Health System Portfolio Rationalization: The CFO's Framework for Growing Up Instead of Out

Large systems are shedding hospitals and investing in specialty depth. What the scale-to-market-potential shift means for your capital strategy.

Infographic showing 2026 health system portfolio rationalization data including CommonSpirit, CHS, and Tenet strategic portfolio shifts.

The nation's largest nonprofit health systems are divesting hospitals at the same moment for-profit systems are reshaping their portfolios. Common Spirit Health transferred Trinity Health System to UPMC, sold a critical access hospital in North Dakota, and is in the process of selling three more. Community Health Systems is divesting nine hospitals across four states for more than $1.2 billion. This is not a distress story. It is a strategy story.

The question every health system CFO needs to answer right now is not "where can we grow?" It is "where should we invest?" Those are different questions, and they carry very different capital implications.

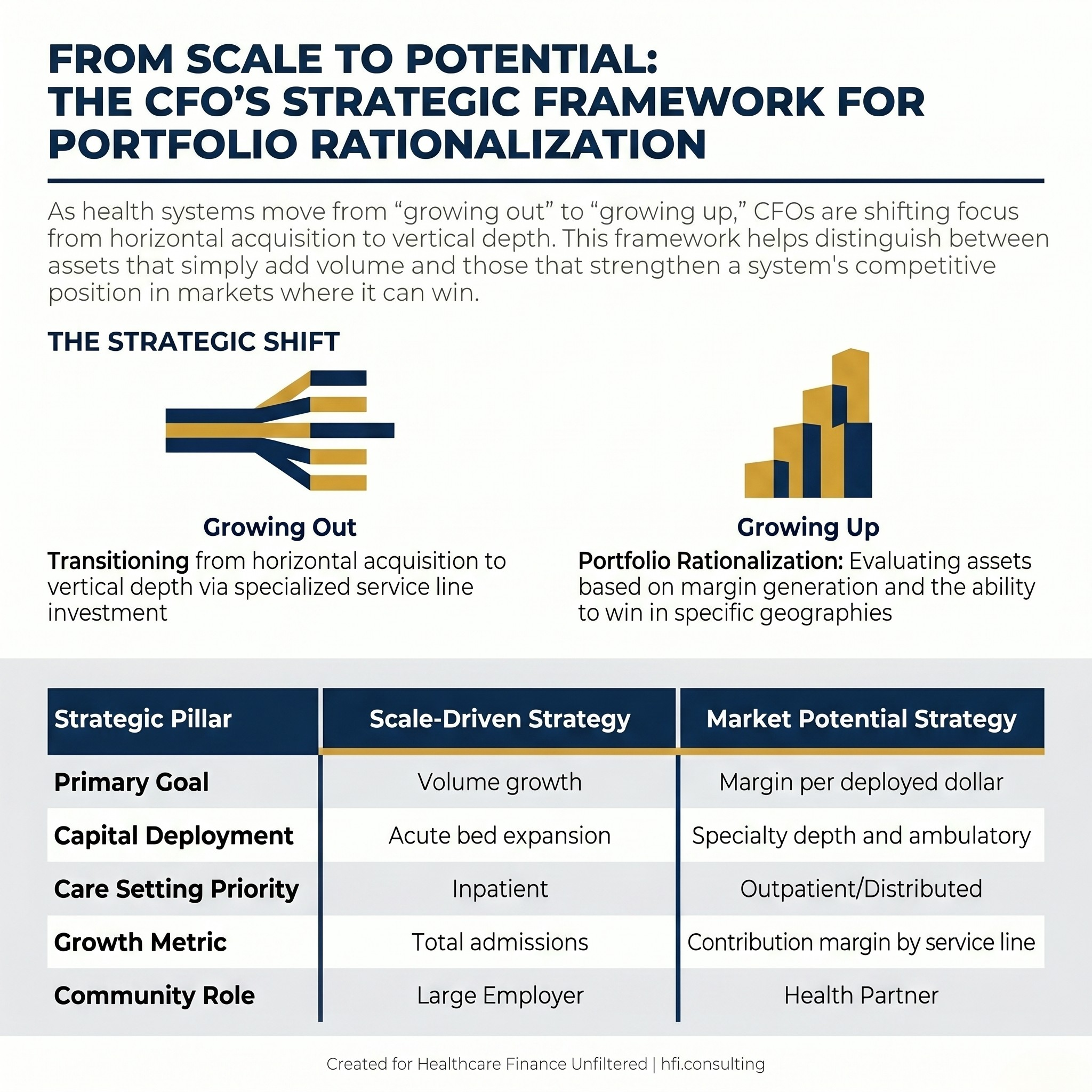

The Mechanics of Portfolio Rationalization

The term portfolio rationalization sounds like a board presentation abstraction. The mechanics are straightforward. A system evaluates each hospital or facility against two criteria: does it generate margin, and does it strengthen the system's competitive position in markets where the system can actually win?

When neither answer is yes, the asset becomes a candidate for divestiture. That logic is driving the current wave of deals whether the seller is nonprofit or for-profit.

CommonSpirit's senior vice president of treasury and strategic investing described the process plainly in a recent Becker's interview. The conversation centers on whether a market is better served by CommonSpirit or by another organization. Integris Health CEO Timothy Pehrson calls it "smart growth," focusing on health value rather than volume and avoiding acquisitions likely to dilute margin or stretch operations too thin.

The CFO's version of that question is more specific. It is about return on deployed capital relative to market position, and whether the strategic rationale that justified the original acquisition still holds in the current operating environment.

The Jacksonville Problem, Scaled to a National Lesson

Jacksonville is a useful case study for what happens when multiple well-resourced systems compete for the same geographic market. HCA, UF Health, Baptist Health, Ascension, and Mayo Clinic all have significant presence in the region. The market is not underserved. In acute care, it is oversaturated.

What the Jacksonville market has produced in response is a shift in the infrastructure layer below hospital campuses. Urgent care centers are multiplying. Freestanding emergency departments are appearing in suburban and rural corridors. Medical office parks are expanding into areas that previously had minimal outpatient infrastructure.

Those are not random market decisions. They reflect what happens when a health system or a private equity-backed ambulatory operator concludes that acute bed capacity is not the constraint, and that patient access, care coordination, and convenience are where differentiation actually lives.

Tenet Healthcare deployed $125 million into seven ambulatory surgery center acquisitions in Q1 2026 alone. That is the national version of the same logic playing out in Jacksonville every week. The capital is not going to more hospital beds. It is going to facilities that serve patients in different care settings at different cost structures.

The Financial Architecture of "Growing Up"

The phrase "growing up instead of out" has a specific financial meaning. Horizontal growth through acquisition adds assets that may or may not generate margin. Vertical depth through service line investment, technology integration, and care model redesign improves contribution margin on existing volume.

The financial case for depth over breadth starts with cost structure. A 25-bed critical access hospital in a rural market with a thin payer mix and aging physical plant is a fundamentally different capital commitment than investing in a Center of Excellence in orthopedics, cardiovascular care, or oncology at an existing anchor facility. One requires ongoing subsidy. The other can drive margin improvement across a service line.

Working across seven hospitals at Ascension, the facilities with the strongest contribution margins were rarely the largest by bed count. They were the ones with defined clinical niches, strong physician alignment, and payer contracts that reflected their specialized position in the market. The CFO's job is to build the analytical framework that makes those distinctions visible to the board before a divestiture conversation becomes reactive rather than strategic.

Comparison table contrasting scale-driven and market-potential-driven health system strategy for CFO capital planning.

What the Financial Analysis Actually Looks Like

Portfolio rationalization at the CFO level requires three parallel assessments running simultaneously: margin by facility, market position by geography, and capital commitment by strategic priority.

The margin analysis starts with contribution margin by service line at each facility, not just operating margin at the entity level. A facility can generate a system-level loss while contributing positively in specific service lines. The decision about what to do with that facility depends on whether those service lines can be relocated or replicated elsewhere in the portfolio.

The market position analysis asks whether the system has the scale and clinical depth to be the dominant provider in that geography. Community Health Systems CEO Kevin Hammons articulated this directly in Becker's: divestiture of non-core hospitals allowed the system to focus on markets where it has the full continuum of care and can leverage its scale. The hospitals that left the portfolio were not necessarily losing money. They were not in markets where the system could win.

The capital commitment analysis is where CFOs have the most direct influence. Every facility that remains in the portfolio competes for capital in the annual planning cycle. A facility that absorbs capital without improving its margin position or market position is pulling resources from facilities that could deploy the same capital more productively. That opportunity cost is often invisible in system-level financial reporting and visible only when you model scenarios explicitly.

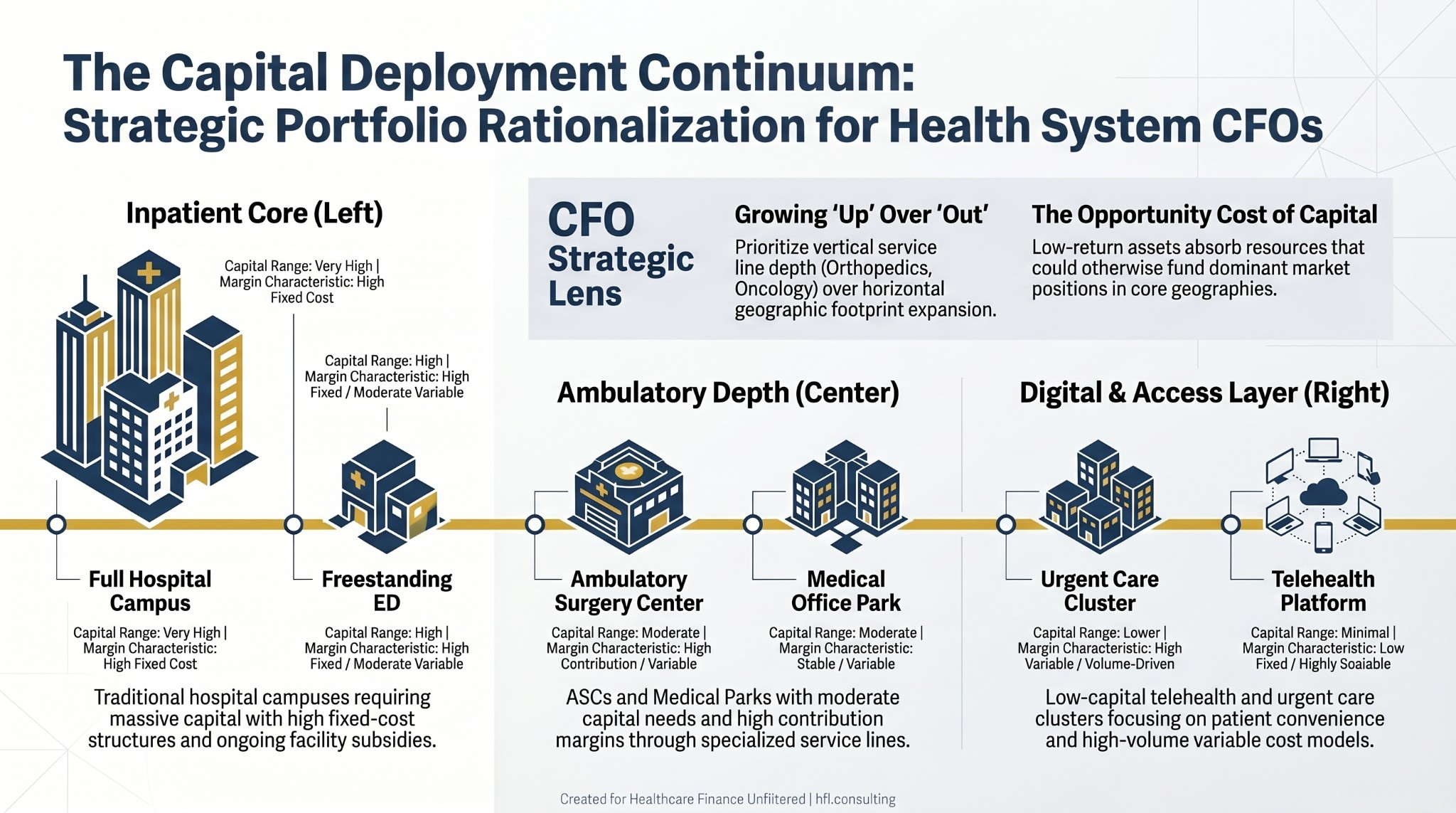

The Ambulatory Shift as a Capital Strategy

The move toward ambulatory care is not new, but the pace has accelerated in ways that have direct implications for how CFOs should be modeling capital deployment. Tenet's ASC strategy and HCA's simultaneous acquisition and divestiture activity in 2025 reflect a sector-wide reassessment of where inpatient and outpatient capacity are needed and in what ratio.

For CFOs, ambulatory expansion is a capital allocation question with a community access dimension. Freestanding emergency departments and urgent care centers reduce cost-per-encounter for conditions that do not require inpatient admission. They also extend the system's geographic reach without the full capital commitment of a new hospital campus.

The financial model for ambulatory care differs from the inpatient model in ways that matter for planning. Contribution margin per visit is lower. Volume requirements are higher. Staffing ratios are more favorable. The payer mix question is critical, particularly as high-deductible plans continue to shape when and whether patients seek care and what they are willing to pay out of pocket.

Capital deployment spectrum for health system CFOs showing investment scale and margin profile from hospital campuses to telehealth infrastructure.

If your system is working through a service line prioritization or portfolio assessment and you want a framework built around your specific market position and capital constraints, hfi.consulting is where I work through these questions with finance leaders.

For a structured starting point on service line financial analysis, seeService Line Financial Assessment: The CFO's Framework for Capital Decisions That Actually Hold Up.

When a Market Is Full

One of the underappreciated realities in health system strategy is that some markets are simply full. Not underserved. Not misserved. Full, in the sense that the available patient volume does not support additional acute care capacity without redistributing existing volume from competitors.

Adding beds in a fully saturated acute care market does not generate new revenue. It generates competition for existing volume at higher fixed cost. The systems that recognize this early can make proactive portfolio decisions with a full range of strategic options. The systems that recognize it late are making reactive divestiture decisions under financial pressure, which is a meaningfully worse negotiating position.

Providence's consideration of selling its insurance arm is an example of a different dimension of portfolio rationalization. The question is not just which hospitals fit the strategic vision. It extends to which business lines the organization can execute competitively given its core capabilities and capital position. CFOs who frame the portfolio question broadly across payer relationships, joint ventures, ambulatory assets, and physician enterprise alongside inpatient facilities are the ones who can surface strategic options before those options narrow.

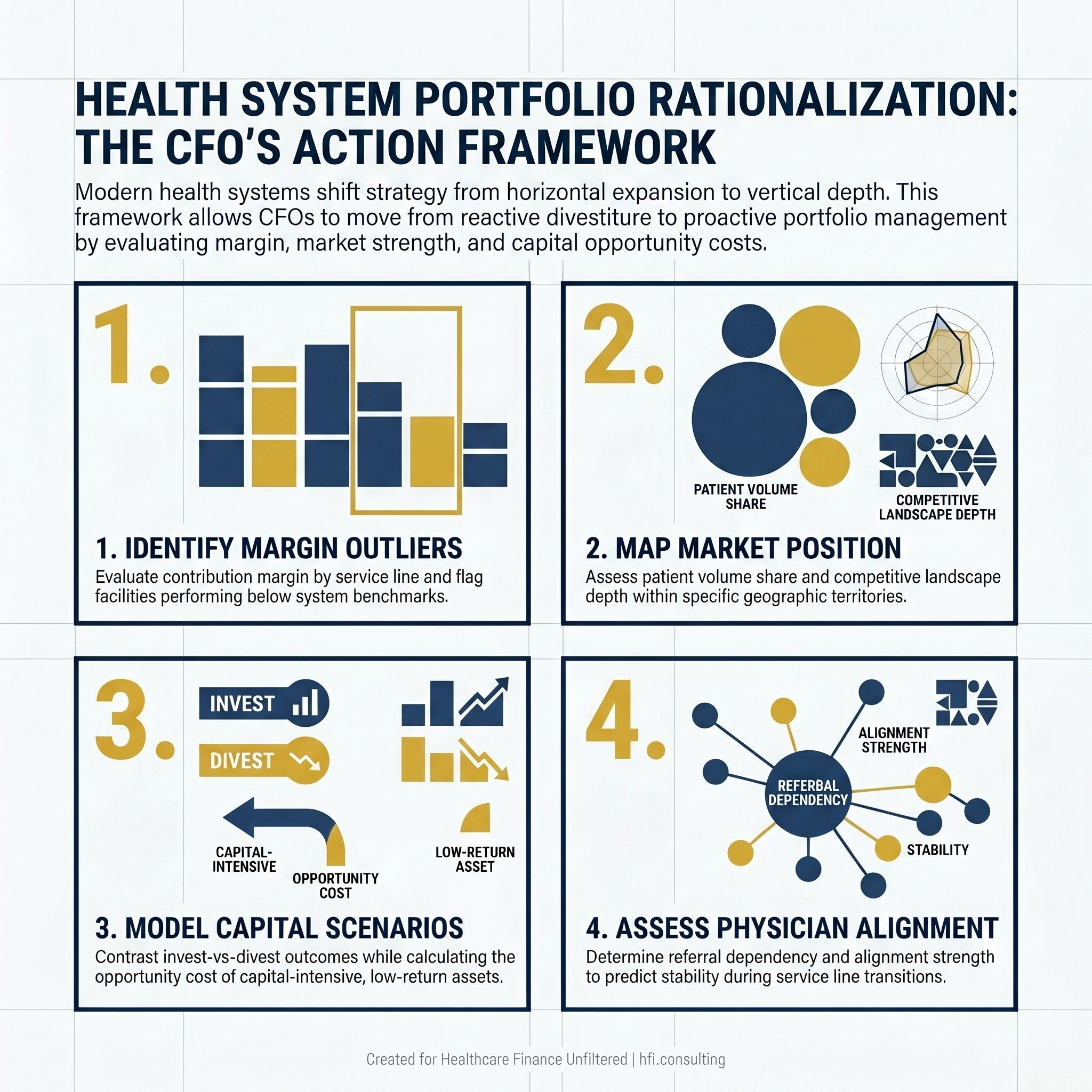

The CFO's Four-Part Action Framework

The national divestiture wave makes portfolio review a timely exercise regardless of whether a specific transaction is being contemplated. Here is a practical starting point.

Identify margin outliers. Which facilities are generating contribution margin below system average? Which service lines are below benchmark at those facilities? Are the root causes structural (market position, payer mix, physical plant) or operational (staffing model, physician alignment, coding accuracy)?

Implant-driven service lines deserve particular scrutiny here. Orthopedic and cardiovascular programs routinely carry contribution margin variance of 400 basis points or more across facilities in the same system, driven by physician preference item costs, payer contract rates, and charge capture gaps that never surface in a standard cost report review. If your margin analysis has not included implant costs and billing accuracy by procedure type, you are likely missing a recoverable gap. This is one of the core analyses I run with finance teams athfi.consulting, working through contribution margin and implant cost reviews for hospitals and ASCs that want to understand where the exposure is before a board conversation forces the issue.

Map market position. For each geographic market, assess the system's share of relevant patient volume and competitive position relative to key service lines. A facility with a weak market position in a crowded geography is a candidate for reassessment regardless of individual financial performance.

Model capital scenarios. For facilities under review, build two scenarios side by side: continued investment with projected return, and divestiture with redeployment of capital to core markets. The comparison should include not just the direct financial return but the opportunity cost of capital currently absorbed by low-return assets.

Assess physician alignment. In markets where physician groups are the primary referral source, the strength of alignment determines whether a service line repositioning or divestiture will affect volume at remaining facilities. This variable often determines timing more than financial analysis does.

Four-part CFO action framework for health system portfolio rationalization: margin analysis, market mapping, capital scenario modeling, and physician alignment assessment.

The Growth Definition That Actually Works

The language health system leaders are using in 2026 reflects a genuine shift in how growth is being defined. Houston Methodist President and CEO Marc Boom articulated it directly in Becker's: growth means more than expanding a footprint. It is growing in ways that best serve patients, and checking boxes to have a presence in an area no longer counts.

For CFOs, the practical implication is that growth metrics need to evolve alongside the strategy. Volume growth in isolation is not a useful performance indicator when the system is intentionally exiting low-margin markets. Revenue per facility is a better metric when the portfolio is being rationalized. Contribution margin by service line is more useful than system-wide operating margin when specific clinical investments are being evaluated.

For a related framework on how healthcare M&A decisions play out post-close, see Healthcare M&A in 2026: Your Deal Just Closed. Now Comes the Hard Part. The financial discipline required to execute a divestiture is the same discipline required to capture value from an acquisition.

Growing up is harder than growing out. It requires more analytical rigor, more difficult conversations with boards and community stakeholders, and more organizational discipline about what the system is and is not trying to be. But it is the decision framework that produces durable financial performance in markets that are no longer rewarding size for its own sake.

The systems that will be in the strongest financial position in five years are making clear-eyed decisions now about where they can actually compete, investing in depth in those markets, and letting go of assets that absorb capital without strengthening their position.

If you are working through a portfolio assessment, service line rationalization, or capital redeployment analysis, visit hfi.consulting to see how I approach these questions with finance teams.

For a deeper look at how capital decisions play out when market position is the primary variable, theFlorida Healthcare Expansion 2026: What CFOs Must Know About Capital ROI Before Breaking Ground piece covers the ROI framework in a market where expansion decisions are happening in real time.

P.S. Which is the harder conversation at your organization: deciding which markets to exit, or getting board alignment on what "strategic focus" actually means when a specific facility is on the table? Hit reply and tell me.