What Congress Actually Said About Healthcare Costs: The AHA Testimony CFOs Need to Understand

The AHA quantified real cost pressures. Congress pushed back hard on consolidation. CFOs need to understand both sides of the record.

On March 18, 2026, the American Hospital Association put specific numbers behind cost pressures that hospital finance leaders have been managing for years. Supply costs up 9.9%. Drug expenses up 13.6%. Medicare margins at negative 12%. Congress heard those numbers. Then lawmakers turned around and asked whether hospital consolidation practices are a significant reason why healthcare costs so much in the first place.

That exchange — the AHA's cost pressure data meeting pointed congressional skepticism about provider market power — is the full record CFOs need to understand. Both sides of it will shape policy outcomes over the next two to three years.

The Setup: What Congress Is Actually Examining

This was the third in a series of Energy and Commerce Subcommittee hearings on healthcare affordability in 2026. Commercial health insurers testified in January. The prescription drug supply chain was up in February. March 18 was the provider installment — featuring testimony from the AHA, the American Medical Association, the American Academy of Family Physicians, the Purchaser Business Group on Health, UCSF Health, and the American Network of Community Options and Resources.

The tone was notably different from the insurer hearing. Lawmakers expressed genuine concern for the stability of U.S. hospitals and medical practices. But that goodwill had a limit. When the AHA's president and CEO attempted to defend provider consolidation, multiple subcommittee members pushed back directly. Rep. Kat Cammack, R-Fla., told him: "I think the data points to a completely opposite scenario than what you just painted."

Understanding the full dynamic of this hearing matters for CFOs in a way that reading only the AHA's prepared testimony does not. Provider organizations presented real and documented cost pressures. Congress simultaneously made clear it views certain provider business practices — particularly consolidation and site-specific billing differentials — as cost drivers that belong on the same ledger. Any legislative response will reflect both perspectives.

The section that follows translates the key data and arguments into planning implications. Where the AHA's testimony and congressional skepticism diverge, both sides are presented.

The Cost Reality the AHA Quantified for Congress

The AHA opened by describing an operating environment that finance leaders recognize immediately: more complex patients, rising input costs, and a reimbursement structure that has not kept pace with either.

Labor: Still the Dominant Cost Driver

Labor and workforce expenses represent roughly 60% of total hospital operating costs. Over the past five years, the AHA testified, these costs have risen sharply — first under pandemic strain, then under persistent workforce shortages. Experienced clinicians left the field. New pipeline supply has not caught up with demand.

The financial consequence is recruitment and retention spending that hospitals cannot fully offset through rate increases. The AHA noted that hospitals are leveraging AI tools to reduce administrative burden on clinical staff, but also acknowledged that infrastructure investment — workforce training, digital literacy — remains a gap.

Supplies and Drugs: Double-Digit Increases in One Year

Hospital spending on supplies increased 9.9% in 2025. Drug expenses grew 13.6% in the same period. These are not rounding errors. For a health system operating at 2-3% margin, a double-digit cost increase in either category is a structural problem, not a cyclical one.

Drug cost growth is being driven by two distinct dynamics: price increases on existing medications, and rapid adoption of new high-cost therapies — particularly in oncology and other specialty areas. The AHA noted that breakthrough treatments can cost tens of thousands to millions of dollars per patient, creating real tension between clinical obligation and financial sustainability.

Patient Complexity: The Volume-Acuity Combination

Recent federal actuarial data cited in the testimony reinforces a point that many healthcare finance leaders have been making internally: the rise in healthcare spending is overwhelmingly driven by higher use and intensity of services, not price inflation alone. In 2023 and 2024, medical inflation tracked roughly in line with general inflation. What changed is how sick the patients are and how many of them there are.

The AHA described a population that is older, managing more chronic conditions, and increasingly seeking care after years of pandemic-era deferrals. From a finance perspective, this means case mix index is shifting — and the revenue model built for a lower-acuity population is under pressure.

Reimbursement Gap: The $100 Billion Problem

Medicare underpayments to hospitals totaled more than $100 billion in 2024. The Medicare Payment Advisory Commission reports that Medicare margins for hospitals have dropped to negative 12%. The AHA characterized this as a payment system that is "increasingly misaligned with the realities of delivering care."

For CFOs who manage significant Medicare volume, this is not a new data point — but it is a data point that is now part of the congressional record and will anchor future reimbursement debates.

The Insurer Friction Layer

The AHA testimony dedicated significant attention to administrative burden from commercial health insurers — a topic that resonates differently depending on whether you sit on the provider or payer side of the table.

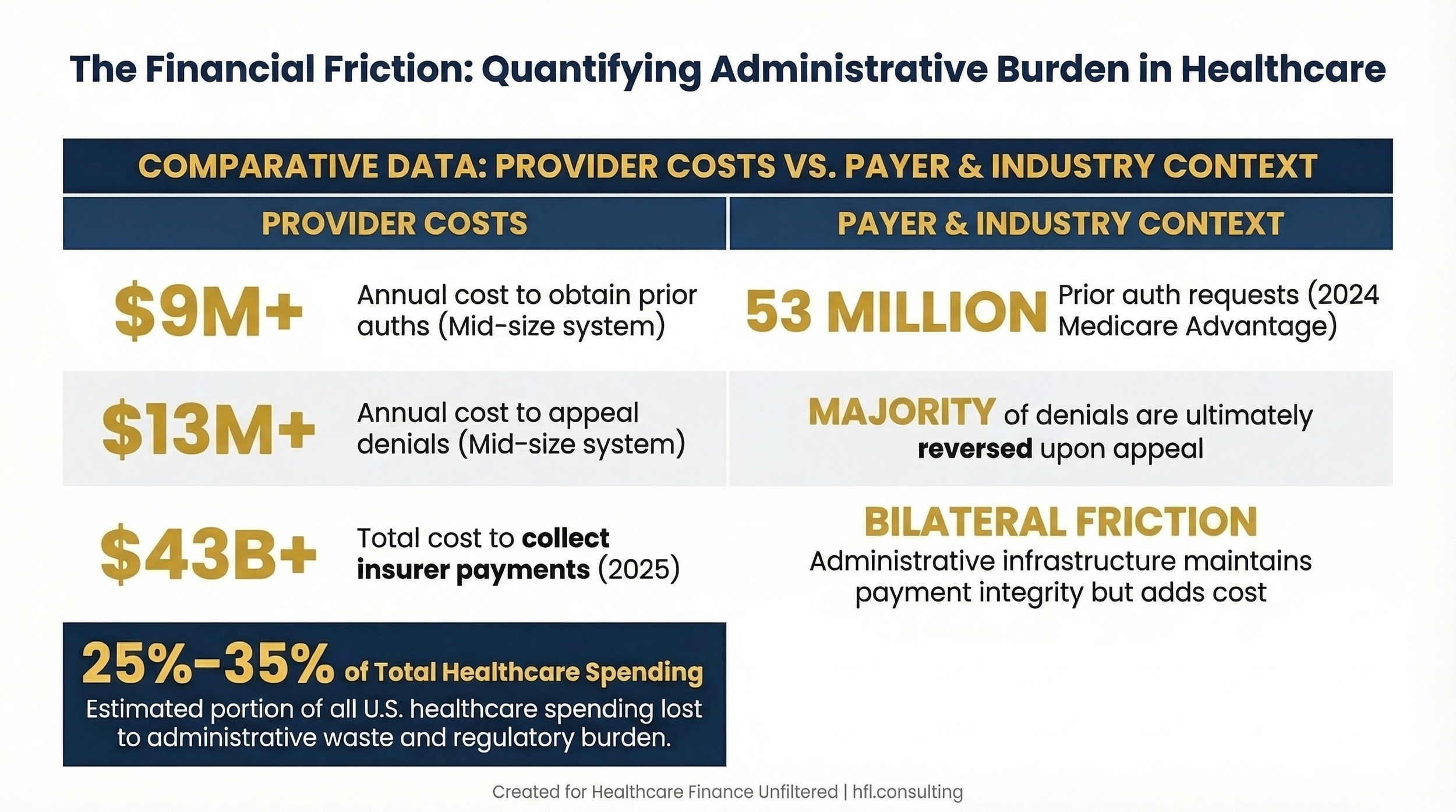

The numbers are notable. In the most recent CMS-reported year, Medicare Advantage plans made nearly 53 million prior authorization requests. The AHA estimates that hospitals spent over $43 billion in 2025 pursuing payment from insurers for care already delivered. One mid-sized health system reported spending more than $9 million annually to obtain prior authorizations and over $13 million appealing denials — the vast majority of which were ultimately overturned.

From the payer side, prior authorization exists as a utilization management tool and a cost control mechanism. Payer CFOs understand that MA plans are under pressure to manage medical loss ratios in a rate environment that has been increasingly constrained. The administrative infrastructure surrounding authorization and claims adjudication is not simply friction — it is also the mechanism through which payment integrity is maintained.

What the AHA testimony signals, and what both provider and payer finance leaders should track, is that congressional scrutiny of these practices is intensifying. The hearing series that included both insurers and providers creates a legislative record that may produce reform pressure in the next session.

In my work at Florida Blue Medicare on the payer side, I saw firsthand how authorization workflows are built for legitimate clinical and financial reasons — and also how the manual touchpoints create real cost on both ends of the transaction. Standardization of these processes is a solution that both sides should be able to support in principle.

Quantifies the bilateral cost of administrative complexity without framing either side as the villain

The Four-Part Solution Framework the AHA Proposed

The AHA organized its recommendations into four categories. Finance leaders should understand each as both a policy position and a potential operational signal.

1. Improving Community Health and Preventing Costly Interventions

The AHA cited data showing the costliest 5% of the population accounts for roughly half of all healthcare spending, and the most expensive 1% of patients is responsible for over 21% of costs. The proposed solution: expand preventive care capacity, support care coordination for high-need patients, and reduce financial barriers that cause patients to defer care until they need emergency services.

For CFOs, the financial logic is sound — preventing a $40,000 hospitalization by funding a $200 care coordination visit is straightforward math. The challenge is the capital structure and the reimbursement model. Fee-for-service doesn't pay for the visit that prevents the admission. Value-based arrangements can, but they require infrastructure and risk tolerance that not every system currently has.

2. Advancing Value Through Care Transformation

This pillar covers transitioning to value-based models, expanding palliative care, and reforming malpractice law to reduce defensive medicine. The AHA noted that malpractice-related costs are estimated at 2.4% of all U.S. healthcare spending — approximately $135 billion in 2025 — driven in part by a legal environment that incentivizes defensive testing and procedures.

Malpractice reform is a long-standing policy debate with little recent federal momentum. What is more immediately relevant for CFOs is the value-based care transition piece. The direction of CMS and commercial payers is clear: more of the risk is moving to providers over time. Understanding your organization's readiness for that shift is a strategic finance question, not just a clinical one.

3. Reducing Regulatory and Administrative Waste

The AHA estimated that administrative burden — including contracting infrastructure, revenue cycle management, compliance and reporting, and prior authorization processes — now accounts for 25%-35% of all healthcare spending. The solutions proposed include standardizing authorization processes, pursuing direct contracting arrangements, and deploying AI for documentation and scheduling.

This is the category where CFOs have the most direct operational influence in the near term. Wherever your organization can standardize workflows, reduce redundant documentation, or automate low-value administrative tasks, the margin impact is real. The policy environment may change slowly, but internal operational improvements don't wait for Congress.

4. Innovating to Improve Care Quality and Outcomes

The AHA highlighted hospital-at-home, remote patient monitoring, advanced telehealth, and AI-assisted diagnostics as examples of innovation that can reduce spending by shortening lengths of stay and shifting care to lower-cost settings. The policy ask was for regulatory structures that accommodate these models and adequate payment for proven digital innovations.

For CFOs planning capital budgets, this signals continued pressure to evaluate technology investments not just as operational tools but as structural cost management strategies.

Where Congress Pushed Back: The Consolidation Question

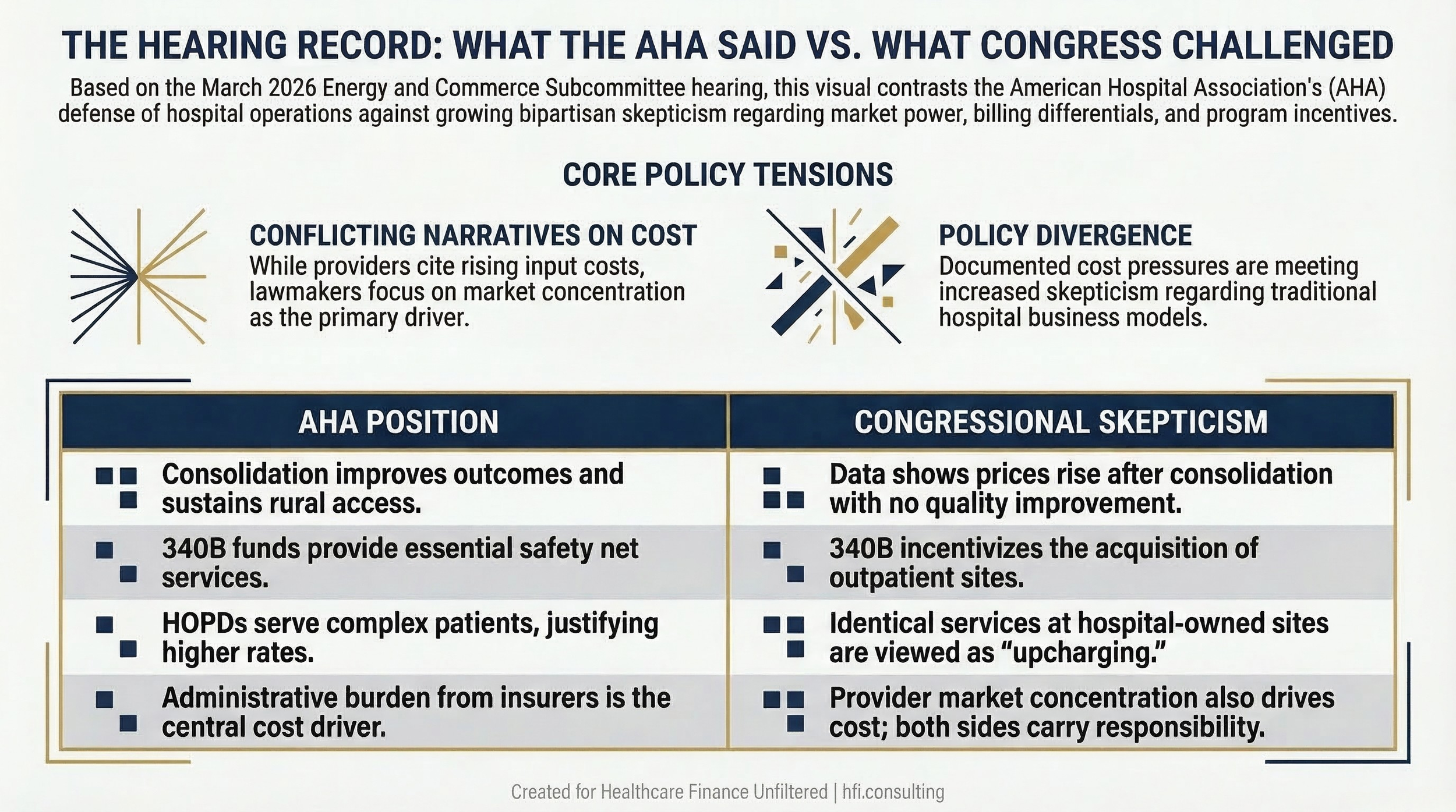

The cost data the AHA presented was largely accepted by subcommittee members. The AHA's defense of provider consolidation was not.

Hospital and provider spending represents more than half of total U.S. healthcare spending, and it is growing faster than healthcare spending overall. Regulators and market researchers have raised increasing concern that mergers and acquisitions among providers are contributing to that growth. Research cited at the hearing suggests that when hospitals acquire physician practices or regional hospitals, prices rise — without corresponding improvements in quality.

AHA CEO Rick Pollack argued that consolidation benefits providers and patients: some physicians choose acquisition to offload administrative burden, some rural hospitals affiliate to stay financially viable, and combined systems show better readmission and mortality outcomes. Lawmakers were unmoved.

The consolidation critique focused on two specific financial mechanisms that CFOs should understand clearly, because both are now in active congressional crosshairs.

Facility fee arbitrage. Hospitals can charge Medicare more for a service delivered at a hospital-owned outpatient site than a non-hospital-owned facility is permitted to charge for the identical service. Elizabeth Mitchell, president and CEO of the Purchaser Business Group on Health — which represents large employer purchasers — put the legislative argument plainly: "A band-aid is a band-aid. A CT scan is a CT scan. And yet they are upcharging because they can." She characterized hospital pricing more broadly as "utterly irrational" and "not related to quality, not related to safety."

For CFOs managing outpatient department portfolios, this is the core financial logic behind site-neutral payment reform. Mitchell testified that equalizing payment rates between hospital-owned and independent outpatient sites could save Medicare billions. The AHA's counter — that HOPDs serve sicker patients and operate under more rigorous regulatory standards — is substantively valid. Congress heard it and appeared unpersuaded.

340B as a consolidation incentive. The 340B drug discount program, which the AHA testified should be protected, received a different reception from Rep. Buddy Carter, R-Ga., who called the program's role in driving hospital acquisitions a "big, big problem." The concern: hospitals have financial incentive to acquire outpatient settings in part because acquisition extends their 340B eligibility to additional dispensing locations, increasing the discount benefit. What the AHA frames as a safety net tool, some lawmakers frame as a market distortion embedded in federal law.

The physician independence thread. A separate but related dynamic ran through the hearing. Just over 42% of physicians worked in private practice in 2024, compared to more than 60% in 2012. Neurosurgeon Anthony DiGiorgio of UCSF Health testified that the current reimbursement and administrative environment has made independent practice financially nonviable: "The system essentially starves independent practices of revenue while burying them in paperwork, making selling to the hospital the only way out."

The AMA and the American Academy of Family Physicians both called on Congress to reform Medicare physician reimbursement so that annual updates more adequately track inflation — a long-standing lobbying position that has not produced results, but that the hearing record now reinforces.

For health system CFOs, the physician employment trend is already a balance sheet reality. For finance leaders at independent practices or systems that contract with independent physicians, this hearing signals that the structural economics of independent practice are not going to improve without federal action — and that action is not guaranteed.

The Hearing Record: What the AHA Said vs. What Congress Challenged

The Policy Battles Finance Leaders Must Track

The hearing produced a more complex picture of the 340B and site-neutral debates than the AHA's prepared testimony alone would suggest. Both issues are now framed in the congressional record with competing arguments — and CFOs need to understand both sides when building financial scenarios.

340B: Safety Net Tool or Consolidation Incentive?

The AHA made a pointed request: oppose any effort to convert 340B pricing from an upfront discount model to a back-end rebate model. Under the rebate approach, hospitals would purchase drugs at full price and recover discounts after dispensing — a cash flow and administrative burden problem that would be acute for facilities without substantial reserves.

That position received a harder reception in the hearing room than in the written testimony. Rep. Carter framed 340B's role in driving hospital acquisitions as a "big, big problem" — a characterization that signals congressional appetite to reform the program in ways that go beyond the rebate vs. discount debate the AHA has focused on.

For hospitals that rely on 340B to fund safety net services, both risks are real and require separate financial modeling. The rebate conversion question is the near-term operational threat. The broader acquisition incentive critique is a longer-cycle legislative risk. 340B Program Update: Rebate Model Dead, But Manufacturer Data Demands Escalate

Site-Neutral Payments: The Billing Gap Congress Wants to Close

The AHA strongly opposed site-neutral payment policies that would align Medicare reimbursement for hospital outpatient departments with physician office rates. The argument: HOPDs serve sicker, more complex patients and operate under more rigorous regulatory requirements — costs that justify differential payment rates.

The Purchaser Business Group on Health offered the direct counter at the same hearing: the billing differential between hospital-owned and independent outpatient settings is not clinically justified for comparable services. The employer purchaser community is one of the most politically organized constituencies in healthcare policy — and they were in the room making that argument alongside hospital lobbyists.

Site-neutral cuts would represent billions in Medicare reductions for health systems with significant outpatient volume. Hospital Facility Fees Under Siege: CFO Playbook for the $172 Billion Medicaid Cut The hearing made clear that the political support for site-neutral reform is broader than the AHA's opposition can simply hold back. If your organization has not modeled this scenario, do it now.

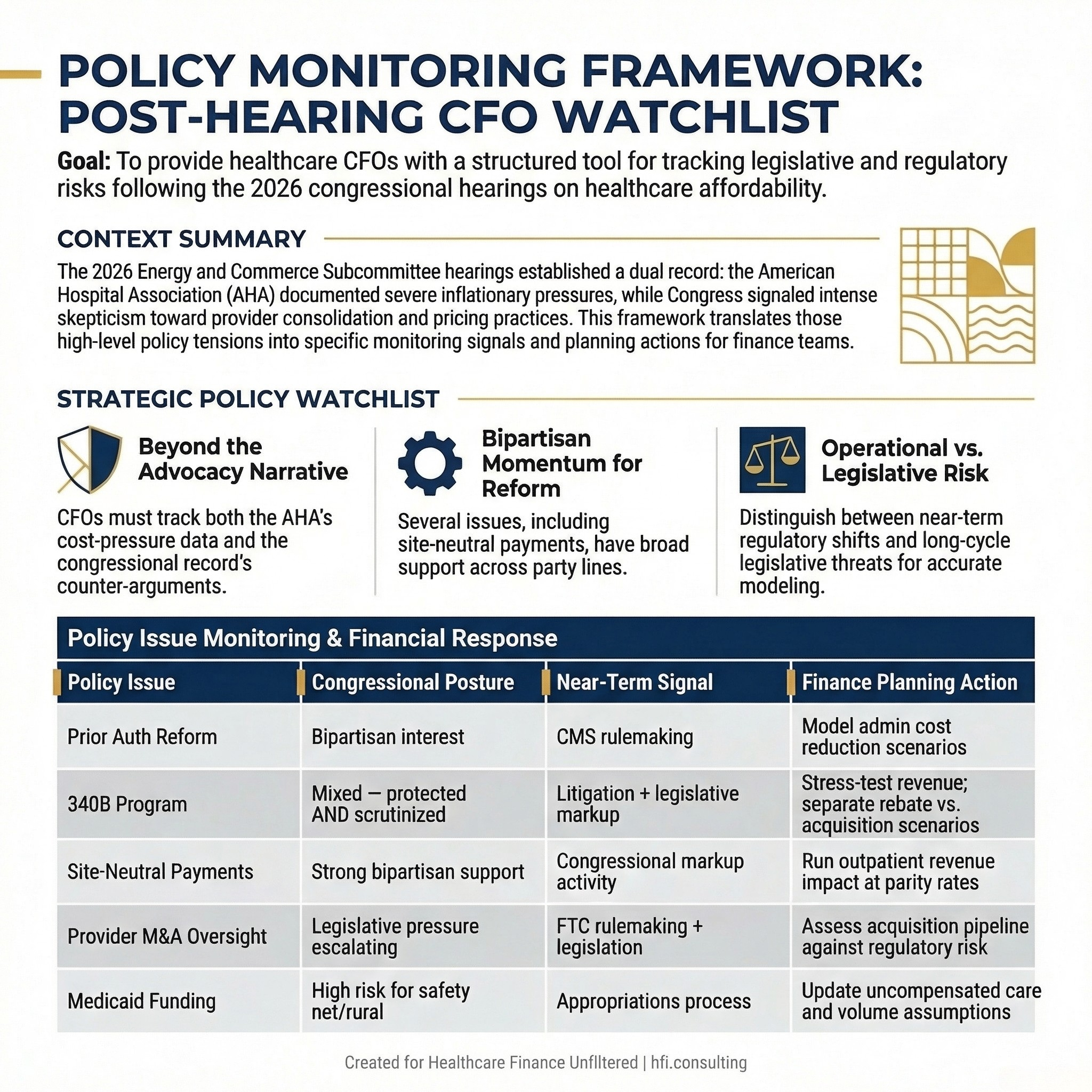

What to Watch Over the Next Six to Twelve Months

Congressional hearing series like this one typically produce one of three outcomes: targeted legislation, broader reform packages that stall, or a formal record that informs regulatory action. The healthcare affordability series is still active — this was the third installment, with no announced conclusion.

The specific items most likely to see near-term movement:

Prior authorization standardization has bipartisan interest. Watch for CMS rulemaking as the most likely vehicle rather than direct legislation.

340B program reform is now a two-track risk: the rebate model debate and congressional concern about acquisition incentives. Budget planning should include a scenario for reduced 340B benefit value, not just a scenario for administrative disruption.

Provider consolidation oversight is moving from regulatory to legislative. The Federal Trade Commission has been the primary enforcement mechanism to date, but the hearing record now includes direct congressional pressure on hospital M&A. Finance teams at health systems with active acquisition strategies should model the regulatory risk alongside the operational thesis.

Site-neutral payment cuts carry measurable bipartisan support and an organized employer-purchaser lobby actively pushing for them. This is not a speculative risk.

Medicaid funding changes are the most significant near-term risk for safety net hospitals and rural systems. Rural Hospitals Already in the Red: How Medicaid Changes Will Push Them to the Brink The congressional record includes testimony documenting compounding pressure from both existing Medicaid underpayment and potential structural funding changes.

CFO Monitoring Framework

What This Means for Your Budget Planning

The congressional record from this hearing contains two different cost stories. The AHA's story: hospitals are absorbing double-digit cost increases in supplies and drugs, operating at negative 12% Medicare margins, and spending $43 billion annually on administrative collection. Congress's story: provider consolidation is driving prices up without quality improvement, facility fee differentials are not clinically justified, and 340B is functioning as an acquisition subsidy.

Both stories have supporting evidence. Budget planning needs to account for both.

Four near-term actions are worth prioritizing regardless of where you sit on the provider spectrum.

First, model your site-neutral exposure. If your system has significant outpatient department volume billed at hospital rates, calculate what revenue looks like under a scenario where those rates are equalized with physician office rates. This is not a hypothetical risk — it has organized bipartisan support and employer purchaser lobby backing.

Second, separate your 340B scenarios. The rebate model threat and the acquisition incentive critique are two distinct legislative risks with different timelines and different financial impacts. Build them as separate sensitivity analyses, not one combined scenario.

Third, quantify your administrative cost footprint. The AHA's figure of 25%-35% of all healthcare spending going to administrative functions is a system-level estimate, but your organization's specific burden is knowable. Understanding where revenue cycle, authorization, and compliance costs sit relative to benchmark gives you a basis for internal optimization regardless of what Congress does.

Fourth, if your organization has active M&A strategy, assess it against an escalating regulatory environment. The FTC has been the primary enforcement tool to date, but the congressional record now includes direct legislative pressure on provider consolidation. That expands the regulatory surface area.

If you are actively modeling the cost scenarios raised in this hearing, I'd like to hear where you are running into the most analytical friction. Hit reply and tell me — what's the hardest scenario to build right now, and what data are you missing?

The Broader Picture

The hearing series the Energy and Commerce Subcommittee is running in 2026 has now put every major healthcare stakeholder on the congressional record — insurers, drug supply chains, and providers. The political dynamics differed by session: insurers faced the most pointed questioning, providers faced genuine concern paired with sharp skepticism about consolidation.

What the full record establishes is that Congress is not looking at any single cost driver in isolation. Insurer administrative practices, drug pricing, and provider market power are all on the table simultaneously. Legislative responses may be incremental or they may be structural, but they will almost certainly touch more than one of these pressure points.

For finance leaders, the practical implication is to build financial scenarios that reflect the full range of policy risk — not just the risks your organization's trade association lobbied against. The cost pressures the AHA documented are real. So is the congressional appetite to examine the business practices that critics argue compound them.

Healthcare Finance Unfiltered covers the regulatory and financial developments that affect hospital and health system budgets — with the analysis that helps you move from headline to action. If this framework was useful, subscribe to get the next one delivered directly to your inbox.

P.S. The hearing record now contains both the cost pressures hospitals documented and the consolidation practices Congress challenged. Which of those two sides of the ledger is your organization better prepared to respond to right now? Hit reply.