMS manual.

What they need to add is the regulatory framework. The Provider Reimbursement Manual (PRM 15-1) replaces GAAP as the governing logic. The question shifts from "what is the right cost" to "what does CMS define as an allowable cost," and those two answers frequently diverge. Audit defense requires regulatory confidence, not just accounting accuracy.

The strategic forecasting dimension is also a genuine skill expansion. Cost accountants are oriented toward historical accuracy and variance analysis. Reimbursement leadership requires forward modeling: how does a shift in CBSA classification affect your wage index? What does a change in resident count do to DGME funding over three budget cycles? That is a different analytical posture, and it takes time to develop.

In my cost accounting work at Ascension across seven hospitals, the finance professionals who understood departmental cost flow at a granular level moved faster, caught errors earlier, and built better business cases than those who came strictly from a billing or general accounting background. That same advantage transfers directly into cost report work. The step-down allocation is familiar territory. The transition is a matter of adding regulatory fluency to operational knowledge that is already strong.

If you are a CFO building succession plans or evaluating whether your current cost report function has the right leadership, the question is not whether the report was filed. The question is whether the person filing it can walk into a MAC audit and defend every line.

Framework diagram showing skills healthcare cost accountants already have versus new competencies needed for a Medicare cost report director role

What the Reimbursement Function Needs to Look Like

The DSH and uncompensated care adjustments that flow through the cost report are a direct function of how well this role is executed. For safety-net hospitals, that is not a secondary concern. It is foundational to the mission funding model. You can read more about the financial stakes of DSH-related settlements in the DSH Lawsuit 2026 analysis at hfi.consulting.

The same applies to service line finance. The Cost-to-Charge Ratios built from your cost report directly influence how CMS values the services your highest-margin lines deliver. If your CCRs are inaccurate, your service line financial assessments are built on a flawed foundation. The Service Line Financial Assessment CFO Framework addresses exactly that problem at the operational level.

At a minimum, the reimbursement function should include:

Annual CCR review before submission, with documentation of any significant shifts from prior year

Worksheet A-8 audit conducted by a qualified internal or external reviewer before certification

MAC audit preparation protocol that begins at submission, not when the auditor arrives

Multi-year forecasting model that incorporates wage index trends, IPPS rule updates, and GME resident count projections

CFO briefing that translates cost report outcomes into board-level financial risk language

The last point matters more than most CFOs expect. The cost report carries a certification requirement under 42 CFR §413.20(b). If a hospital fails to file by the five-month deadline, the MAC can suspend all interim Medicare payments and deem prior payments as overpayments. That is not a compliance detail. It is a liquidity event.

If you are evaluating whether your current cost report function has the depth it needs, or if you are building a reimbursement leadership role from scratch, the team at HFI Consulting works with health systems on exactly these organizational and financial risk questions. Visit hfi.consulting to start the conversation.

What Happens When You Outsource the Whole Thing

Some health systems do not have a reimbursement director at all. They contract the work annually to a consulting firm or a Big Four advisory team, the report gets filed, and the engagement closes until next year. For certain organizations, that arrangement is a legitimate choice. For others, it is a risk posture that no one formally decided to take.

The honest framing is this: a contractor can file an accurate report. What they cannot do is carry institutional knowledge across fiscal years, maintain the documentation infrastructure that MAC auditors will want to review two years from now, or walk into your October leadership meeting to flag that a new telehealth platform contract is going to create a partitioning problem on next year's cost report.

That continuity gap is where outsourced-only models consistently underperform. The filing is correct. The strategic function is absent.

There is a real use case for outsourcing. Critical access hospitals with lean finance teams, organizations in the middle of a leadership transition, and smaller independent facilities that genuinely cannot justify a full-time director-level FTE are all reasonable candidates. The model works when it is paired with an internal owner who understands enough to manage the contractor relationship, review the output, and translate the implications upward.

What does not work is treating the annual contractor engagement as a substitute for institutional cost report competency. When the MAC auditor arrives, they are not auditing the contractor. They are auditing the hospital. The CFO is the one signing the certification. The liability stays in-house regardless of who prepared the worksheets.

If your current model is full outsourcing, the right question is not whether to bring it entirely in-house. It is whether you have someone internal who owns the function at a strategic level, even if the technical preparation is contracted out. That single point of accountability changes the risk profile significantly.

The Workforce Pipeline Problem Is Bigger Than One Role

HFMA's decision to launch the CHCRS reflects something real: the cohort of professionals who built cost report expertise over decades is retiring, and there has not been a structured pathway to replace them.

The clinical revenue cycle has absorbed most of the talent investment in healthcare finance over the past ten years. Denials management, prior authorization, AI-driven coding tools. That investment has been directionally correct given payer pressure. But it has come at the cost of institutional knowledge on the federal cost reporting side.

Health system CFOs who are serious about workforce planning should be asking two questions.

First: who in your current finance organization has the foundational skills to develop into a cost report leader? Cost accountants, budget analysts with deep operational experience, and reimbursement staff who have been filing support roles are all viable starting points. The CHCRS certification gives them a structured pathway to build the regulatory competency they are missing.

Second: is the reimbursement director role in your organization structured to attract and retain the right talent? This function carries multi-million-dollar implications. If it is compensated and positioned as a compliance coordinator role, you will attract compliance coordinators.

The Hospital Workforce Cost Control CFO Guide gets into the broader compensation strategy framework. The core principle applies directly here: the cost of underpaying a high-impact finance role shows up in your settlements, not your salary budget.

The Medicare Cost Report Is a Multi-Million Dollar Negotiation. Is the Right Person Running It?

Who Should Own This Role Going Forward

The short answer: someone who understands both sides of the ledger. The federal ledger, where CMS defines what is allowable and what is not. And the operational ledger, where clinical departments generate the costs that flow through the worksheets.

A former hospital cost accountant with regulatory training is often the strongest candidate in the market right now, precisely because that combination is rare. The operational fluency is hard to teach. The regulatory framework, while complex, is learnable. The CHCRS certification is a useful signal that the regulatory work has been done at a documented level of rigor.

CFOs who are evaluating this role, or who are considering whether their current reimbursement function needs restructuring, are welcome to reach out directly through hfi.consulting. These are the exact conversations the consulting practice is built around.

P.S. Who owns the Medicare Cost Report at your organization? Is it a dedicated reimbursement director, a shared function, or something that gets handed off at year-end? Hit reply and tell me what that structure looks like. I am genuinely curious how this is being handled across different health system sizes, and the patterns are worth a follow-up piece.