The $37,824 Breaking Point: What Business Owners, Health System CFOs, and Payer Leaders Need to Know About 2026 Health Cost Inflation

Employer health costs jumped 7.9% this year. ICHRA is changing the game for small businesses. Here is what every stakeholder needs to model before renewal season.

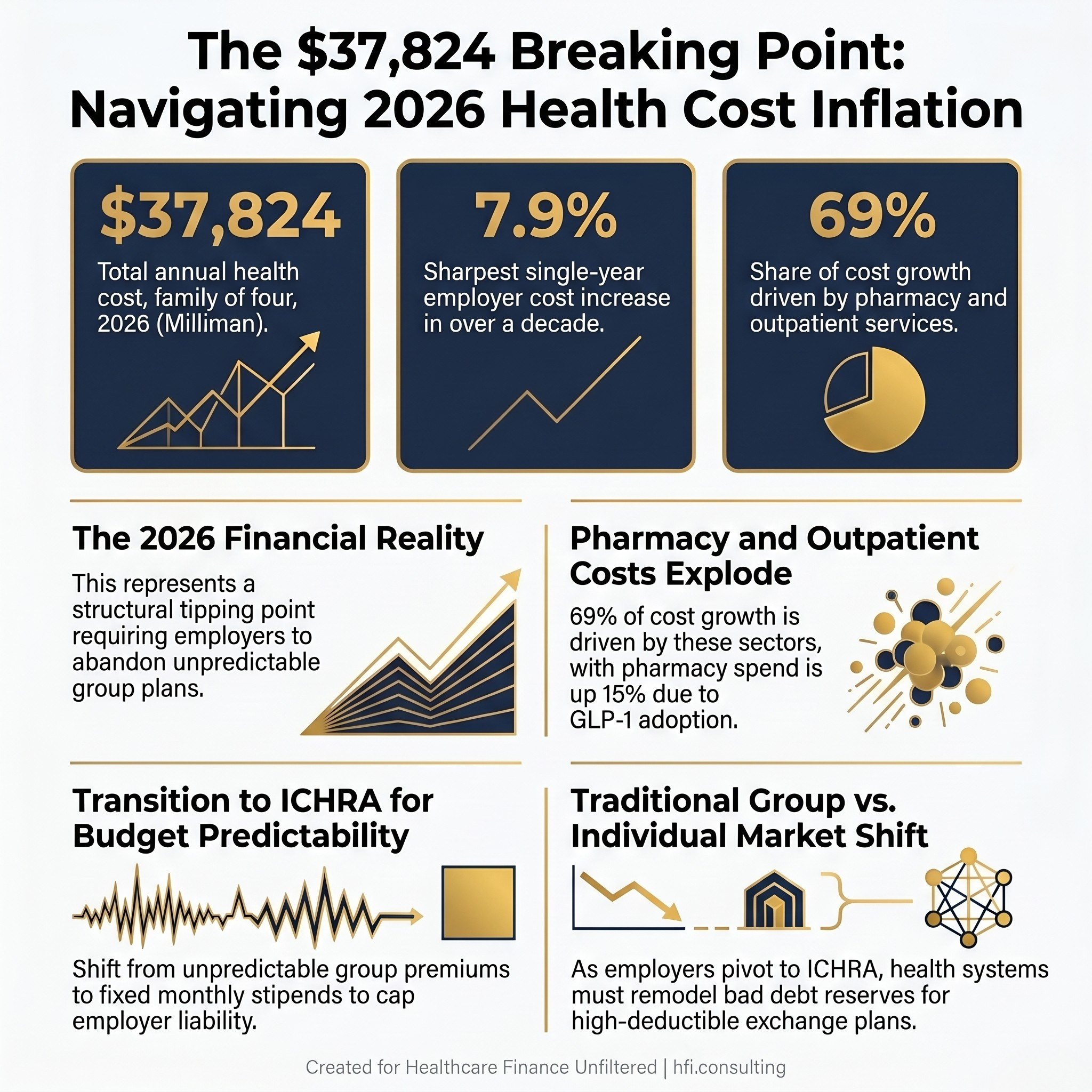

The Milliman 2026 Medical Index landed on May 20 with a number that should matter to anyone who signs payroll, manages a hospital revenue cycle, or prices health plan products: 7.9%. That is the sharpest single-year increase in employer health costs in more than a decade. A family of four on a typical employer plan now commands $37,824 in total annual costs. That figure is not an abstraction. It is a forcing function reshaping how employers buy coverage, how employees access care, and how health systems and payers model their financial assumptions. The decisions being made at employer renewal tables right now will show up in CFO variance reports and payer trend data twelve months from today.

Three-panel stat card showing 2026 Milliman employer health cost benchmarks: $37,824 family cost, 7.9% annual increase, 69% driven by pharmacy and outpatient.

The Cost Drivers Every Employer Needs to Understand

The Milliman data captures both employer and employee cost share. What it really reveals is a system where the employer is absorbing a shrinking slice of a rapidly expanding bill. The employer share of healthcare costs has declined from 61% to 58% since 2005, while the employee share of premiums has climbed from 21% to 27% over the same period.

Pharmacy is the fastest-rising cost category, up nearly 15% per person. GLP-1 medications for diabetes and weight management are playing an increasingly significant role in employer drug spend. Outpatient care now accounts for about 31% of total employer-sponsored spending and has grown more than 300% in cost for a family of four over the past two decades.

When employees absorb more, two things happen predictably. They defer care. And they look for alternatives. Both behaviors have financial consequences that ripple far beyond the employer's HR budget.

The ICHRA Mechanism: From Group Plan to Individual Stipend

Employers at every size are responding. A growing number are exiting the defined-benefit group plan model entirely and moving toward Individual Coverage Health Reimbursement Arrangements. ICHRA is not a fringe strategy. It is a structural response to budget unpredictability that has been accelerating since 2020 and reached a tipping point with this year's renewal cycle.

Under ICHRA, an employer sets a fixed monthly contribution, anywhere from a few hundred dollars to over a thousand per employee. Employees take that amount and purchase their own coverage on the individual market. For employees who qualify, the contribution can be applied toward Medicare or Medicare Advantage plans. The employer's liability is capped. The employee makes their own coverage decisions and owns their plan regardless of job change.

For a mid-sized employer facing a pharmacy spike tied to GLP-1 adoption across 10% of the workforce, that exposure can exceed $700,000 in unbudgeted annual spend. ICHRA eliminates that variability at the plan level by converting an unpredictable group expense into a fixed per-employee contribution the employer can index to inflation or wage growth.

Side-by-side comparison of traditional group health plan versus ICHRA model showing employer cost exposure, employee cost-sharing, and budget predictability differences.

If You Are a Business Owner: What to Actually Do at Renewal

This section is for business owners and HR decision-makers at small and mid-sized companies. If you are a hospital CFO or payer executive, the next two sections are written for you.

The group health insurance model was built for a world where premiums were manageable, employees stayed long enough to justify the investment, and the administrative burden was worth the predictability. That world is functionally over for most employers under 200 covered lives.

If you are staring at a renewal quote that is 10%, 12%, or 15% higher than last year, here is what you need to know before you sign.

The ICHRA math is worth running. Take your current total premium spend, including both employer and employee contributions. Divide it by your number of covered employees. Compare that per-employee cost to what you would spend at a competitive ICHRA contribution level, typically $400 to $800 per month per employee for individual coverage, more for employees with families. In most markets, especially for healthier workforces, ICHRA contributions come out lower while still giving employees real buying power on the exchange.

The key variable is your workforce demographics. Older employees and families will need a higher contribution to access comparable coverage on the individual market. Younger, single employees often land on plans that are dramatically cheaper than what they had on the group plan. ICHRA allows you to set different contribution amounts by employee class, so you are not required to treat every employee identically.

DPC plus catastrophic coverage is a real strategy for some workforces. A Direct Primary Care membership typically costs $70 to $120 per employee per month. For that flat fee, employees get unlimited primary care visits, same-day or next-day access, and in many practices, direct physician cell access. Combine that with a high-deductible catastrophic plan to cover hospitalizations and serious illness, and total cost for a healthy single employee can run well under $300 per month versus $600 or more on a traditional group plan.

This model works best for workforces that are younger, generally healthy, and where primary care access is the main day-to-day need. It is not appropriate for employees managing complex chronic conditions who regularly hit specialists and imaging. But for a contractor workforce, a small professional services firm, or a retail business with younger staff, the DPC-plus-catastrophic combination deserves a serious look.

Functional medicine is worth understanding, not necessarily endorsing. Some employees with high-deductible plans will seek out functional medicine or DPC practices specifically because the math works better for them than meeting a large deductible through conventional care. This is a workforce wellness signal worth tracking. If your employees are self-directing toward alternative care models, your traditional EAP and wellness benefit may not be reaching them. Knowing where your workforce is actually getting care helps you design benefits that land.

Five questions to ask your broker before renewal:

First: What is the ICHRA contribution level that would give my employees comparable buying power to what they have today, and what does that number look like relative to my current total premium spend?

Second: What individual market plans are available in my employees' ZIP codes at the contribution level I am considering, and what are the deductibles on those plans?

Third: Are any Direct Primary Care practices in my market willing to contract with me for a group membership rate, and how does that change my total benefits math?

Fourth: If I shift to ICHRA, how does that affect my older employees and anyone currently managing a chronic condition? What contribution level do I need to set to avoid leaving them underinsured?

Fifth: What are my competitors in my industry and geography doing at renewal this year? Am I about to be at a recruiting disadvantage or a cost advantage?

If your broker cannot answer these questions fluently, you may be working with someone who is not current on the market.

If you are a business owner heading into renewal and want a side-by-side cost comparison template for group plan versus ICHRA, reply to this email and I will send it directly. And if you are a CFO at a health system or payer, I want to hear what you are seeing in your commercial payer mix. Hit reply and tell me what your bad debt reserve methodology currently looks like for high-deductible commercial patients.

For Health System and Payer CFOs: The Revenue Cycle Consequences

When employers shift to ICHRA and employees land on individual exchange plans, your patient population changes in ways that do not show up cleanly in payer category reports.

Individual market plans, particularly at lower premium tiers, carry significantly higher deductibles than comparable group coverage. A patient who was previously covered by a mid-market group plan with a $2,000 family deductible may now be carrying $6,000 or $7,000 on an exchange plan purchased with an ICHRA stipend that did not fully close the premium gap.

That patient is functionally self-pay for primary and routine care. They defer imaging, skip specialist referrals, and delay elective procedures. When they do present, they arrive with higher acuity and less financial capacity to absorb out-of-pocket costs.

From my work supporting financial operations across seven hospitals at Ascension, one of the clearest early warning signals of payer mix deterioration was never the payer category itself. It was the deductible exposure embedded in the plans underneath the category. A patient listed as "commercial" on your revenue cycle dashboard may represent the same bad debt risk as a self-pay patient once deductible structure is accounted for.

Your bad debt reserve methodology needs a line of sight into individual market plan penetration in your service area. If ICHRA adoption is growing in your employer base, your commercial category is not stable. It is stratifying.

The Parallel Pipeline: Functional Medicine and Direct Primary Care

There is a second structural shift running alongside the ICHRA transition. The growth of functional medicine and direct primary care is not just a consumer wellness story. It is a referral pipeline question.

The Institute for Functional Medicine trained 13,129 unique practitioners in 2025 alone, bringing their total trained workforce since 1991 to more than 103,800 practitioners. That is a credentialed practitioner base operating largely outside the traditional insurance reimbursement model. DPC practices offer unlimited primary care for flat monthly fees without insurance billing.

When a patient with a high-deductible ICHRA plan calculates that a $100 per month DPC membership plus cash-pay lab rates is cheaper than meeting a $6,000 deductible, the math works for them. It also works for the DPC provider who exits the insurance billing loop entirely.

For hospital-based and health system-affiliated primary care networks, that math represents a referral chain that never starts. Primary care physicians within your system are the entry point for downstream specialty care, imaging, and procedural volume. If patients with high-deductible plans are routing their primary care to DPC practices outside your network, your specialty volume assumption is built on a foundation that is eroding.

Functional medicine attracts a specific demographic: commercially insured, higher income, proactive about chronic disease management. That is also the demographic that anchors profitable outpatient volume. You do not need to validate functional medicine's clinical claims to recognize that its growth changes where high-value patients go first.

From the payer side at Florida Blue Medicare, benefit structure shifts in employer groups were a leading indicator of individual market enrollment changes before they ever appeared in claims data. The same predictive logic applies on the provider side. ICHRA adoption in your employer base today is a signal about your commercial mix composition twelve to twenty-four months from now.

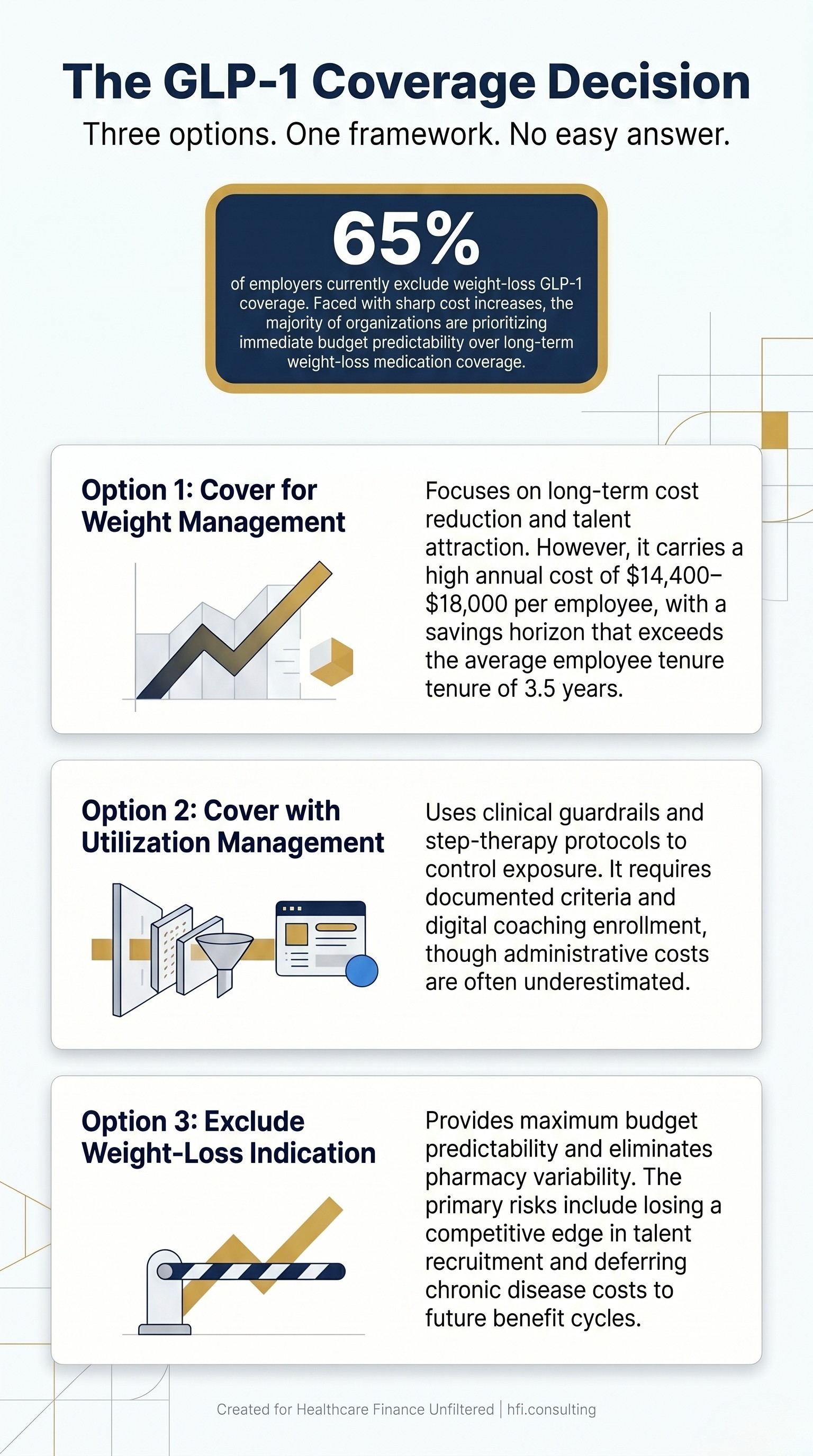

The GLP-1 Budget Problem Is Shared

This problem does not belong exclusively to employers. If your health system sponsors a self-funded plan for employees, the 15% pharmacy cost increase in Milliman's data is hitting your own benefit budget. A system with 5,000 covered employees facing 10% enrollment in GLP-1 weight management programs is carrying more than $7 million in unbudgeted annual pharmacy spend.

The clinical case for coverage is real. Weight loss reduces downstream costs for diabetes, cardiovascular disease, joint replacement, and sleep apnea. But the financial math is disconnected from the benefit horizon. The average employee tenure runs 3.5 to 4.1 years. The long-term savings from GLP-1 use play out over a decade. You pay for a benefit whose financial return will largely accrue to future employers.

This is why 65% of employers are currently excluding weight-loss indications from their GLP-1 formularies. The ones who do cover require documented clinical criteria, step-therapy protocols, and enrollment in digital coaching. Those are defensible budget controls that need to be factored into total benefit spend, not just pharmacy line items.

Three-column decision matrix for employers and health system CFOs evaluating GLP-1 weight management medication coverage options including cost, ROI, and utilization management trade-offs

The Scenario Framework: What to Model Now

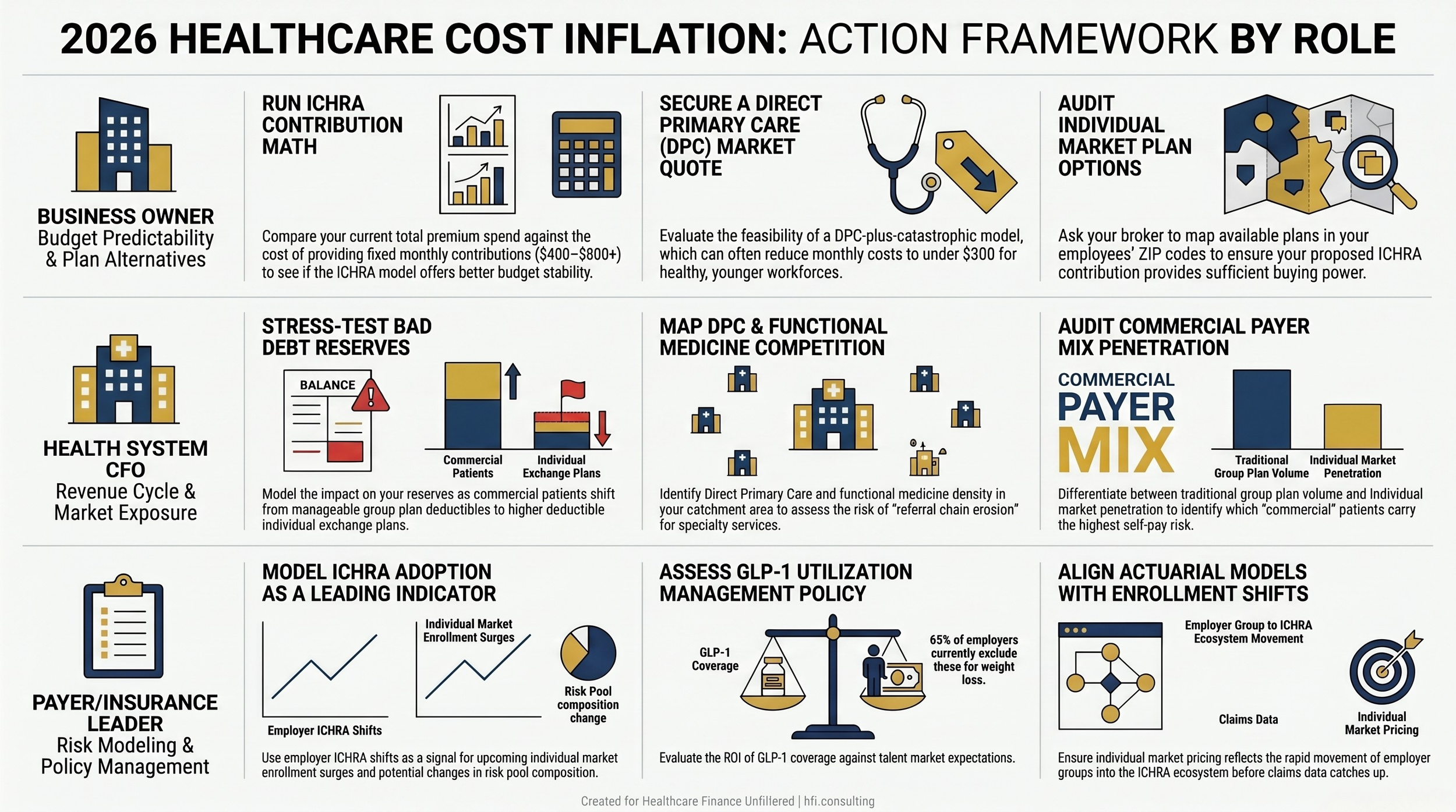

The 2026 Milliman data gives you a benchmark. What you do with it depends on which seat you are sitting in.

For business owners at renewal: Run the ICHRA contribution math against your current premium spend. Get a DPC quote in your market. Ask your broker for individual market plan options at your proposed contribution level before you decide, not after you sign.

For health system CFOs: Model what happens to your bad debt reserve if 15% of current commercial volume shifts from group plan deductibles to individual market deductibles over the next 24 months. Map DPC and functional medicine practice density in your primary care catchment area. Identify which employer groups are prime ICHRA candidates based on size and industry.

For payer leaders: Benefit structure shifts in employer groups are a leading indicator of individual market enrollment surges. If ICHRA adoption in your geographic markets is accelerating, your risk pool composition is changing before your actuarial models reflect it.

None of these analyses are simple. They require pulling data across your revenue cycle, your local employer market, and your own benefit plan claims. But the alternative is explaining gaps in a variance analysis six months into the fiscal year when the data to anticipate them was available today.

Three-track action framework showing 2026 health cost inflation response steps for business owners, health system CFOs, and payer leaders.

The Bottom Line

The 7.9% increase in employer health costs is not one organization's problem to solve. It lands on the business owner renewing a group plan, the health system CFO watching commercial patient acuity climb, and the payer modeling individual market enrollment shifts. The mechanisms are different. The pressure is the same.

ICHRA adoption is accelerating because the group plan model is financially unsustainable for many employers. DPC and functional medicine are growing because patients with high-deductible plans are running their own math. Both trends redirect patients, dollars, and risk in ways that will show up in financial statements before they show up in strategic plans.

The organizations that model these shifts now have time to adjust assumptions and make decisions. The ones that wait will be explaining gaps they had the data to see.

Healthcare Finance Unfiltered covers the decisions that actually move the needle, whether you run a business, a hospital system, or a payer operation. If you are not already a subscriber, join the finance and operations leaders reading every issue at hfi.consulting.

P.S. Two questions I genuinely want your answer to. If you are a business owner: what is your broker telling you about ICHRA this renewal season? If you are a health system or payer CFO: have you started modeling high-deductible commercial exposure in your bad debt reserve? Hit reply. Both answers will shape the follow-up piece.