Rural Hospital Turnaround: The CFO Finance and Grant Strategy Guide for Staying Open

What separates rural hospitals that survive from those that close comes down to finance strategy, not just federal funding.

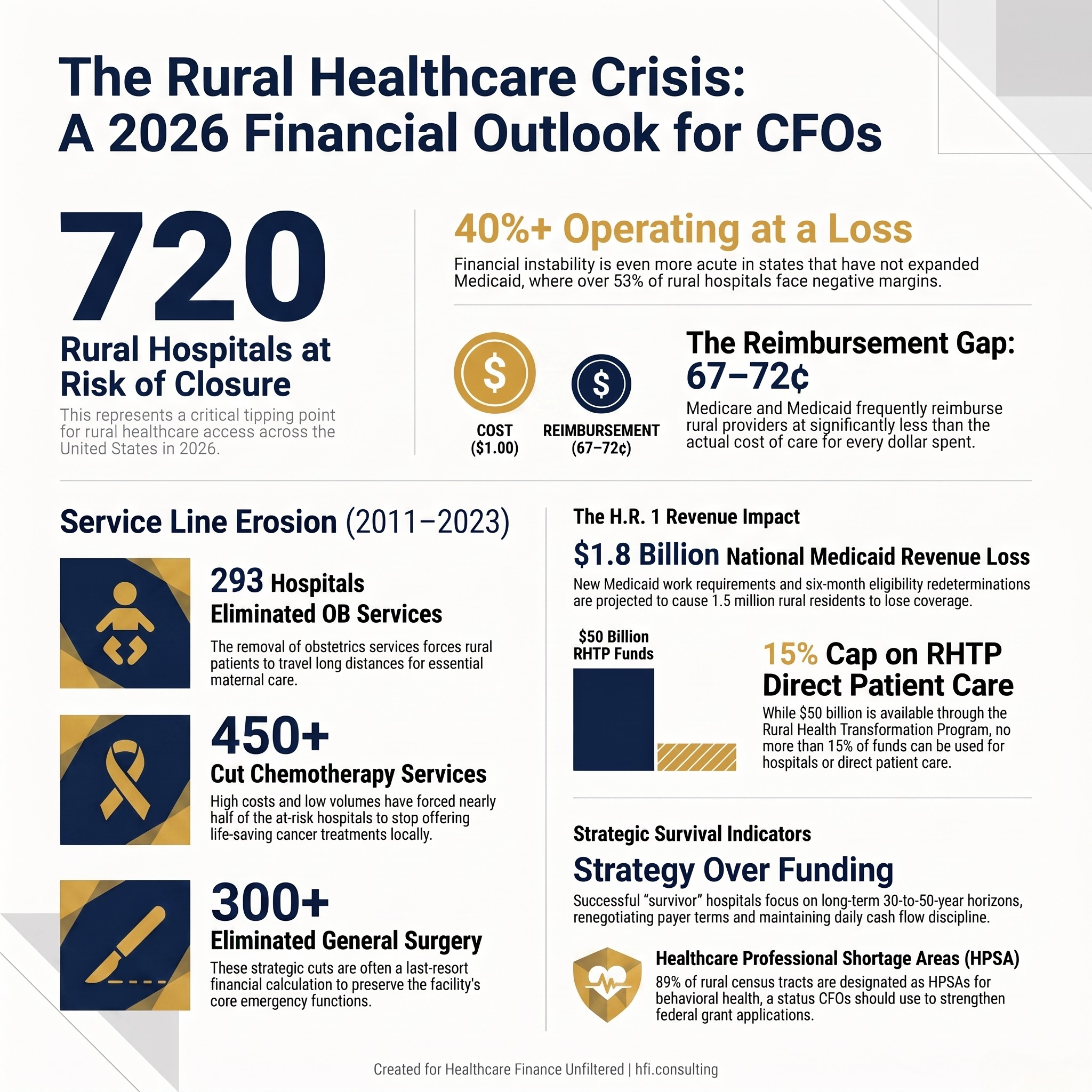

Seven hundred twenty rural hospitals are currently at risk of closure in the United States. One of them shut its doors last month after 101 years of serving its community. The question healthcare finance leaders need to answer right now is not whether this crisis is real — it is — but whether your organization has a financial strategy to survive it or is simply waiting for the next grant cycle.

Infographic showing 720 rural hospitals at risk of closure in the US with key statistics on rural hospital financial distress in 2026.

The Numbers Healthcare Finance Leaders Cannot Ignore

Over 40 percent of rural hospitals are currently operating at a loss. In states that have not expanded Medicaid, that number climbs above 53 percent. These are not projections. These are the current operating conditions for facilities that are serving as the sole source of acute care for their communities.

Between 2011 and 2023, 293 rural hospitals stopped offering obstetrics services. More than 424 cut chemotherapy. More than 300 eliminated general surgery. Every one of those decisions was a financial calculation made by a CFO or board facing the same fundamental problem: the revenue model that funds urban hospital care does not translate to low-volume, high-fixed-cost rural operations.

Medicare and Medicaid, the dominant payers for rural hospitals, frequently reimburse at 67 to 72 cents on the dollar relative to actual cost of care. A larger share of rural than urban patients are enrolled in Medicare Advantage plans, which carry lower provider payment rates and higher claims denial rates than traditional Medicare. The math does not work at scale, and it does not work in isolation either.

For context on how rural hospitals sit within the federal payment system, the six Medicare rural hospital designations — Critical Access Hospital, Low-Volume Hospital, Rural Emergency Hospital, Rural Referral Center, Medicare-Dependent Hospital, and Sole Community Hospital — each carry distinct payment mechanisms and eligibility requirements. Critical Access Hospital status, held by 59 percent of rural hospitals, reimburses at 101 percent of Medicare allowable costs. That sounds favorable until you account for the fixed cost reality on the ground.

If you are managing a Critical Access Hospital or any facility operating under one of these designations, the foundational financial analysis belongs in the Critical Access Hospital CFO Toolkit I published earlier this year. That piece covers margin strategy, AI applications, and the financial controls framework CAH finance leaders need before the next budget cycle.

H.R. 1 Has Changed the Math — Again

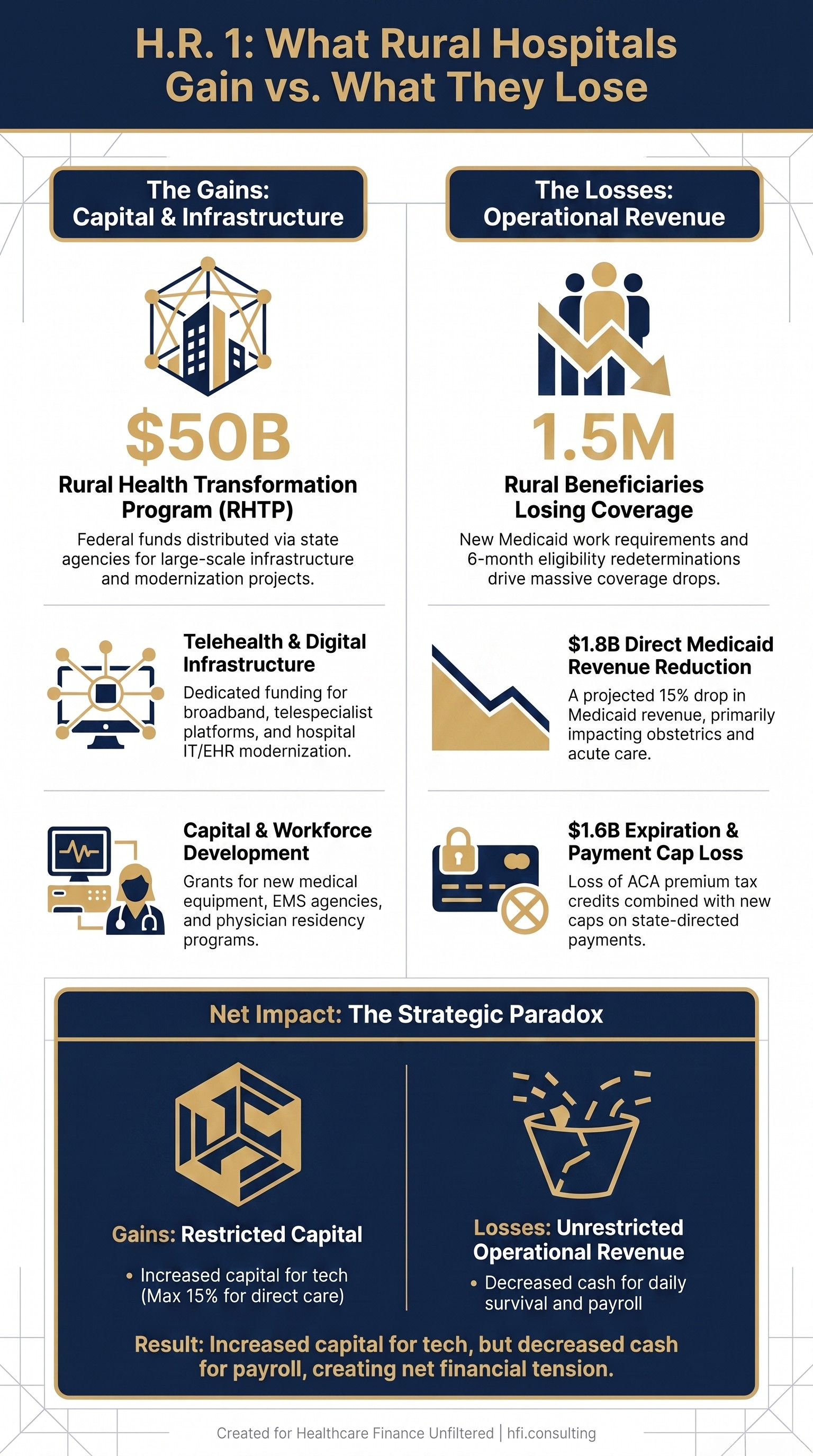

The 2025 budget bill created the Rural Health Transformation Program, a $50 billion federal initiative distributed through state agencies. It also introduced Medicaid changes that will hit rural hospitals harder than urban systems, and that dual reality is what every rural CFO needs to model before the end of this fiscal year.

H.R. 1 provisions affecting rural Medicaid revenue are significant. Medicaid work requirements will require beneficiaries to regularly verify employment status to remain enrolled, with states redetermining eligibility every six months instead of twelve. Projections indicate 1.5 million rural Medicaid beneficiaries will lose coverage as a result. A 15 percent reduction in Medicaid revenues would strip over $1.8 billion from rural hospitals nationally, with disproportionate impact on obstetrics departments where nearly half of all rural births are Medicaid-covered.

New caps on state-directed payments are expected to accelerate closures. These caps limit state Medicaid programs' ability to offer enhanced payments to rural hospitals — one of the primary mechanisms states have used to offset the gap between Medicaid rates and actual cost of care. Combined with the expiration of ACA enhanced premium tax credits at the end of 2025, rural hospitals could lose an additional $1.6 billion in patient revenue.

This is the policy context finance leaders need to carry into any budget conversation. For a detailed look at how Medicaid structural changes are affecting hospital financial planning more broadly, the earlier piece on Rural Hospitals Already in the Red covers the pre-H.R.1 baseline that makes these new cuts even more consequential.

Framework comparing H.R. 1 funding gains versus Medicaid and ACA revenue losses for rural hospitals in 2026.

The RHTP Funding Window Is Open — But It Requires Active Management

The Rural Health Transformation Program represents the largest single federal investment in rural health infrastructure in recent history. States are moving quickly. Kansas awarded nearly $80 million to 39 organizations in June alone. Nevada distributed $36 million in first-round grants. Colorado released $160 million in applications. Oregon awarded $97 million to 136 local projects.

The funding categories vary by state but follow consistent themes: telehealth infrastructure, capital equipment modernization, EMS workforce development, digital health literacy, behavioral health capacity, and care coordination networks. North Carolina invested $10 million in rural EMS agencies and launched three separate programs to improve digital infrastructure. Wyoming deployed $205 million toward physician residency programs, emergency resource pooling, and statewide telespecialist platforms.

For rural hospital CFOs, RHTP funding is not a passive revenue source. It requires an active grants management function, a clear capital project pipeline, and the organizational capacity to execute funded initiatives within state-defined timelines. Finance leaders who approach RHTP as a windfall will underperform relative to those who treat it as a structured capital planning opportunity.

The grant writing and strategic positioning analysis I covered in the Rural Health Transformation Program CFO and CIO Guide published in March walks through the EHR and ERP application strategy in detail. If your organization has not yet submitted a letter of interest to your state RHTP office, that is the first action item.

However, it is worth being direct about the RHTP's limitations. CMS stipulates that no more than 15 percent of funds can be used on hospitals or direct patient care. The majority of available funding is directed toward infrastructure, transformation initiatives, and workforce programs — not the operational losses that are pushing rural hospitals toward closure today.

What Actually Separates Hospitals That Survive From Those That Close

The financial turnaround literature that exists on rural hospital recovery points to a consistent pattern: the hospitals that survive are not always the ones with the best grant writers. They are the ones whose leadership teams face operational reality early, make decisions with a long time horizon, and control the variables that are actually within their authority.

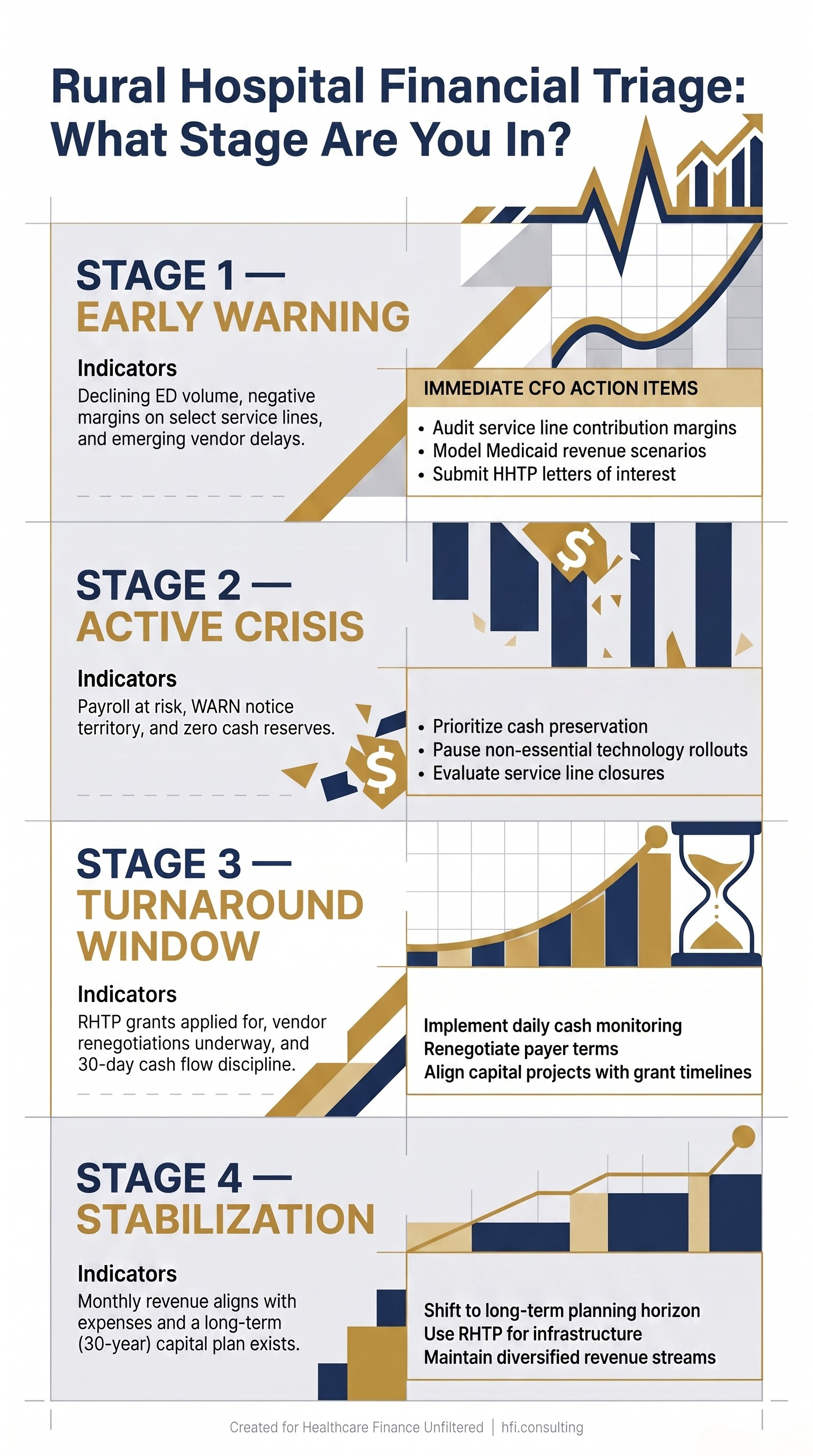

East Adams Rural Healthcare in Ritzville, Washington came within months of closure in 2025. When CFO Viola Babcock joined, the hospital had no cash and vendors who had not been paid in six to seven months. Payroll was at risk. The hospital filed a WARN notice in fall 2025, which is required by federal law when payroll continuity is in question.

What followed was a deliberate decision to manage toward a 30-to-50-year horizon rather than quarter-to-quarter survival. Leadership renegotiated vendor and payer terms, rebuilt cash flow discipline, and refused to pursue initiatives that had payback periods longer than the hospital's remaining financial runway. One year later, net revenue tracks with expenses monthly, vendors are paid biweekly, and the hospital added a new ambulance to its fleet.

CFO Babcock's framing is worth holding onto: "We are going to make long-term decisions. I think that is what separates this team and the board from all other turnarounds that I have seen, because they tend to be short term."

That framing applies directly to the service line decisions rural CFOs are making right now. The decision to eliminate obstetrics, chemotherapy, or general surgery is not a cost reduction. It is a contribution margin calculation with community access consequences. The framework for building those decisions with financial rigor is in the Hospital Service Line Closures CFO Financial Framework — a piece that addresses exactly the analytical process rural leaders need before removing a service from their portfolio.

Decision flowchart showing four stages of rural hospital financial crisis and CFO action steps for each stage in 2026.

The Point of No Return: When the Math Stops Working

Not every rural hospital can be turned around. Understanding when a hospital has crossed into unsalvageable territory is a leadership responsibility that is rarely discussed directly, but it is the most important financial judgment a rural CFO can make.

Nitesh Kumar, MD, CEO and founder of A3HCS, who has advised facility turnarounds, draws a direct line: "A hospital crosses into 'point of no return' territory when the losses are driven by forces leadership can't reverse: workforce shortages that can't be staffed around, a shrinking or aging local population that can't sustain volume, or capital needs so large that no realistic financing path exists. The tell is whether the next dollar invested still moves the needle. If it doesn't, you're no longer managing a turnaround; you're managing a wind-down."

For finance leaders managing hospitals with six months or fewer of financial runway, the prioritization framework is cash preservation first, continuity of patient care second. Everything else — technology rollouts, long-term strategic planning, systemwide culture initiatives — belongs on hold until the runway is extended.

This calculus is similar to the restructuring analysis I covered in the Healthcare Bankruptcy 2026 CFO Restructuring Playbook. The tools are different in a rural context, but the decision logic — protect cash, control what you can control, stop initiatives that don't move the needle within your runway — maps directly.

Rural hospital closures also create downstream financial consequences that CFOs at surviving facilities need to model. When Sturgis Hospital in Michigan closed in June after 101 years, it left a 13 percent decrease in emergency department volume as a leading indicator in the months prior. When a rural hospital closes, remaining hospitals in the region absorb uncompensated volume, experience workforce migration pressure, and face supply chain disruption. The emergency department census changes, the payer mix shifts, and the fixed cost structure does not.

The State-Level Funding Gap Finance Leaders Need to Watch

The June 2026 state activity report from State Health and Value Strategies documented the broad range of state responses to the rural health crisis. Beyond RHTP grant distribution, states are implementing Medicaid provider oversight changes, telehealth infrastructure programs, and Marketplace affordability efforts — all of which carry revenue implications for rural hospitals.

States that have not expanded Medicaid remain the highest-risk environments. The Medicaid revenue differential between expansion and non-expansion states directly correlates with rural hospital operating margins. In Medicaid expansion states, rural hospital Medicaid revenue shares rose an average of 33 percent in the first two years of expansion, equivalent to approximately $2 million per hospital in additional revenue, while uncompensated care costs fell 43 percent.

For rural hospital CFOs operating in non-expansion states, the financial strategy is more constrained. The RHTP grants provide capital access but do not address the structural reimbursement gap. The state-directed payment caps in H.R. 1 further narrow the tools available to state Medicaid programs to supplement hospital payments. Finance leaders in these environments need to model Medicaid revenue scenarios with the cap constraints explicitly included.

Building a Sustainable Rural Finance Strategy

The rural hospitals that are finding financial stability share three operational characteristics. First, they have disciplined cash flow management that extends beyond monthly reporting to daily monitoring during periods of financial stress. Second, they have diversified their revenue through service line rationalization that is guided by contribution margin analysis, not by a commitment to maintaining historical service offerings regardless of financial performance. Third, they are treating RHTP and other federal funding not as replacement revenue but as capital that accelerates infrastructure improvements that reduce cost per unit of service over time.

Grant writing capability matters here. The organizations capturing RHTP funding disproportionately are those with existing relationships with their state health authority, prior experience with federal grant compliance, and the internal capacity to document outcomes as required by grant terms. If your organization does not have that infrastructure, building it — or contracting for it — is a finance priority before the next RHTP funding cycle closes.

The behavioral health shortage adds a specific service line dimension. Approximately 89 percent of rural census tracts are designated as Healthcare Professional Shortage Areas for behavioral health. That designation creates a documented need that strengthens federal funding applications and supports service line investment cases. Finance leaders should be using HPSA designation actively in grant narratives, not treating it as an administrative classification.

If you are a rural hospital CFO evaluating your organization's financial position against the combined pressure of H.R. 1 Medicaid changes, RHTP opportunity windows, and operating margin challenges, HFI Consulting works with health system finance leaders on exactly these decisions. The strategic scenario analysis, grant positioning, and contribution margin frameworks that determine whether a rural hospital can sustain its mission are the core of what we do. Visit hfi.consulting to connect.

What the Next 12 Months Require

The rural health finance picture in 2026 is defined by a narrow window in which federal capital is available at historically high levels while structural reimbursement pressures are simultaneously intensifying. Finance leaders who treat these as separate problems will underperform relative to those who build an integrated strategy.

The RHTP grants require organizational readiness to capture. The Medicaid coverage losses require immediate revenue scenario modeling. The H.R. 1 state-directed payment caps require proactive conversations with your state Medicaid office about how enhanced payment programs will be administered under the new rules. The workforce pipeline required to sustain rural service lines requires investment decisions today that will not generate returns for 18 to 36 months.

"There are options to closing the doors, and unfortunately, I would imagine some places don't get that option," EARH CEO Todd Nida said. "But if they do, the fight is worth it. The communities depend on us in these small rural communities, and we're vital in this community, not just for what we provide as healthcare services, but as an employer, we're vital to the economy."

That framing is accurate. It is also not sufficient as a finance strategy. The communities that depend on rural hospitals need their finance leaders to build the analytical infrastructure, the grant management capability, and the contribution margin discipline that keeps the doors open. The money exists at the federal level to support that work. Whether your organization is positioned to access it is the question that matters most right now.

For CFOs who want a structured starting point, the Rural Hospital Financial Scenario Planning Tool is available at hfi.consulting — a framework for modeling RHTP grant scenarios, Medicaid revenue impacts, and service line contribution margins under the H.R. 1 policy environment.

P.S. If you are a rural hospital CFO or finance leader, I want to understand what your biggest constraint is right now — is it grant management capacity, Medicaid revenue modeling, service line contribution margin analysis, or something else entirely? Hit reply and tell me. The answer will shape the next piece I write on this topic.