The Great Hospital Sell-Off: What the ASC Acquisition Spree Means for Every CFO's Balance Sheet

Major health systems are converting inpatient assets into ambulatory power. Here is what it costs everyone else.

Three of the largest health systems in the country are actively dismantling their hospital portfolios and funneling billions into ambulatory surgery centers. Tenet sold 14 hospitals for more than $4.8 billion. Ascension has shrunk its hospital footprint from 139 facilities to 90 while closing a $3 billion deal to acquire 250 ASCs. Community Health Systems is offloading nine more hospitals while simultaneously opening new surgery centers in new markets. This is not a trend. It is a structural recapitalization of American healthcare, and it is happening right now on every CFO's balance sheet whether they are participating or not.

Bar and stat comparison showing Tenet, Ascension, and CHS hospital divestitures and ASC investment totals in 2025-2026.

Why Health Systems Are Choosing Ambulatory Over Inpatient

The calculus is straightforward on paper. Medicare reimburses a basic colonoscopy with biopsy at approximately $805 in an ambulatory surgery center and $1,371 in a hospital outpatient department. That is a 70 percent premium for the same clinical procedure in a different building. Health systems have spent decades building toward that HOPD premium through physician employment, facility designation, and payer contract leverage. Now the payer landscape, the regulatory environment, and the patient preference data are all moving against them simultaneously.

Patients are choosing ASC-level settings at increasing rates for orthopedic, spine, and cardiovascular procedures that once filled inpatient beds. Independent clinical practices face cost pressures they cannot absorb alone. When a health system acquires an independent ASC, it immediately converts that center's payer contracts from independent rates to system master service agreements, capturing a significant commercial rate premium per case. It frees up inpatient OR blocks for the complex, high-acuity tertiary cases that cannot be shifted to ambulatory settings.

The result is a portfolio reshaping strategy that looks defensive and offensive at the same time. Sell the lower-margin inpatient asset. Acquire the ambulatory access point. Absorb the ASC into system payer contracts. Capture the commercial rate differential.

The Revenue Cycle Friction No One Wants to Discuss

The acquisition rationale holds up in the boardroom. The execution is considerably messier in the revenue cycle.

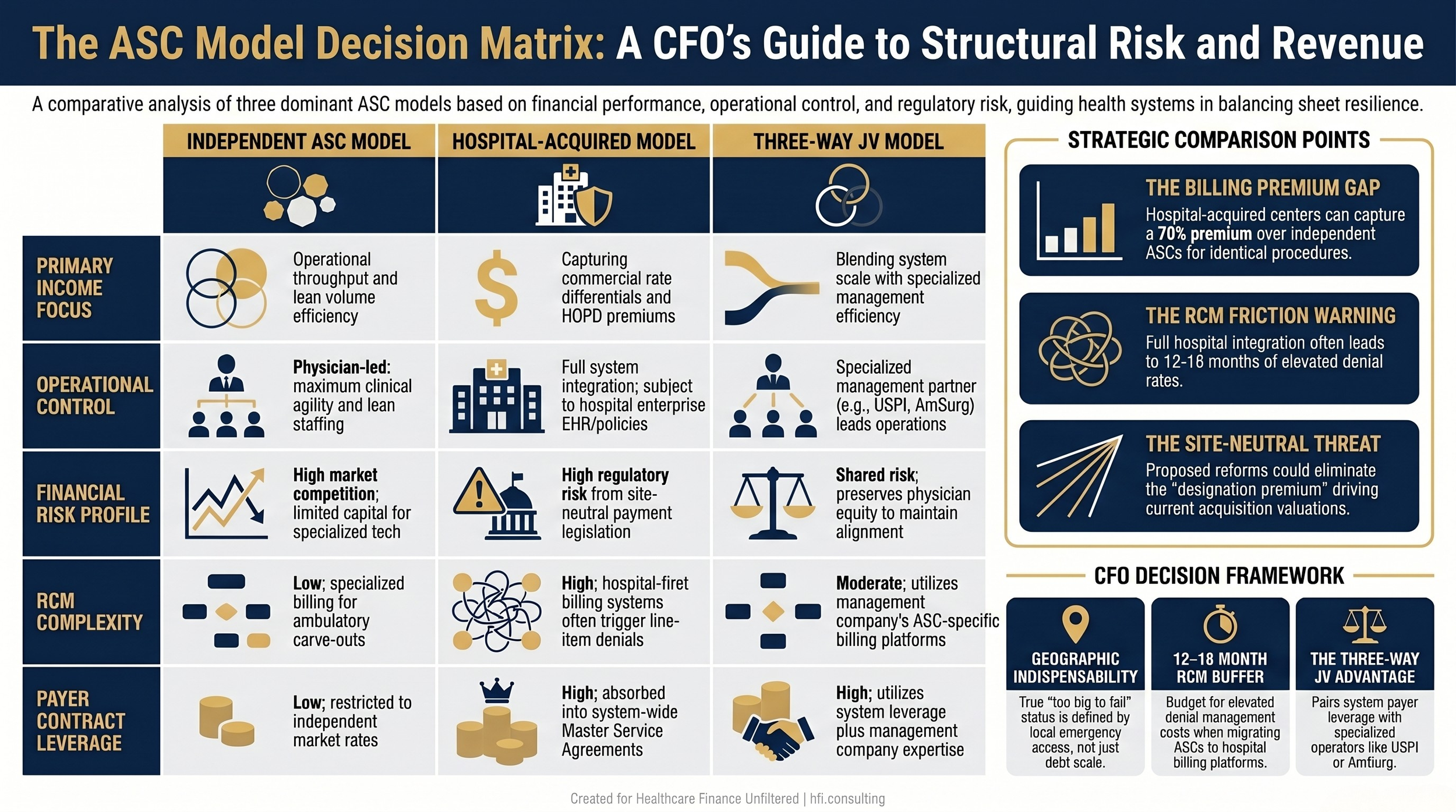

ASC billing is a fundamentally different discipline from hospital billing. ASC claims operate on lean cash flow timelines, carrier-specific coding interpretations, and complex implant carve-outs that hospital-first RCM platforms were not built to handle. When a health system forces a newly acquired ASC through its enterprise EHR and billing infrastructure, denial rates frequently spike in the first 12 to 18 months. What looks like a clean claim to a hospital coder often triggers a line-item denial from payers running ASC-specific edits.

I saw versions of this dynamic during Ascension's multi-hospital integration work across seven facilities. RCM standardization timelines almost always underestimate the complexity of merging specialized billing operations into a centralized platform. An ASC acquisition compounds that complexity because you are not merging two hospital environments. You are merging two fundamentally different reimbursement worlds.

The systems that execute this well are moving toward three-way joint ventures rather than outright acquisitions. The model pairs the health system's payer leverage and capital base with a specialized ASC management company (USPI, AmSurg, Surgical Partners) that maintains the lean operational discipline the ambulatory setting requires. The physicians retain equity, which preserves throughput incentives. This structure is becoming the market standard precisely because it acknowledges that hospital-scale management and ASC-scale efficiency do not naturally coexist.

Three-column comparison table showing financial and operational differences between independent ASC, hospital-acquired ASC, and three-way joint venture structures.

What This Means for Your Balance Sheet Right Now

The implications run differently depending on which side of the transaction you sit on.

If you are a provider CFO at a system executing this strategy: Your near-term capital allocation is shifting from inpatient capacity investment to ambulatory access point acquisition. The GPO advantages are real. You will reduce cost per case on orthopedic implants and specialized surgical supply the moment the ASC is absorbed into your group purchasing contracts. But your RCM team needs ASC-specific expertise, and the transition timeline for payer contract conversion will not match your pro forma assumptions. Budget for 12 to 18 months of elevated denial management costs.

If you are a provider CFO at a system not executing this strategy: You are watching payer-preferred procedure volume migrate to facilities where you do not have a stake. Your orthopedic and spine service line contribution margins are at risk not from your own operational performance but from referral pattern shifts. The RAND Corporation data on physician employment is clear: employed physicians align their referrals to system-owned facilities. If the acquiring system employs the surgeons, the cases follow.

If you are a payer CFO: You are facing a direct premium increase on the exact procedures you had been routing to independent ASCs to manage unit cost. The shift from independent to hospital-backed ASC billing is not neutral. It triggers a contract renegotiation dynamic where the system's leverage has just expanded.

This is one of the clearest real-world illustrations of a dynamic I covered in detail in my earlier analysis of the ambulatory growth paradox.

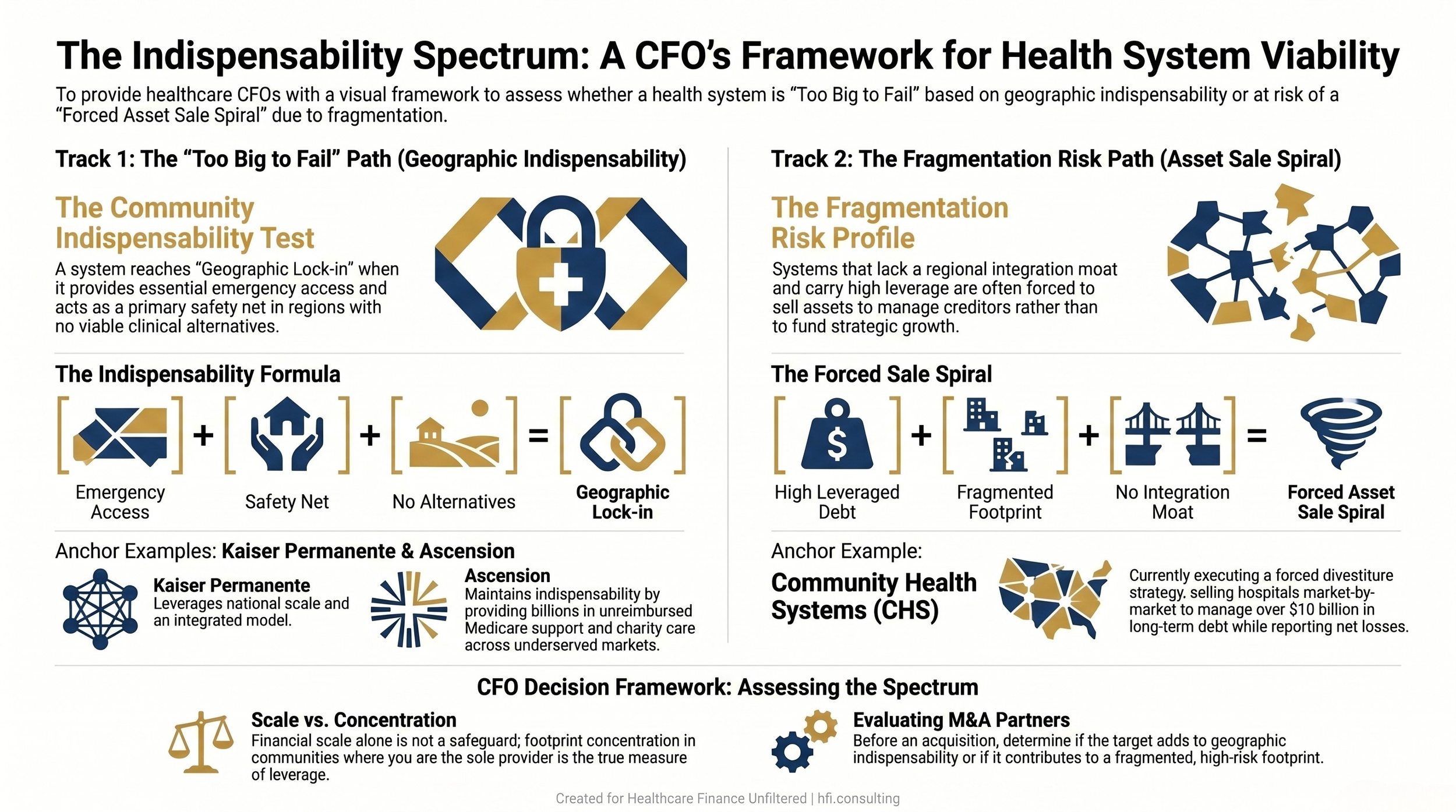

Are These Systems "Too Big to Fail"?

The question deserves a more precise answer than "yes" or "no."

Kaiser Permanente reported $34.6 billion in quarterly operating revenues in Q1 2026, with a net income of $2 billion and an investment portfolio generating $1.3 billion in that quarter alone. Kaiser is not acquiring ASCs as a survival strategy. It is building an integrated system at national scale through its Risant Health subsidiary, acquiring regional systems like Geisinger and Cone Health to export its value-based model. Kaiser is not at risk of failing. It is expanding to the point where entire regional economies depend on its operation.

Ascension represents a different dynamic entirely. In the nine months ending March 2026, Ascension provided $2.1 billion in community benefits and charity care, including $883 million for people living in poverty and $1.3 billion in unreimbursed Medicare support. If Ascension's hospital footprint were to dissolve in underserved markets, the public safety net would collapse in dozens of metropolitan and rural communities. That is not financial leverage in a banking sense. It is geographic indispensability.

Community Health Systems is the counterexample. With $10.15 billion in long-term debt and a $58 million net loss in Q1 2026, CHS is executing a forced divestiture strategy to manage creditors. It is not too big to fail. It is failing hospital by hospital, market by market, selling individual assets to stay afloat. That is a fundamentally different risk profile than Kaiser or Ascension.

The CFO takeaway is that "too big to fail" in healthcare is a geographic and clinical concept, not a financial one. A system becomes indispensable when its closure would vaporize local emergency access and safety-net capacity. Financial scale alone is not the determining factor. Footprint concentration in communities with no alternatives is.

For a deeper look at M&A integration risk across different system profiles, see my earlier analysis of what 41 hospital sales teach finance leaders about transition complexity.

Dual-track flow diagram showing "too big to fail" community indispensability criteria versus fragmentation risk spiral, with Kaiser, Ascension, and CHS as reference examples.

Washington Is Not Waiting: The Site-Neutral Payment Battle

The policy response to this consolidation wave is already in motion. This is not a future risk. It is an active legislative and regulatory fight with direct implications for your FY27 and FY28 budget assumptions.

The core issue is facility fees. Medicare currently pays a significant premium for procedures performed in hospital outpatient departments compared to identical procedures in independent settings. That premium is the financial engine driving the acquisition playbook. When a health system converts an independent ASC to a hospital outpatient department designation, Medicare reimbursement rises by 60 percent or more for the same clinical service.

Site-neutral payment reform would eliminate that designation premium entirely. CMS and lawmakers are pushing to set a single flat reimbursement for a clinical service regardless of whether it is performed in a physician's office, an independent ASC, or a hospital-owned facility. The goal is explicit: remove the financial incentive for hospitals to acquire independent practices and ASCs purely for billing conversion purposes.

The American Hospital Association is fighting this aggressively, and their argument is not without merit. Hospitals operate 24/7 emergency departments, maintain disaster standby capacity, and absorb disproportionate uninsured patient volume. The margins captured from outpatient surgical procedures are not excess profit for most systems. They are the internal subsidy that keeps the ED and the rural clinic from shutting down.

That tension is real. But it does not change the policy trajectory. If site-neutral payments are fully implemented, the financial logic that makes the hospital-to-ASC conversion attractive almost disappears. The acquisition premium collapses. The three-way JV structure becomes the only model that preserves enough operational efficiency and physician alignment to generate a return.

CFOs who are not yet running site-neutral payment scenarios in their five-year models are behind the curve. The Florida outpatient acquisition landscape I analyzed earlier this year highlighted exactly this dynamic in a state market context.

The Framework Every CFO Needs Before Their Next Board Presentation

This is not a passive trend to monitor. It is an active capital allocation decision that belongs in your strategic planning cycle now.

Before your next board presentation on ambulatory strategy, run three scenarios through your finance model.

Scenario One: Site-neutral payments pass at 80 percent of the current proposed scope. Model the revenue impact on your HOPD designation conversions. Recalculate the pro forma on any pending ASC acquisition that assumed HOPD billing conversion. If the deal does not pencil under this scenario, you do not have a deal. You have a liability.

Scenario Two: A dominant regional competitor completes a three-way JV with a national ASC operator in your primary service area. Map the physician employment relationships in your orthopedic and spine service lines. Identify which surgeons have system loyalty and which have independent or JV-adjacent incentives. Model the case volume loss if 20 percent of your ASC-eligible cases shift to a competitor's newly acquired center.

Scenario Three: Your system is the acquirer. Identify the specialized ASC RCM talent you do not currently have. Budget realistically for the denial management spike in months 6 through 18 post-acquisition. Evaluate whether a management company partnership preserves operational efficiency better than full integration into your hospital billing infrastructure.

The implant cost dimension deserves separate attention in every scenario. ASC orthopedic and spine cases carry implant costs that behave very differently under independent GPO contracts versus system purchasing agreements. I have written specifically about the revenue gaps that accumulate when implant billing disciplines from ASC settings are not carried forward cleanly into a hospital RCM environment.

Healthcare Finance Unfiltered goes deeper on M&A integration, capital reallocation strategy, and the policy shifts reshaping your balance sheet. If you are not already a subscriber, join the finance leaders who get the analysis before it lands in the trade press.

Subscribe to Healthcare Finance Unfiltered

What This Looks Like in 18 Months

The velocity of this consolidation suggests a near-term market structure that most strategic plans do not account for.

By the end of 2027, the ambulatory surgery landscape in most major metro markets will be dominated by three types of entities: health system-owned centers operating under master service agreements, three-way JV structures that blend system leverage with specialized management, and a shrinking pool of independent single-specialty centers serving the niches that large systems have not yet prioritized. The independent ASC that is not embedded in some form of system alignment is increasingly structurally disadvantaged in payer contracting, implant purchasing, and clinical staffing.

For payer CFOs, that concentration means your preferred independent ASC network is getting acquired out from under your cost management strategy. The unit cost you built into your actuarial models for outpatient orthopedics will not hold as the facilities convert to system billing.

For provider CFOs, the window to establish ambulatory presence in your primary markets through JV structures is narrowing as competitors move first. The first mover in each market captures the physician alignment and the payer contract advantage. The second mover pays acquisition premiums on a smaller pool of remaining independent targets.

Neither position is comfortable. But only one of them is recoverable with deliberate strategy.

The Bottom Line for Finance Leaders

The hospital sell-off is not a strategic pivot story. It is a capital structure story. Health systems are trading lower-return inpatient assets for higher-margin ambulatory access points, capturing commercial payer premiums at the point of acquisition, and using GPO scale to reduce per-case costs. The logic works until site-neutral payment reform removes the billing premium that makes the conversion economics attractive.

The CFOs who will navigate this well are already running both scenarios simultaneously. Not because the policy outcome is certain, but because the business case for your current ambulatory strategy has to survive either outcome to be a real strategy at all.

If your system is evaluating an ASC acquisition, a joint venture structure, or a service line rationalization that involves ambulatory reallocation, I work with finance teams on the pro forma assumptions, RCM readiness assessment, and scenario modeling that belongs in the pre-decision analysis. Reach out throughhfi.consulting to start the conversation.

P.S. The site-neutral payment debate tends to get framed as a policy fight between hospitals and CMS. But the more interesting CFO question is this: if the billing premium disappears, which ASC acquisition deals in your pipeline still pencil out on operational merit alone? Hit reply and tell me where your team is on that scenario.