Remote Bookkeeping for Independent Medical Practices: Why Outsourcing Beats In-House and What It Really Costs

The real math behind outsourced bookkeeping, and why some firms are quietly adding fractional CFO services.

If you run a 3 to 15 provider practice, your books are probably being handled by whoever has five spare minutes. That is not a knock on your office manager. It is just how independent medicine works when margins are tight and headcount is tighter.

The problem is that medical bookkeeping is not small business bookkeeping. A single patient visit can generate a copay, a partial insurance payment weeks later, and a contractual adjustment after that. Miss the reconciliation on any one of those, and your P&L stops reflecting reality.

That gap is exactly why remote, healthcare-specialized bookkeeping has become the default operating model for independent practices between roughly $1M and $15M in revenue. It is worth understanding why it works, what you are actually paying for, and why a growing number of these boutique bookkeeping firms are quietly turning into something closer to a part-time finance department.

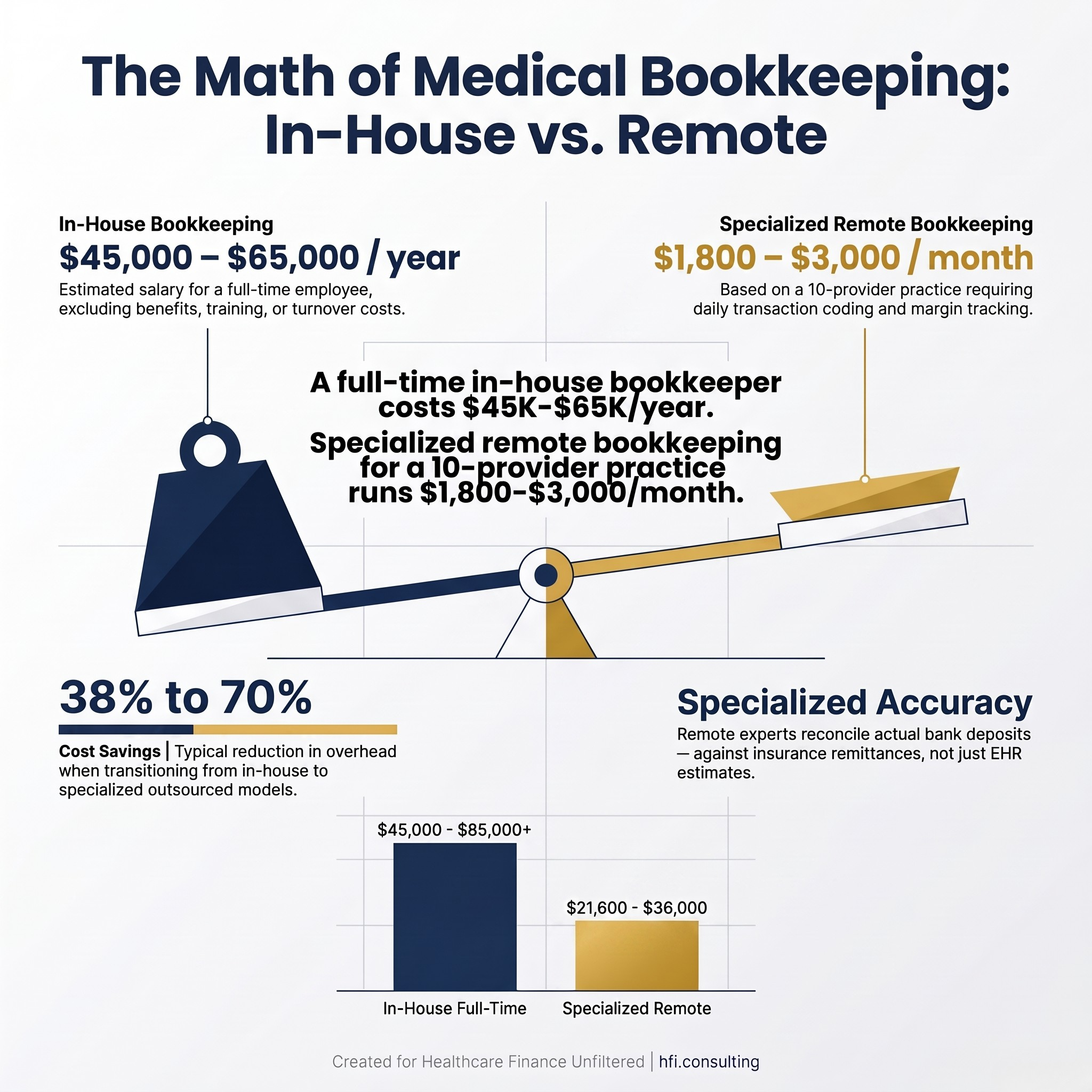

Cost comparison graphic showing in-house bookkeeper salary versus monthly outsourced bookkeeping fees for medical practices

Why In-House Bookkeeping Breaks Down at This Size

Independent practices sit in an awkward middle. They generate too many transactions for an office manager to handle as a side task, but not enough margin to justify a full-time controller.

The front desk problem. In most small practices, bookkeeping lands on the same person checking in patients, verifying insurance, and answering phones. Financial recording becomes the task that waits, and waiting is how books fall behind. Entries get batched at the end of a long week, and small mismatches quietly compound into a reconciliation headache by quarter end.

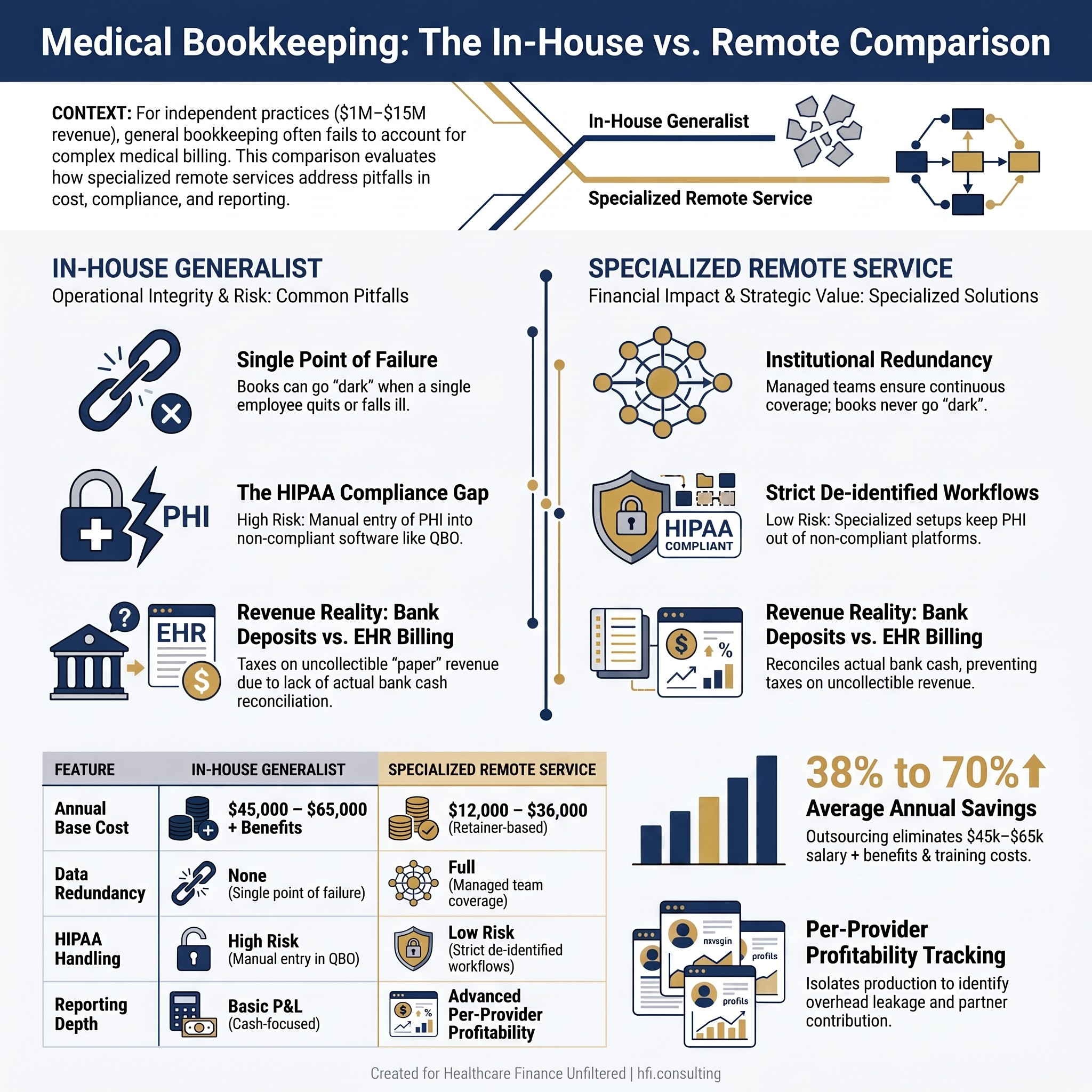

The single point of failure problem. If your office manager is your bookkeeper and that person leaves, your financial data stalls. There is no backup, no institutional memory, and no one who can pick up the reconciliation mid-stream. It is the same ownership gap that shows up when nobody is clearly accountable for a health system's Medicare cost report: the task gets treated as a side responsibility until the day it cannot be.

The billing versus accounting confusion. This is the single biggest financial blind spot in independent practices. General bookkeepers, and sometimes owners themselves, look at an EHR or billing clearinghouse and treat gross charges or estimated receivables as real revenue. It is not. Real revenue is what actually lands in the bank account after contractual write-offs and clearinghouse fees, and confusing the two means a practice can end up paying taxes on money it will never collect.

From my time in payer operations, I watched this exact confusion play out from the other side of the claim. Practices that treated billing software as their accounting system consistently misjudged their own cash position, sometimes by tens of thousands of dollars a quarter, simply because nobody was translating claims data into true collected revenue.

Comparison table of in-house versus outsourced medical practice bookkeeping across cost, backup coverage, and reporting depth

What a Specialized Remote Bookkeeper Actually Does Differently

A generalist bookkeeper and a healthcare-specialized remote bookkeeper are not doing the same job, even if the invoice looks similar.

Disentangling billing from accounting. A specialized bookkeeper reconciles actual bank deposits against electronic remittance advices, not against what the EHR says was billed. That keeps the P&L tied to true cash flow instead of paper revenue.

Per-provider profitability. In a multi-provider practice, compensation is often tied to RVUs or collections minus a share of overhead. A properly built chart of accounts isolates each provider's production so partners can see exactly who is covering their own overhead and where the leakage is happening. This is the same discipline behind contribution margin integrity work in larger health systems, just scaled down to a physician group instead of a service line.

Institutional redundancy. A managed bookkeeping arrangement means a team steps in when one person is out, sick, or gone. Your books never go dark because one employee quit.

HIPAA-aware workflow discipline. This is the part most practices underestimate, and it deserves its own section, because it is where the real cost decisions get made.

The QuickBooks Online HIPAA Question, Answered Directly

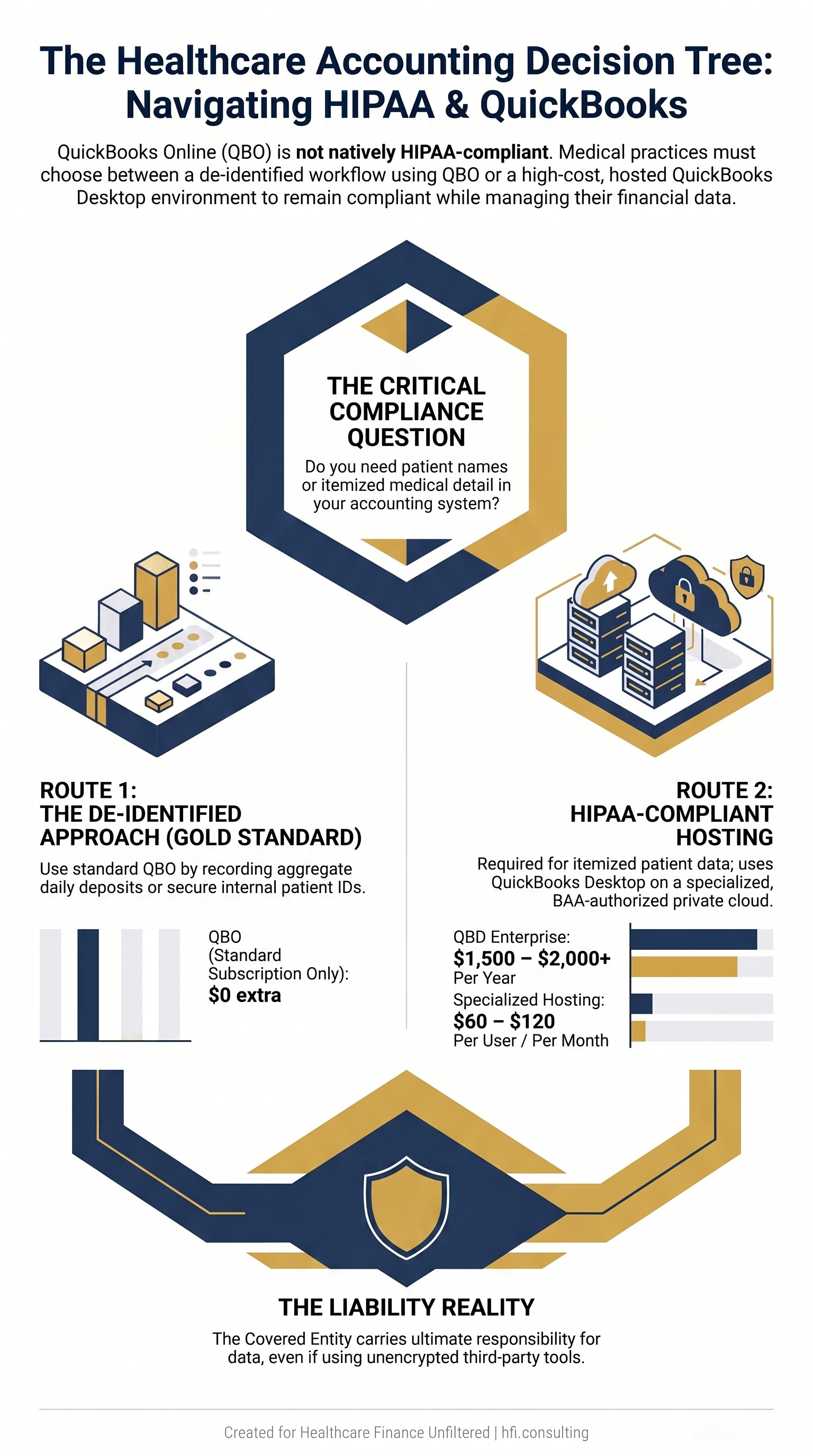

The short answer is no. QuickBooks Online does not offer HIPAA-compliant hosting, and Intuit will not sign a Business Associate Agreement. Intuit is explicit that QBO is not designed to store protected health information, and it advises against entering individually identifiable health details into the platform.

That leaves independent practices with two distinct paths, and the cost structure depends entirely on which one you choose.

Route 1: The de-identified approach. Most independent practices stay on standard QuickBooks Online and simply change how entries are recorded to stay outside HIPAA scope entirely. Instead of invoicing "John Doe for an orthopedic consultation," the bookkeeper records a generalized category, a secure internal patient ID, or an aggregate daily deposit summary pulled from a HIPAA-compliant EHR or merchant processor. There is no additional compliance cost. You pay your standard QBO subscription and your bookkeeper's standard fee.

Route 2: Dedicated HIPAA-compliant hosting. If a practice insists on running full QuickBooks functionality with actual patient names or itemized medical billing attached to transactions, QBO is off the table. That requires QuickBooks Desktop deployed inside a specialized, authorized private cloud, hosted by a company willing to sign a BAA and enforce the required technical and physical safeguards. The practice bears this cost directly: a QuickBooks Desktop Enterprise subscription running well over $1,500 to $2,000 a year, plus a recurring hosting fee typically in the $60 to $120 per user, per month range. The bookkeeper simply gets a login to that secure, practice-owned environment.

The gold standard for keeping overhead low is Route 1: standard QuickBooks Online, a strict rule against entering patient names, and every identifiable detail locked safely behind your BAA-protected EHR instead. If a remote bookkeeper brings their own generic, unencrypted tool to manage identifiable books, that is a liability blind spot, because the Covered Entity, meaning the practice, carries the ultimate responsibility for that data.

Decision flowchart showing whether a medical practice needs standard QuickBooks Online or HIPAA-compliant hosted QuickBooks Desktop

What This Actually Costs

Specialized healthcare bookkeepers for practices this size rarely bill hourly. They operate on a fixed monthly retainer that scales with provider count and complexity.

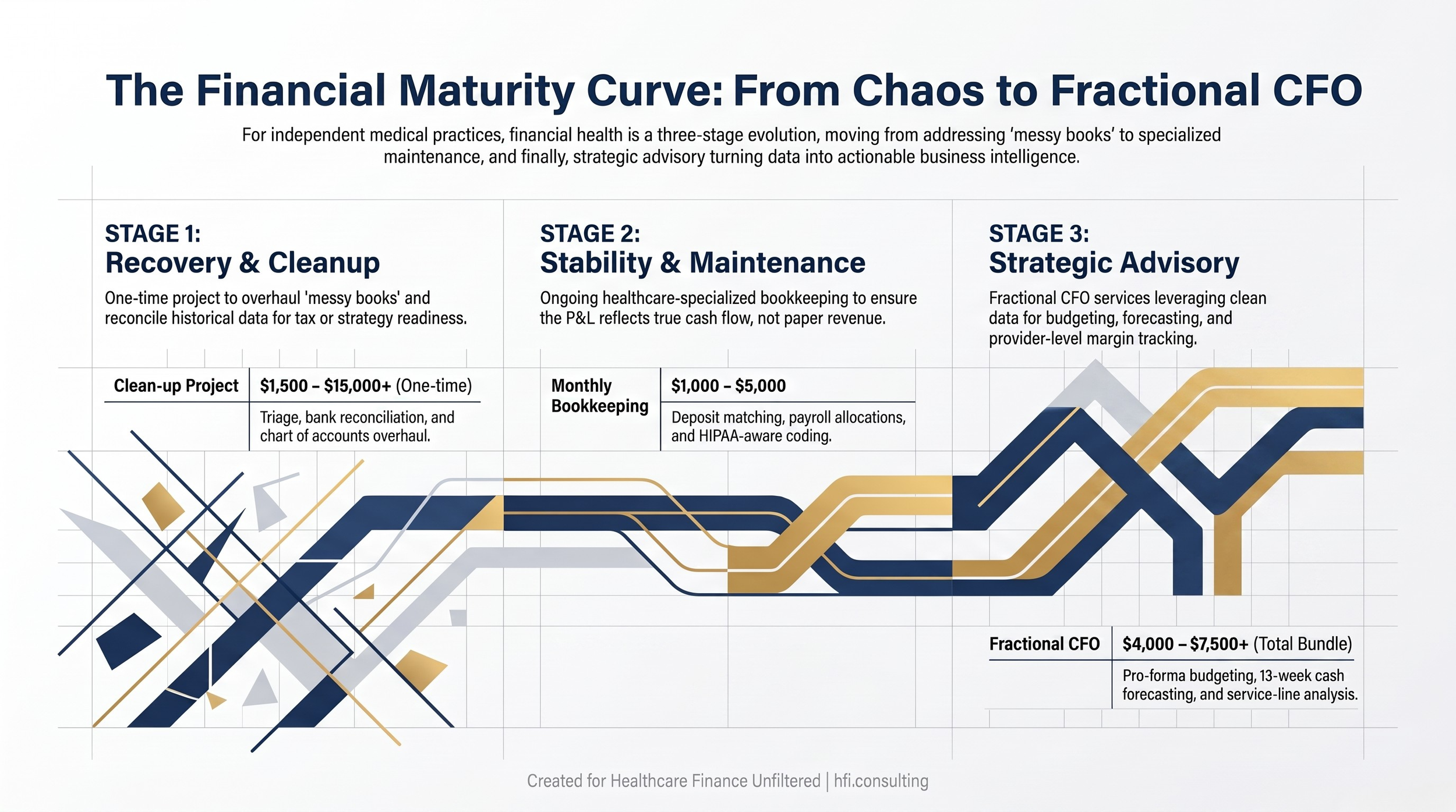

A 3 to 5 provider practice generating $1M to $3M in revenue typically runs $1,000 to $1,800 a month for daily transaction coding, deposit-to-clearinghouse matching, and baseline monthly financials. A 6 to 10 provider practice in the $3M to $7M range moves into $1,800 to $3,000 a month, adding accounts payable, payroll journal allocations, and provider-level margin tracking. An 11 to 15 provider practice with ancillary lines like physical therapy or imaging lands at $3,000 to $5,000 or more, covering multi-entity tracking and layered compensation modeling.

Compare that to a full-time in-house bookkeeper, which runs $45,000 to $65,000 a year in salary alone before benefits, training, or turnover costs, and the outsourced math becomes hard to argue with. Reported savings versus in-house typically fall in the 38 to 70 percent range depending on practice size.

Clean-up work is priced separately, as a flat one-time project rather than a retainer. Light triage for a practice one to six months behind runs $1,500 to $3,500. A full-year overhaul, the kind that surfaces right before tax season when nobody reconciled the bank account correctly all year, runs $3,500 to $7,500. Severe, multi-year chaos can run $7,500 to $15,000 or more.

Why Boutique Bookkeeping Firms Are Quietly Becoming Fractional CFOs

Here is the pattern worth watching. Once a specialized bookkeeping firm has clean, reconciled books and a properly built chart of accounts, the natural next question from the practice owner is almost always the same: now that I can see my numbers, what do I do with them?

That question is exactly where these firms start layering on advisory work, usually branded quietly as fractional CFO or strategic advisory services rather than a hard product launch. For a mid-sized practice, this typically adds $1,500 to $4,000 or more per month on top of bookkeeping, or gets bundled into a comprehensive package running $4,000 to $7,500 a month total.

What you actually get for that premium is pro-forma budgeting benchmarked against actual monthly performance, granular net revenue per FTE provider tracking mapped directly against compensation structure, service line break-even analysis for decisions like adding a new location or an in-house lab, and rolling 13-week or 12-month cash flow forecasting.

This is not a bookkeeping firm overreaching. It is the logical progression once the underlying data is trustworthy. You cannot forecast cash you cannot see, and you cannot benchmark provider productivity against a chart of accounts that was never built to isolate it. The bookkeeping is the foundation. The advisory layer is what the foundation makes possible.

Diagram showing the progression from bookkeeping cleanup to reconciled books to fractional CFO advisory services with monthly cost ranges

If your practice is at the point where you can reconcile the books but still cannot answer a basic question like which provider or service line is actually driving your margin, that is usually the signal that the conversation needs to move past bookkeeping. That is a conversation I have with independent practices fairly often, and it is one of the areas I work in through HFI Consulting when practices want that next layer without hiring a full-time CFO.

What to Look For Before You Sign

Not every bookkeeper is built for healthcare, and the wrong fit costs more than a bad invoice.

Screen for genuine healthcare fluency: comfort reconciling partial and adjusted insurance payments, not just categorizing expenses. Confirm HIPAA-aware process discipline specifically, meaning a documented answer for how they keep PHI out of QBO or how they operate inside a BAA-covered environment if you need full patient-level detail. Ask about backup coverage. A single freelancer with no team behind them is the same single point of failure you were trying to escape by outsourcing in the first place. And confirm the accounting platform actually talks to your EHR or billing system, because manual re-entry between two disconnected systems is where errors and staff burnout both live.

This is the same due diligence discipline behind avoiding the platform trap when consolidating vendors: the cheapest or most convenient option is not automatically the safest one for your revenue and your compliance exposure.

Making the Decision

Match the model to where your practice actually sits. A solo or small cash-pay practice with a tight budget can often start with a lighter-weight platform before graduating to specialized support. A 3 to 15 provider group generating real insurance volume is squarely in the zone where a specialized remote bookkeeper, kept strictly outside HIPAA scope through the de-identified approach, delivers the cleanest return.

Ready to see where your practice actually stands? Reply and tell me which side of this decision you're on: still doing books in-house, currently outsourced, or somewhere in between.

The practices that get the most value out of this shift are the ones that treat clean books as the starting point for real financial strategy, not the finish line. Whether that next step is building your own reporting cadence or bringing in fractional CFO support, the goal is the same: know your numbers well enough to make decisions with them, not just file them.

If you want a second set of eyes on your current bookkeeping setup or the fractional CFO question, that is work I do through HFI Consulting, and I am always glad to talk through where a given practice actually stands.

P.S. If you are a practice owner reading this: what's actually stopping you from outsourcing this, cost, trust, or just not knowing where to start? Hit reply, I read every response.