Government and Academic Hospital Transfers: The CFO Due Diligence Framework When Public Assets Enter the Deal

When a municipal hospital transfer skips statutory requirements, the litigation risk lands on your balance sheet before the deal ever closes.

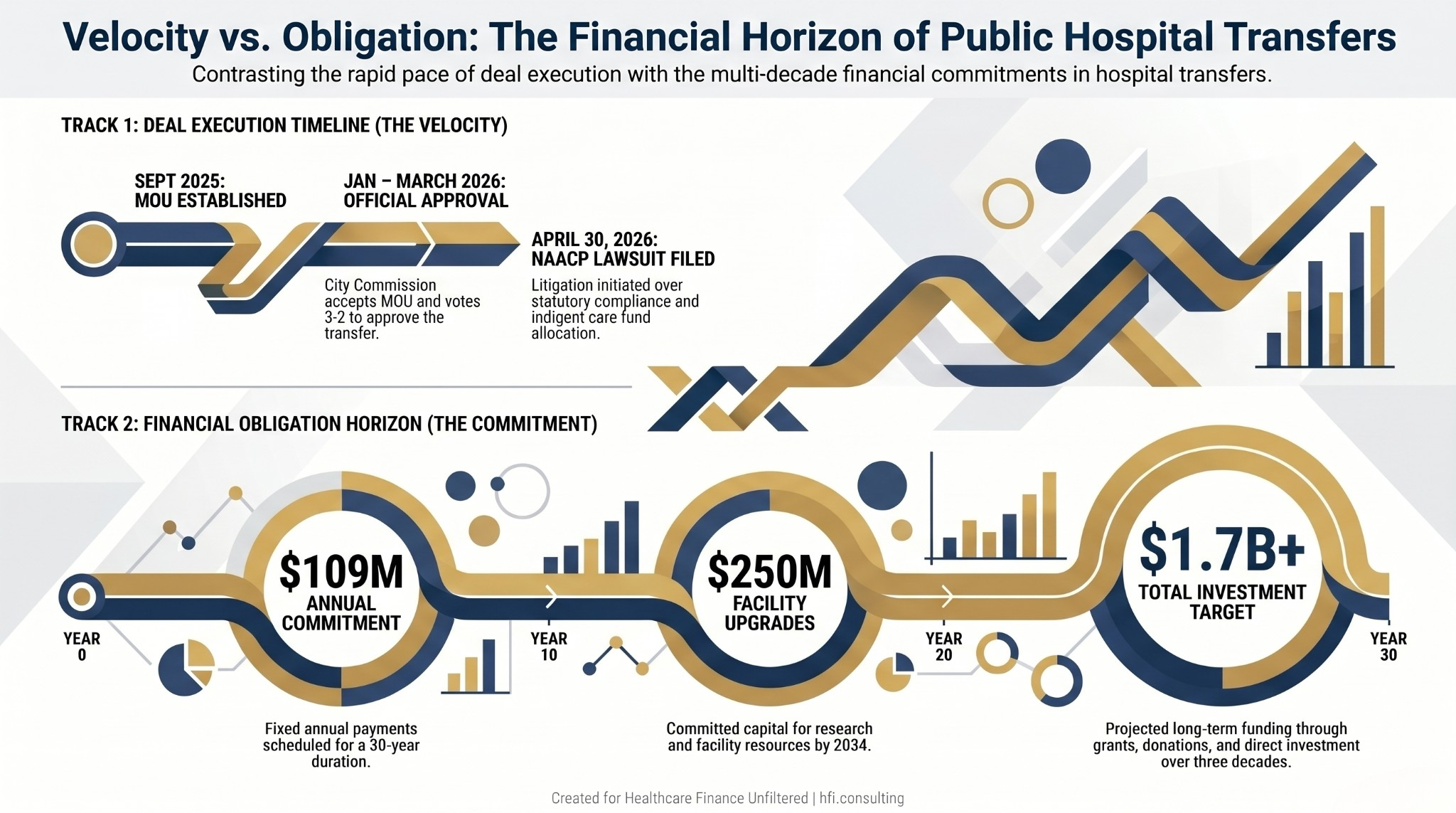

A 3-2 city commission vote in Tallahassee was supposed to be the final political hurdle before a 772-bed hospital transferred from city ownership to Florida State University. Six weeks later, it became a lawsuit.

The Tallahassee Branch of the NAACP filed suit in late April alleging the city violated Florida statutory requirements governing the sale or transfer of public hospital property. The complaint specifically alleges the city failed to properly allocate sale proceeds for indigent care and economic development purposes, did not obtain Tallahassee Memorial HealthCare's consent, and did not offer the assets to TMH before approving the deal.

This isn't just a Tallahassee story. It is a framework problem that applies to every CFO evaluating a hospital transfer involving a government entity, academic partner, or publicly owned asset.

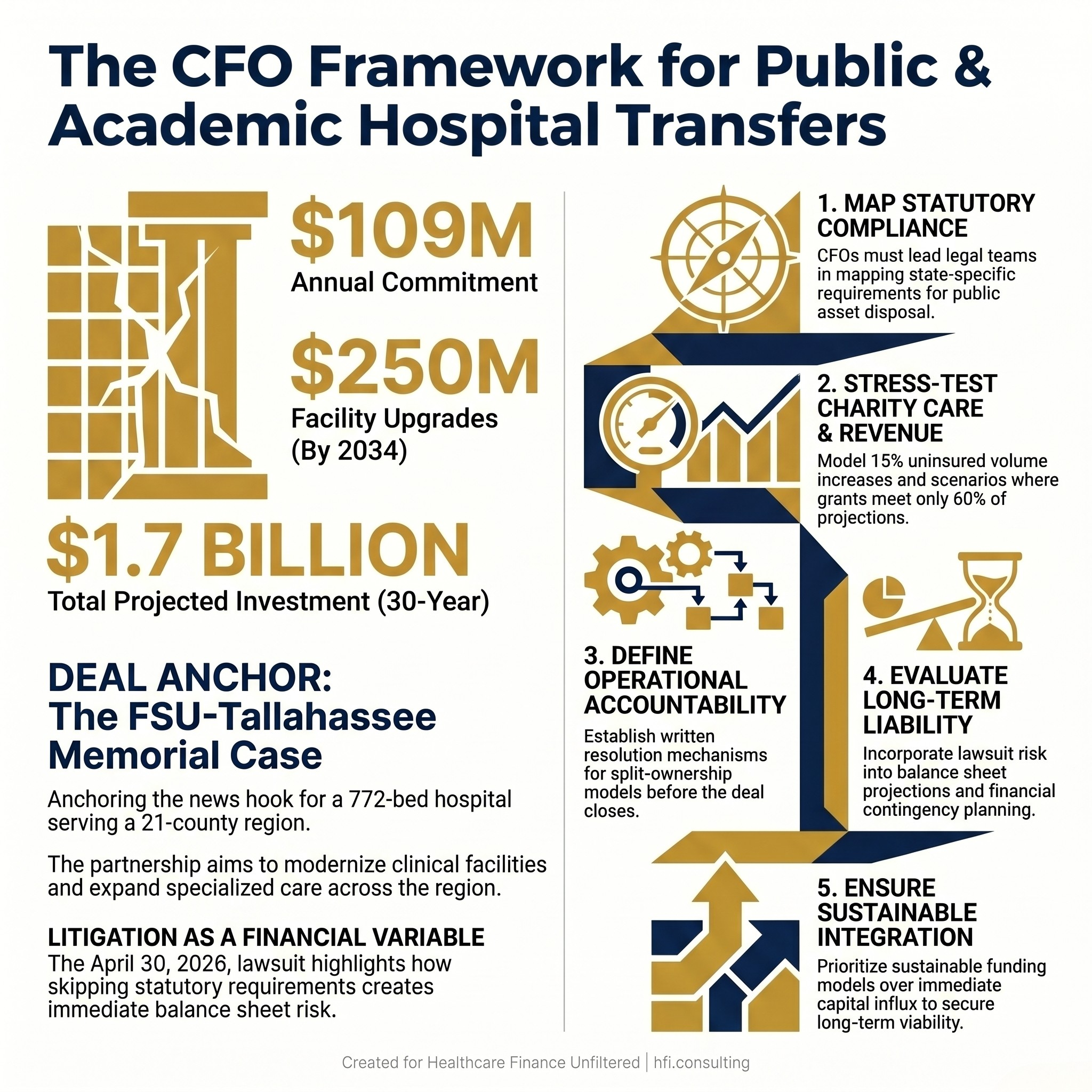

Infographic displaying key financial terms of the FSU-Tallahassee Memorial HealthCare hospital transfer deal alongside the NAACP lawsuit filing date.

Why Government and Academic Deals Break Down Differently

Most hospital M&A analysis focuses on the commercial transaction: valuation, payer mix, operational synergies, debt assumptions. When a municipal government or state university is involved, the financial analysis has to extend into an entirely different layer of legal obligation, community accountability, and long-term contractual commitment.

The FSU deal was structured as a property transfer with TMH retaining long-term operating responsibility under a lease. FSU would own the assets; TMH would run the hospital. That split-ownership model has real financial advantages. It can separate capital obligations from operational risk and attract academic investment that would not otherwise reach a community hospital. But it also creates legal complexity that traditional commercial deals do not carry.

Municipal hospital assets in Florida are subject to specific statutory requirements governing how they can be disposed of. When those requirements are not followed, even if the underlying deal is financially sound, the transaction becomes legally vulnerable. The NAACP lawsuit is not primarily arguing that FSU is a bad partner for Tallahassee. It is arguing that the process violated the law.

For CFOs evaluating similar deals, the lesson is that process compliance is itself a financial variable. A deal that falls apart in litigation costs more than a deal that takes an extra six months to close properly.

What the FSU Framework Tells Us About Academic Partnerships

The proposed investment structure is worth examining on its own terms, because academic medical center partnerships are becoming more common as health systems seek capital and mission alignment simultaneously.

FSU committed to $109 million in annual payments over 30 years as compensation for the city-owned assets, $250 million by the end of 2034 in facility upgrades and research resources, and a broader investment plan targeting more than $1.7 billion over three decades through grants, donations, and other funding sources.

That is a significant long-term commitment. It is also the kind of commitment that requires CFO-level modeling well beyond the initial deal terms. What does $109 million per year look like against projected inflation in facility maintenance costs over three decades? What is the risk that grant and donation revenue does not materialize at projected levels? What happens to the academic center's financial commitments if the university faces its own budget pressure mid-cycle?

These are not hypothetical questions for the FSU situation. They are the questions that belong in a financial model before any board signs off on this structure.

The Indigent Care Variable Is Not Optional

The lawsuit specifically alleges the city failed to properly allocate sale proceeds for indigent care purposes. This is the piece that most CFO analyses underweight in academic and government deals.

Tallahassee Memorial HealthCare operates as the primary safety-net provider for a 21-county region. Even if the region's indigent population is modest relative to major urban markets, the legal obligation to continue that care does not disappear when asset ownership changes. It becomes more complicated.

When a public hospital transfers to an academic or quasi-public entity, state and federal law typically requires explicit commitments about charity care continuation. The Disproportionate Share Hospital payments the institution currently receives are tied to those obligations. If the ownership structure changes in ways that affect DSH eligibility, the revenue impact is immediate and material.

The memorandum of understanding in the FSU deal does address charity care continuity, requiring that protections remain at least as generous as current arrangements. But the lawsuit argues the allocation of sale proceeds for indigent care purposes was not handled correctly. That is a separate legal issue from the ongoing care commitment itself, and it carries its own financial consequence.

For CFOs, charity care obligations in these transactions have two distinct financial dimensions. The first is the ongoing cost of delivering that care after closing. The second is the proper handling of any proceeds from the asset transfer itself. Both require explicit modeling. Neither belongs in a paragraph in a memorandum of understanding.

From my work at UF Health Jacksonville at a Level 1 Trauma center and Level 3 NICU, I know firsthand that indigent care obligations are not uniform across institutions. The populations you serve, the payer mix implications, and the community benefit documentation requirements all vary by market. A deal structure that works in one geography may create material financial exposure in another.

For a deeper look at service line financial assessment frameworks that intersect with these obligations, the analysis applies directly to how academic partners evaluate which programs to grow.

Dual-track timeline showing the FSU-Tallahassee Memorial deal approval milestones alongside the 30-year financial commitment schedule.

The CFO's Five-Step Due Diligence Framework for Government and Academic Hospital Transfers

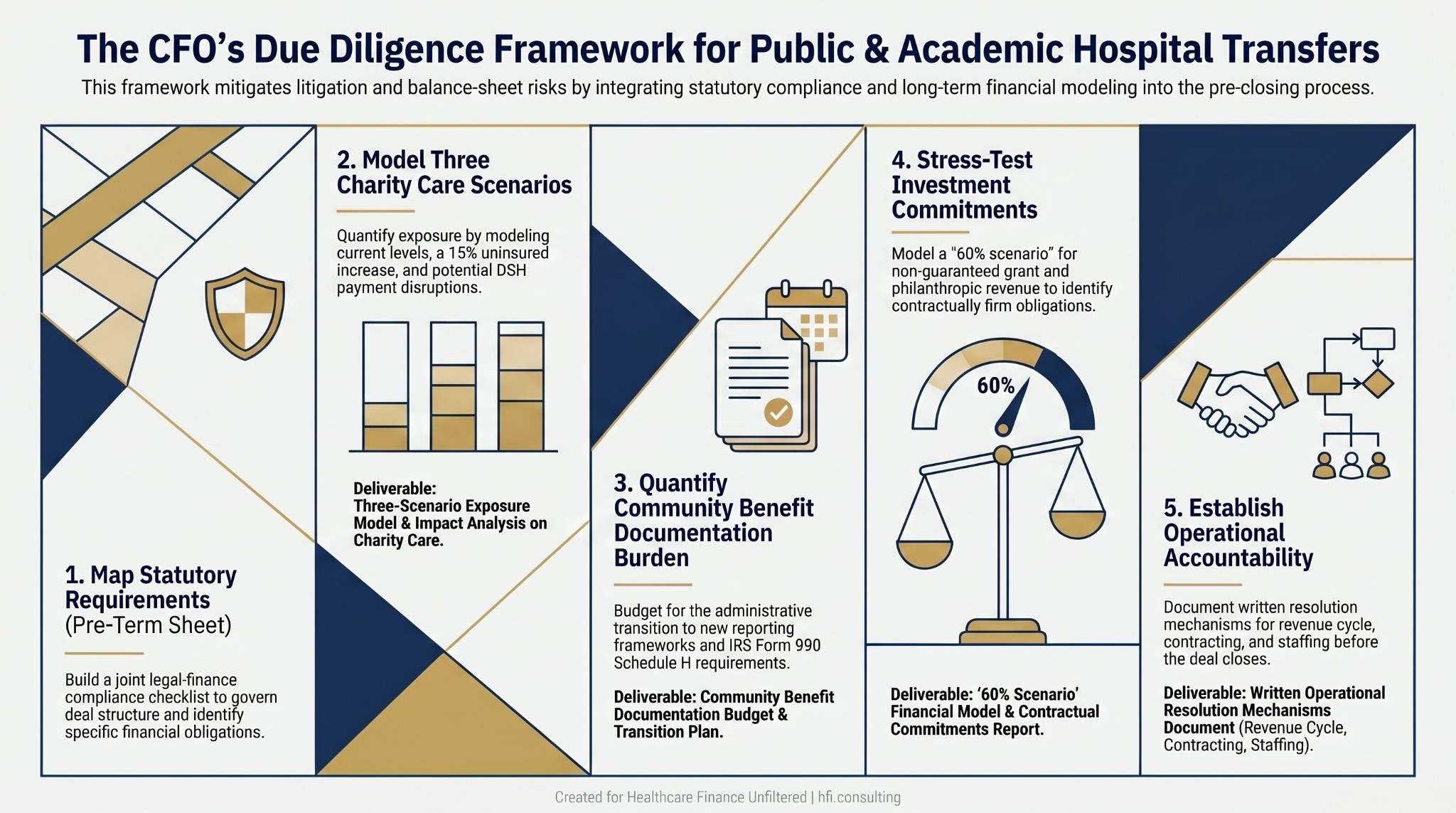

Five-step CFO due diligence process flow for government and academic hospital transfer transactions, covering statutory compliance through operational accountability.

Step 1: Map the Statutory Requirements Before the Term Sheet

Government hospital transactions are governed by state law, not just general M&A practice. Florida's statutory requirements for the disposition of municipal hospital assets are specific about process, consent, and the allocation of proceeds. Before any term sheet is signed, legal and finance teams need to jointly map the applicable statutory requirements and build a compliance checklist that governs deal structure, not just closing conditions.

This step is often delegated entirely to outside counsel. That is a mistake. The CFO needs to understand the specific financial obligations that attach to statutory compliance. What happens to DSH eligibility during the transition? How must sale proceeds be allocated by law? What consent processes are required, and what do they cost in time and deal complexity?

Step 2: Model Charity Care Obligations Across Multiple Scenarios

Charity care commitments in public hospital deals need to be modeled as ongoing financial obligations, not footnotes. Build three scenarios: current obligation level, a 15% increase in uninsured volume (a reasonable planning assumption given coverage market instability), and a scenario where DSH payments are disrupted during the transition period.

Those three scenarios produce a range of charity care financial exposure that can be incorporated into deal economics before pricing is finalized. This is also where Florida healthcare expansion capital ROI modeling intersects directly with transaction structure, because the capital commitment needs to absorb both growth investment and safety-net obligation simultaneously.

Step 3: Quantify the Community Benefit Documentation Burden

Academic medical centers generate significant community benefit through research, education, and health professions training that qualifies for IRS Form 990 Schedule H credit. That is a genuine financial advantage of the academic partnership structure. But documenting and reporting that benefit adds administrative burden that needs its own budget line.

If the acquiring entity is a state university, the reporting framework may differ materially from what a nonprofit hospital finance team is accustomed to. That transition needs a responsible owner and a budget before the deal closes, not after the first Schedule H filing is due.

Step 4: Stress-Test the Long-Term Investment Commitments

In the FSU deal, a significant portion of the $1.7 billion long-term investment projection relies on grants and donations that have not yet been secured. That is not unusual in academic partnership structures. Philanthropic and research funding is a real and legitimate source of academic medical center capital. But it is not guaranteed.

CFOs evaluating similar structures should model a scenario in which grant and philanthropic revenue comes in at 60% of projection. What does the facility investment plan look like under that scenario? Which obligations remain contractually firm, and which are contingent on funding that may not arrive on schedule?

Step 5: Establish Clear Operational Accountability Before Closing

The FSU structure separates asset ownership from operational responsibility. FSU would own the property; TMH would operate the hospital. That is a defensible structure that can work well when designed correctly. But it requires explicit documentation of who is accountable for what, and what happens when those responsibilities conflict.

Revenue cycle, payer contracting, staffing, and quality performance are operational functions that directly affect financial performance. If the operating entity and the asset owner have different priorities or different financial pressures, that tension needs a written resolution mechanism before closing. Not addressed when a dispute arises.

For a detailed look at what comes after a hospital deal closes and how finance teams structure post-close accountability, the framework applies directly to split-ownership structures like this one.

If you are evaluating a hospital transaction involving a government entity, academic partner, or publicly owned assets, the financial complexity extends well beyond standard M&A due diligence. HFI Consulting works with healthcare finance leaders on deal structure analysis, charity care obligation modeling, and community benefit documentation frameworks. Visit hfi.consulting to learn more or connect directly.

What the Broader M&A Wave Means for CFOs

The FSU situation is playing out against a backdrop of significant consolidation activity. The week of May 4 alone included Sanford Health and North Memorial Health signing a definitive agreement to combine into a single nonprofit system, Atrium Health and WakeMed announcing merger plans with a $2 billion investment in Wake County, UPMC signing to acquire Trinity Health System in Ohio, and Christus Health completing its takeover of Titus Regional Medical Center in Texas.

Each of these deals carries its own financial complexity. But government and academic deals add a layer of statutory accountability that commercial transactions do not carry. The accountability obligation runs not just to shareholders or board members, but to the public and, in many cases, to statute.

The FSU lawsuit is a useful data point for every CFO engaged in M&A work. A deal that looked straightforward from a strategic standpoint - a university building out its medical school, a city hospital finding a capital-rich partner - is now in litigation because the process did not follow the statutory requirements governing public hospital assets in Florida.

The financial impact of that litigation is not just legal fees. It is delay, uncertainty, potential restructuring of deal terms, and the cost of community trust that takes years to rebuild when a deal is perceived as having shortchanged the people it was supposed to serve.

The Revenue Question That Belongs in the Model

The long-term revenue trajectory of an academic medical center partnership depends on answering one question that rarely appears in the initial deal analysis: what does this institution need to look like in 10 years to make the investment worthwhile?

For FSU, the answer involves specialty care expansion, research infrastructure, and reducing the need for regional residents to travel outside the area for advanced care. Those are legitimate goals. They also require clinical program investment, faculty recruitment, and research funding that take years to materialize into net revenue.

Academic medical centers carry higher operating costs than community hospitals. Faculty practice costs, research infrastructure, and graduate medical education overhead are real budget lines. The revenue premium on academic programs - tertiary and quaternary cases, research funding, teaching hospital reimbursement adjustments - is also real, but it develops over time.

CFOs evaluating these partnerships need a 10-year pro forma that reflects both sides of that ledger honestly. The FSU deal projects more than 900 jobs over three decades and $1.7 billion in investment. Those projections may be entirely achievable. They may also represent best-case assumptions that look materially different under a realistic scenario model. The only way to know is to build the model before signing.

For more on healthcare M&A financial frameworks, community benefit modeling, and capital commitment stress-testing, visit hfi.consulting.

P.S. For CFOs who have worked through government or academic hospital transactions: what was the most underestimated cost or obligation in the deal structure? Hit reply and tell me. The patterns across transactions are worth a follow-up piece.