Why Your Value-Based Care Contracts Never Pay Out as Planned

The attribution gaps and data delays are driving provider VBC shortfalls, plus a CFO framework to close them.

Your health system signed a value-based care contract. The modeled upside was real. The shared savings scenario your team ran looked achievable. And the reconciliation check that arrived was a fraction of what the model projected.

If that scenario is familiar, the problem probably isn't your clinical performance. It's the financial infrastructure underneath the contract — and the parts of it your team has the leverage to control.

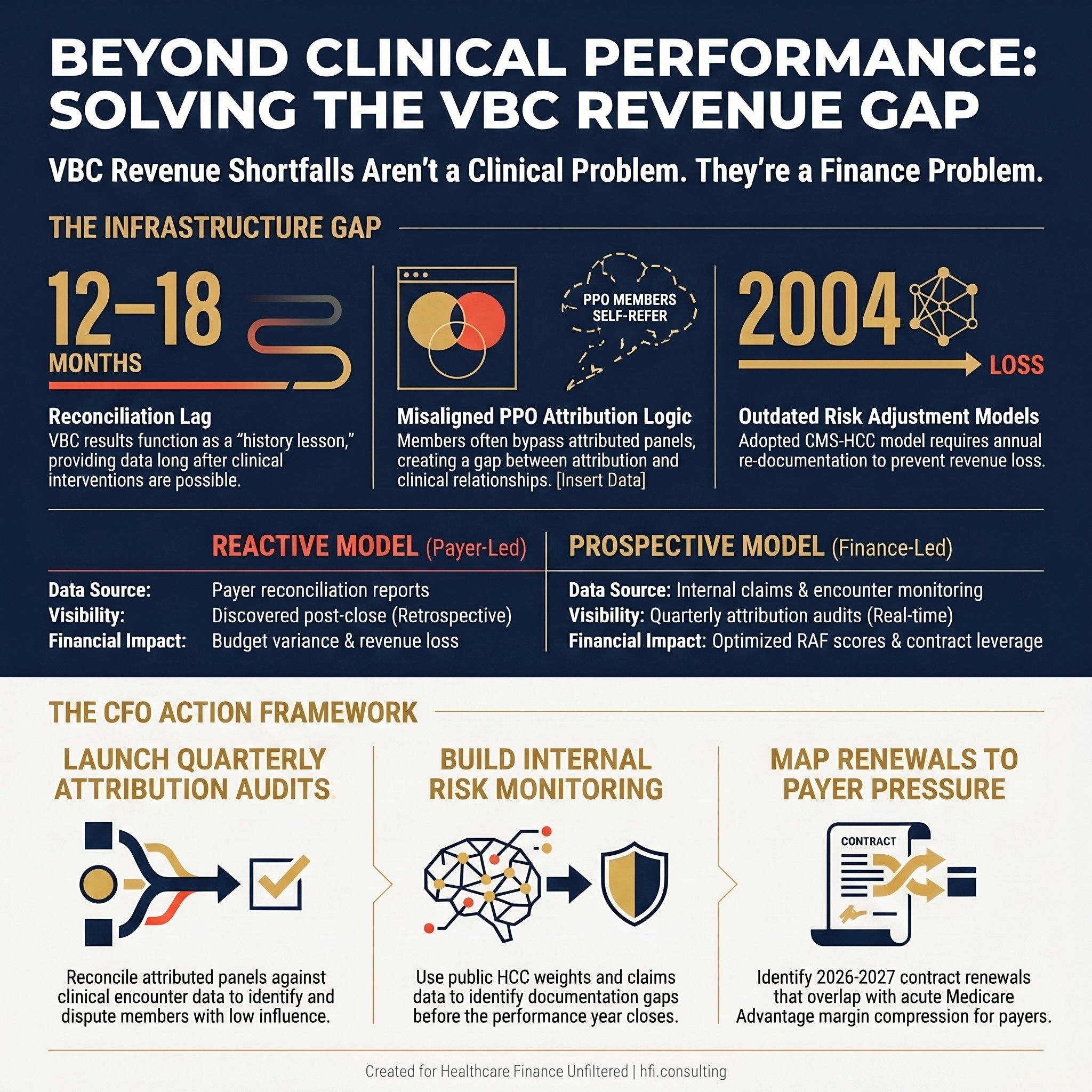

Stat card highlighting that VBC revenue shortfalls are a finance infrastructure problem, not a clinical performance problem

What VBC Is Supposed to Do (And Why It Sounds Better in Theory)

Value-based care was designed to solve a concrete problem: fee-for-service reimbursement pays for volume, not outcomes. Under traditional FFS, a hospital earns more revenue from a readmission than from preventing one. VBC flips that incentive structure by tying payment to quality metrics, cost efficiency, and population health outcomes across an attributed member panel.

The model has been part of the conversation since the early 2000s, and most healthcare finance professionals have spent the bulk of their careers operating in some version of it. That longevity is part of why the persistent underperformance is so frustrating. VBC is not new. Health systems have had time to figure it out. And yet the gap between contracted upside and actual reconciliation results keeps showing up in budget variance reports.

The theory is sound. The execution is where it consistently breaks down.

Three Places Where Provider VBC Revenue Goes Missing

Attribution Logic That Was Never Built for PPO Members

The most durable VBC math problem is attribution — the process by which a payer assigns members to a provider panel for the purpose of measuring cost and quality performance.

Attribution works reasonably well in HMO environments where patients designate a primary care physician and that PCP functions as a genuine gatekeeper. Referrals flow through the PCP. The care relationship is documented. The attribution reflects something close to clinical reality.

In PPO plans, member behavior is structurally different. Members self-refer to specialists. They see multiple physicians across the same condition and often across different networks. Many commercially insured patients use cardiologists, rheumatologists, and orthopedic surgeons as their functional primary care relationship — not because those providers are their assigned PCPs, but because that is where their chronic conditions are actually being managed.

The attribution model does not capture that. It assigns members based on plurality of claims or designated PCP, not on where the clinical relationship actually lives. When a provider's attributed panel includes members who are getting the majority of their care elsewhere, the cost and quality metrics applied to that provider reflect utilization patterns that provider had limited ability to influence.

This is a structural design problem, not a data error. Most health systems are not systematically quantifying the gap between their attributed panel and the members they have a genuine clinical relationship with — and that gap is where a significant share of VBC reconciliation shortfalls originate.

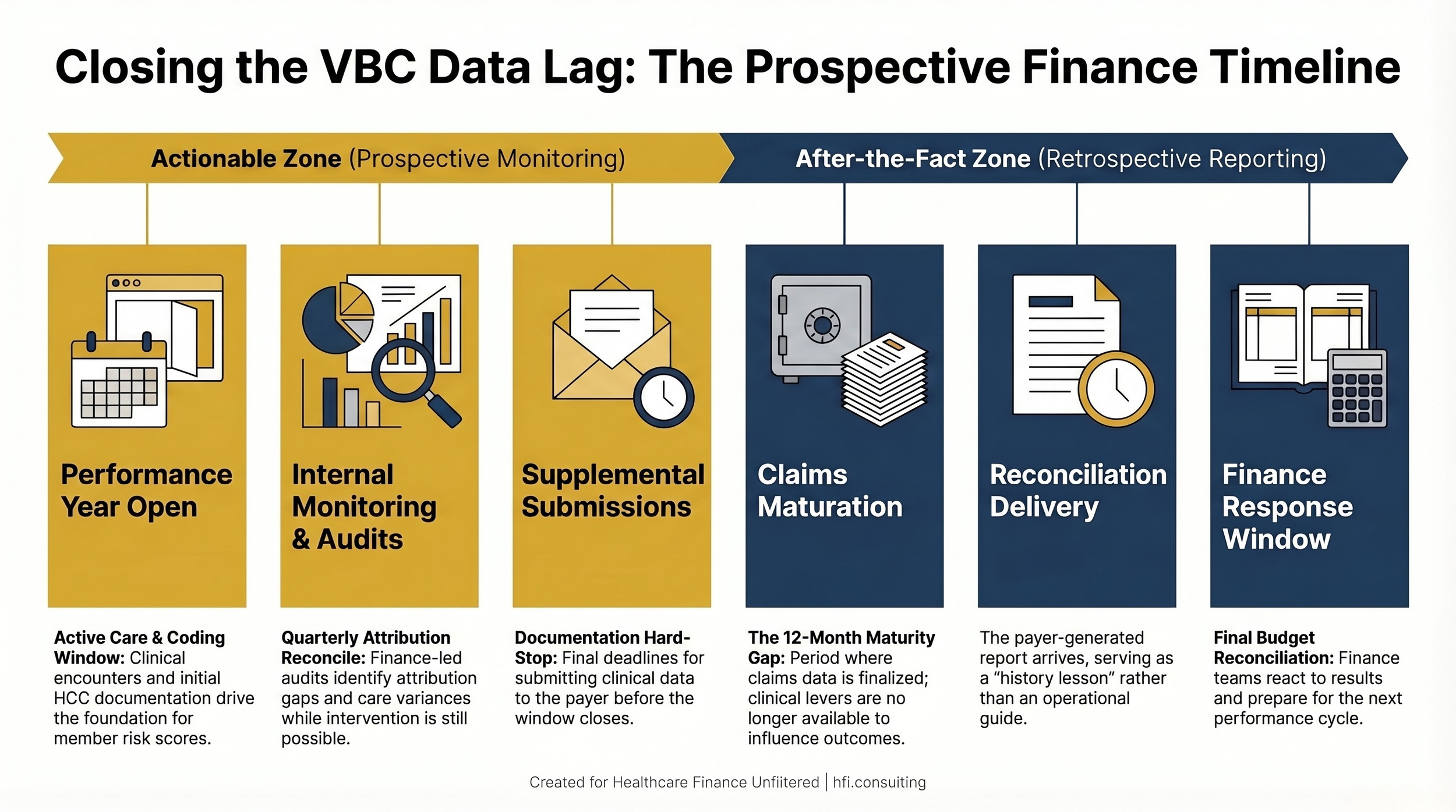

Data Lag That Turns Reconciliation Into a History Lesson

VBC reconciliation runs on a significant delay. Claims data takes time to mature. Supplemental data submissions have deadlines that fall well after the close of the performance year. By the time a health system sees final reconciliation figures, the clinical decisions driving those results were made 12 to 18 months earlier.

Finance leaders evaluating their VBC performance using payer-generated reconciliation reports are working with a retrospective signal. When underperformance surfaces, the interventions that could have changed the outcome are already out of reach.

The providers who close this gap build their own performance monitoring infrastructure rather than waiting for payer reports. CMS publishes significant amounts of program data publicly. The Shared Savings Program and ACO REACH Model provide data feeds for organizations in those arrangements. For commercial VBC contracts, claims data provisions in most agreements allow for supplemental reporting access. The analytical capacity exists at more health systems than are actively using it.

Timeline showing the VBC reconciliation cycle and the 12-18 month gap between performance and financial visibility

The Commercial Contract Rollup Problem

At multi-hospital systems, VBC contract performance frequently rolls into commercial payer reporting at the large group level. That is a common structure and it is not inherently a problem — but it means the VBC line is visible only if your finance team knows to break it out.

Teams that are not specifically tracking VBC performance as a discrete category often discover their exposure at reconciliation rather than mid-year. By then, the levers available for intervention are limited. This is an operational data integrity challenge as much as a clinical performance issue — and it lives squarely in the finance function's responsibility.

Why 2026 Changes the Negotiating Environment

Medicare Advantage margins are compressing. CMS rate adjustments, post-pandemic utilization normalization, and tighter medical loss ratio benchmarks are putting MA plan financials under pressure that is visible in public filings and plan strategic communications.

Payers managing MA margin pressure will look to other lines of business to offset it. That includes commercial VBC contracts, where negotiation dynamics are less constrained by CMS regulatory structure. Shared savings thresholds, performance benchmarks, and attribution methodology provisions tend to shift when the payer is managing a margin recovery strategy across its full product portfolio.

Provider CFOs who built their VBC revenue assumptions on historical contract terms may find that renewal negotiations in 2026 and 2027 look materially different. This is a predictable response to payer financial dynamics, not a speculative risk. Finance leaders who are modeling it now — and building their own performance data to bring into renewal discussions — will be in a structurally better negotiating position.

For a detailed look at how MA rate changes are already affecting provider planning assumptions, see Medicare Advantage 2027 Rate Changes: Strategic Planning Guide for Provider Finance Leaders.

What Providers Are Not Using: The Claims Data Unlock

This is where the conversation moves from diagnosis to action.

CMS publishes substantial program data publicly. The HCC weights that drive RAF score calculations are available. Benchmark methodologies for ACO and value-based programs are documented. For providers in commercial VBC arrangements, most contracts include claims data access provisions that go largely underutilized.

The analytical infrastructure to use this data exists at more health systems than are actively deploying it. Large systems often employ actuarial staff. Regional systems have access to analytics vendors and EHR-integrated data platforms. The question is whether the VBC performance problem has been framed as a finance problem requiring analytical investment — or whether it has been delegated entirely to the clinical quality function.

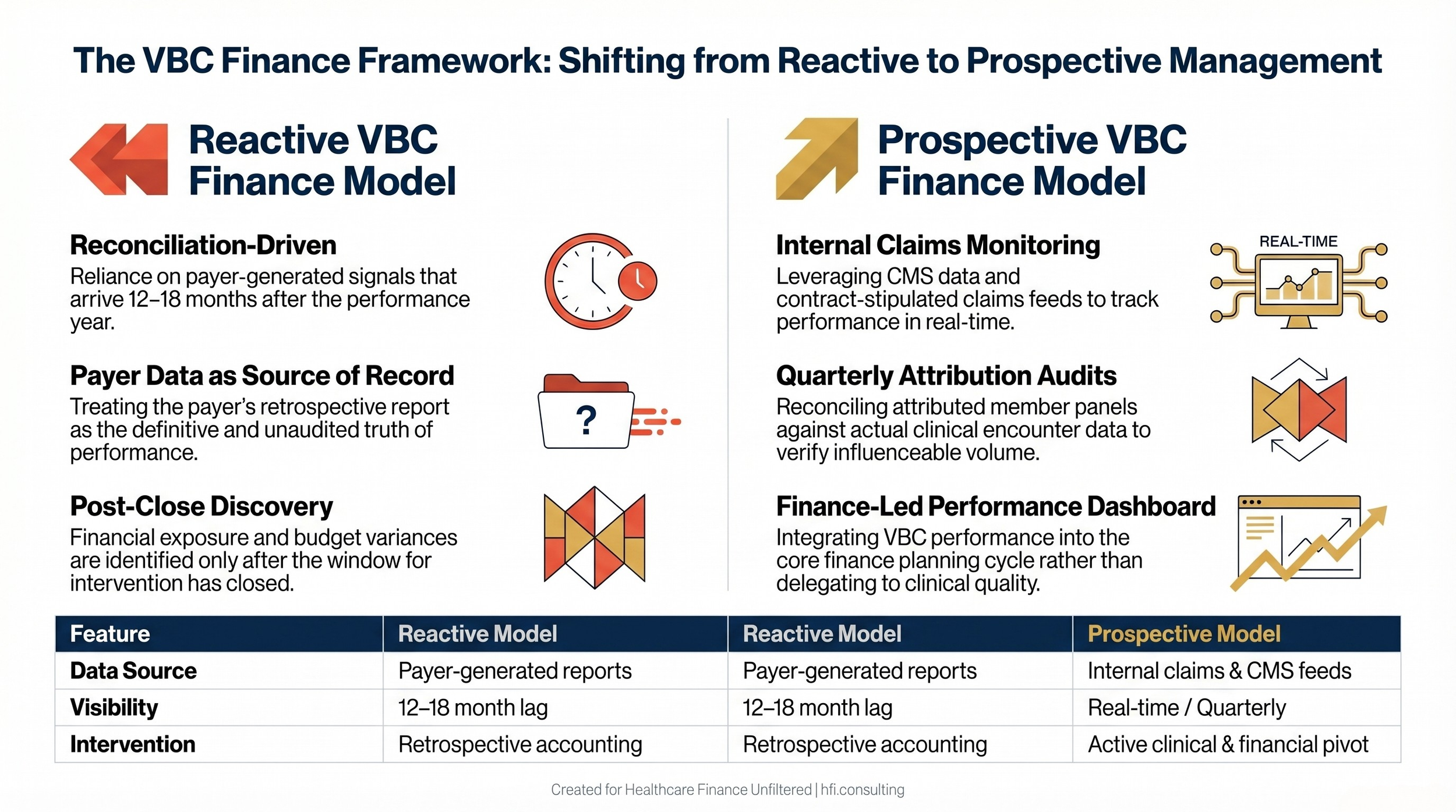

Finance leaders who treat VBC reconciliation as a retrospective accounting event will always be behind. Finance leaders who build prospective claims-based monitoring into their planning cycle can identify attribution anomalies, care gap patterns, and cost trend variances while there is still time to act on them.

During my time as a Business Advisor for McKesson (now Change Healthcare) during Performance Analytics implementations, the providers who were most frustrated with VBC were not the ones with the worst clinical outcomes. They understood the theory. They were executing on quality metrics. What they lacked was financial visibility into where their actual performance stood between reconciliation cycles. The analytics infrastructure existed. The connection to the finance planning process had never been built.

Side-by-side comparison of reactive versus prospective VBC finance management approaches

Building Your Own Risk Adjustment Picture

The American College of Physicians published a position paper in July 2025 calling for modernization of the CMS-HCC Risk Adjustment Model. One of the core recommendations addresses the "zeroing out" of HCC codes at the start of each calendar year — a provision that requires chronic conditions to be re-documented annually to maintain their contribution to a patient's risk score.

That annual reset creates a predictable documentation gap. Conditions that were captured in year one drop out of the risk profile in year two if they are not re-documented. For providers managing VBC contracts tied to member risk scores, this means that documentation completeness is not a clinical records issue — it is a revenue issue.

Provider finance teams can build internal tools that compare their attributed panel's documented HCC burden against the risk scores flowing back from payers on those members. The HCC weights are public. The RAF score data is typically included in payer contract data exchange. A system with actuarial or advanced analytics capacity can construct a basic risk adjustment monitoring table that identifies documentation gaps and attribution discrepancies before reconciliation closes.

The goal is not to replicate the payer's calculation. It is to identify where your panel's clinical complexity is being underrepresented in the risk adjustment model — and to surface that gap while the performance year is still open.

The Kaiser $556 million Medicare Advantage settlement involved coding practices on the payer side. The inverse problem — providers leaving RAF value on the table because of documentation gaps rather than overcoding — is less visible in public enforcement actions but operationally significant for provider finance. For context on risk adjustment program integrity issues, see When to Sound the Alarm: What Kaiser's $556M Medicare Advantage Settlement Teaches Finance Leaders About Risk Adjustment Fraud.

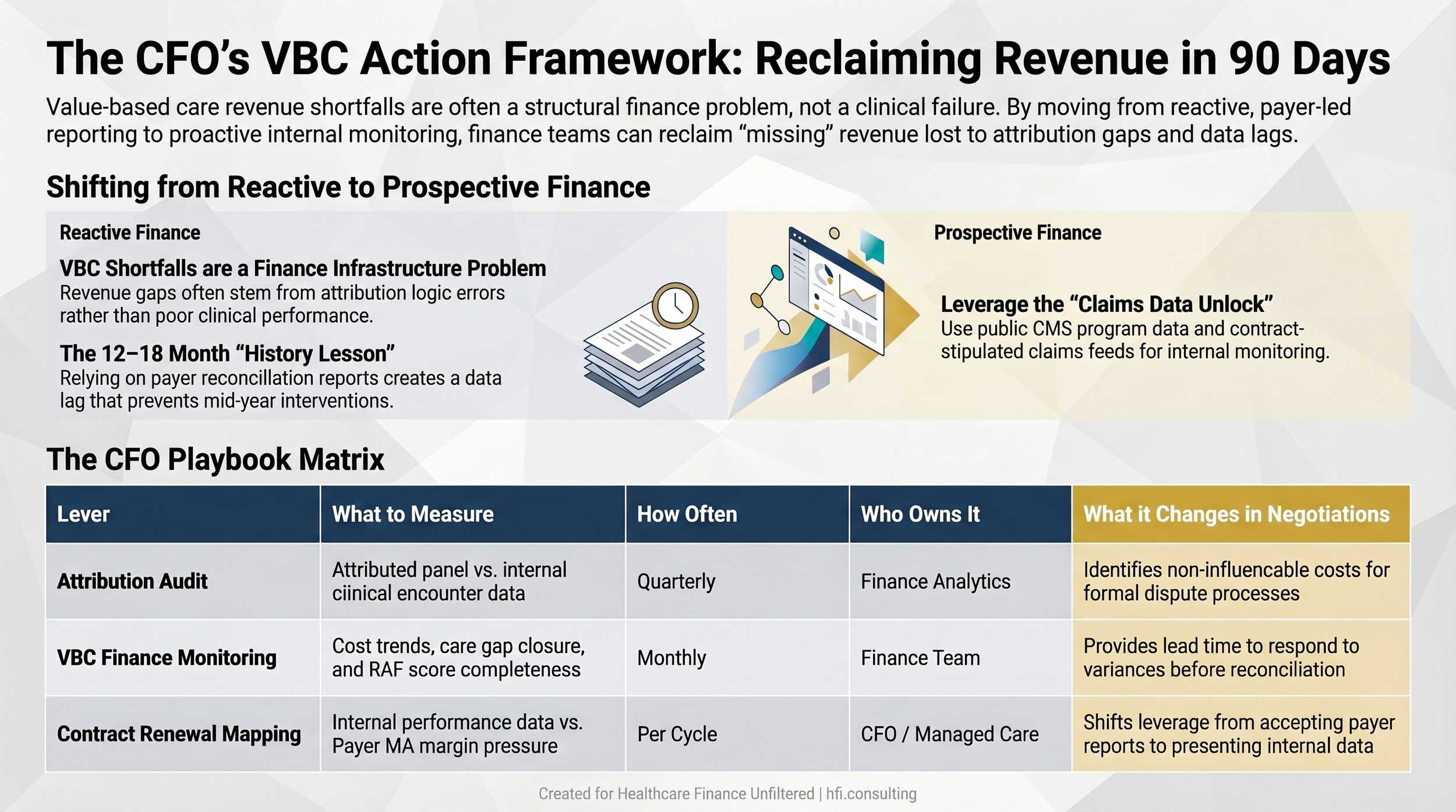

The CFO Playbook: Three Finance Levers for VBC Performance

Lever 1: Build an attribution audit process. On a quarterly basis, reconcile your attributed member panel against your clinical encounter data. Identify members attributed to your system with fewer than two documented encounters in the past 12 months. These are members whose VBC metrics are being measured against your contract but over whom you have limited clinical influence. Quantifying this exposure is the first step toward addressing it — either through outreach to re-establish the care relationship or through formal attribution dispute processes where your contract permits them.

Lever 2: Establish a VBC-specific finance monitoring function. VBC performance should not live exclusively in the CMO's office. Finance needs direct visibility into cost trends, utilization patterns, care gap closure rates, and risk score completeness before reconciliation. A monthly VBC finance dashboard that separates attributed panel performance from global quality metrics gives your team the lead time to respond.

Lever 3: Map contract renewals against payer financial cycles. When your VBC contracts come up for renewal, understand the payer's financial context. A plan absorbing MA margin pressure will negotiate differently than one in a growth phase. Provider finance leaders who walk into renewal discussions with their own performance data — including attribution gap analysis, documentation completeness metrics, and their own claims-based cost trend — negotiate from a materially different position than teams who accept the payer's reconciliation as the definitive record.

Three-lever CFO action framework for improving VBC contract performance and renewal positioning

Your VBC Revenue Is Not Irretrievable

The frustration most provider CFOs carry about value-based care is legitimate. The contracts are complex. The performance measurement window is long. The reconciliation data arrives late. And the attribution mechanics were designed for member behavior patterns that do not reflect how most commercially insured patients actually use care.

But "the system is imperfect" is not a planning framework.

The providers closing the gap between contracted VBC upside and actual reconciliation results are doing it with finance-led analytics, prospective monitoring, and rigorous attribution auditing. The tools are available. The CMS data is public. The actuarial capacity exists at most major systems. The gap is almost always organizational: VBC has been treated as a quality program when it is, at its core, a financial performance problem that belongs on the finance team's agenda.

If your VBC revenue shortfalls have become a recurring budget variance, the fix starts with your finance team taking ownership of the monitoring — not waiting for the next payer report to explain why the reconciliation came in light again.

Healthcare Finance Unfiltered covers payer strategy, revenue cycle finance, and the operational frameworks healthcare CFOs use to close the gap between policy complexity and financial performance. If this analysis is useful, subscribe to get the full breakdown delivered to your inbox — and forward it to the CFO who needs to hear this before their next VBC renewal.

Your Next 90 Days: Three Specific Actions

The MA margin pressure is building now. Commercial VBC contract renewals will reflect payer financial realities within the next 12 to 18 months. The window for building internal monitoring capacity before it becomes urgent is the current planning cycle.

Start here this quarter:

Pull your attributed member panel from each active VBC contract and compare it against your clinical encounter data. Quantify the attribution gap by payer and by contract.

Determine whether your system has actuarial or advanced analytics capacity that could be directed toward building a basic HCC documentation monitoring workflow.

Map your VBC contract renewal timeline against the 2026 to 2027 window and identify which renewals fall during the period when payer MA margin pressure will be most acute.

The VBC revenue that never came in as promised is not gone. In many cases it is sitting in documentation gaps, attribution anomalies, and reconciliation cycles that the finance function has not yet been equipped to manage.

Working through a VBC shortfall or preparing for a contract renewal? Reply and tell me what you're seeing. I read every response.

P.S. When your VBC contracts come up for renewal this cycle, will you be walking in with your own performance data — or accepting the payer's reconciliation as the only version of the story?