Productivity Reporting and Labor Benchmarks: The CFO's Missing Budget-Season Toolkit

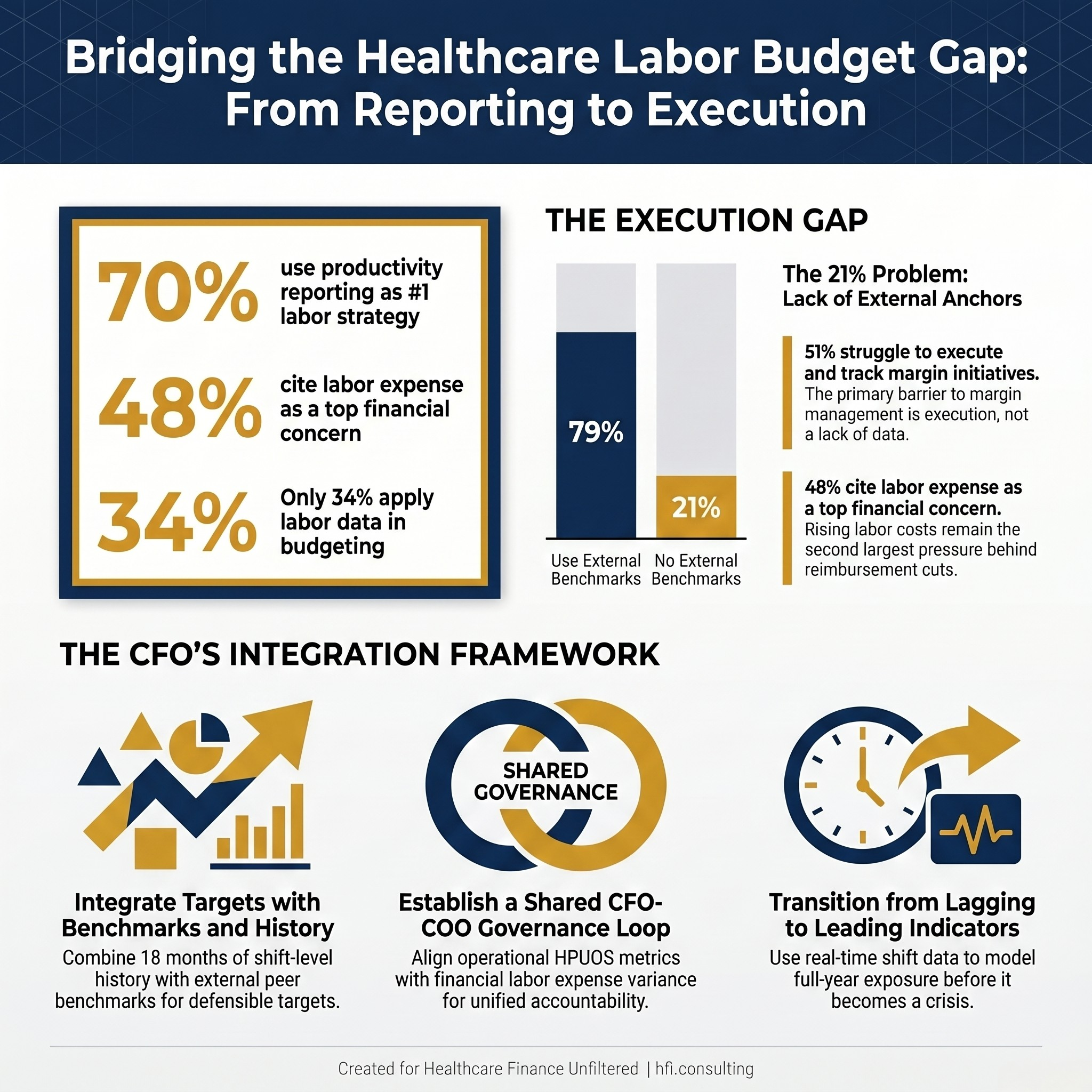

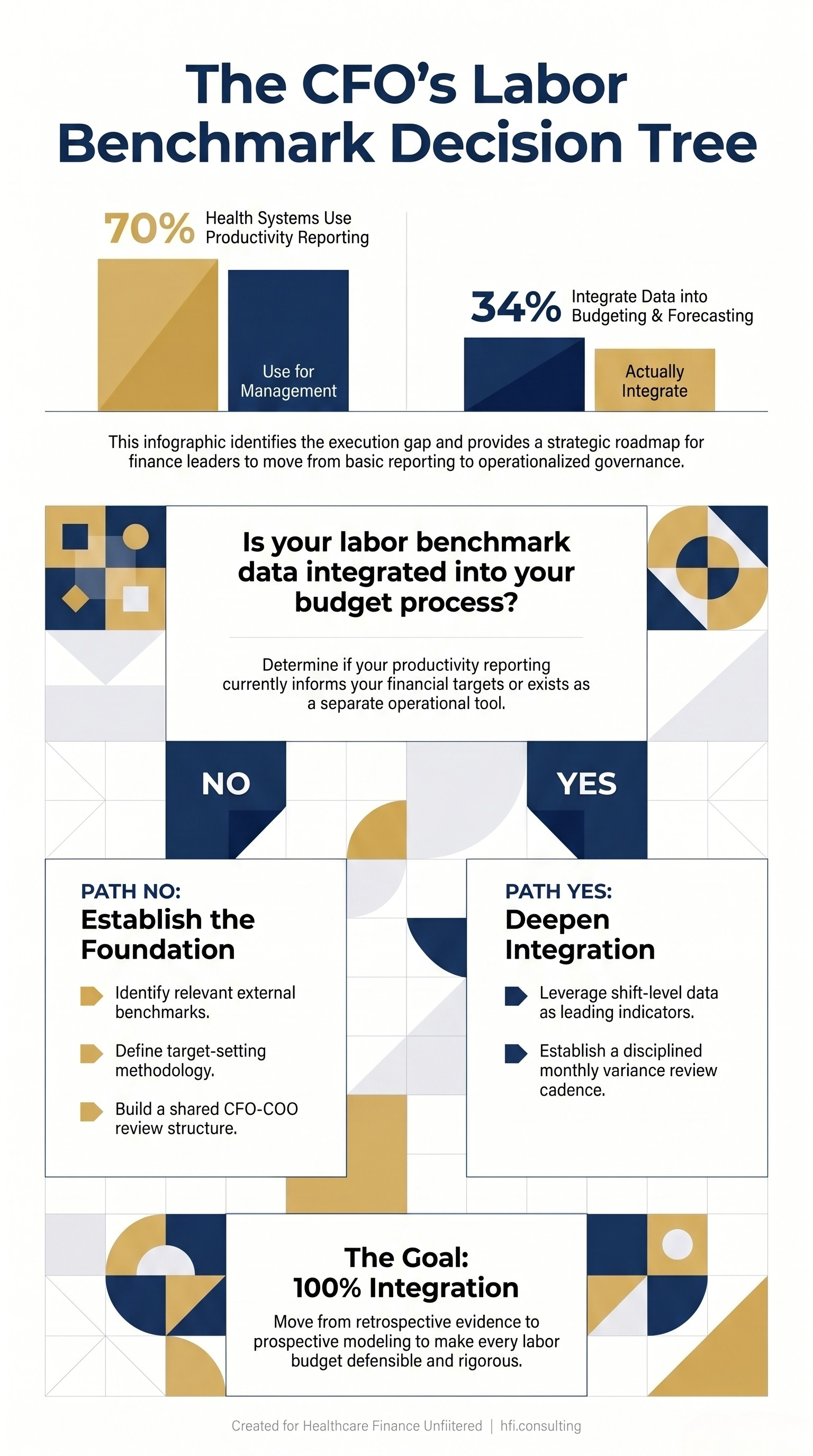

New Strata data shows 70% of health systems use productivity reporting — but most CFOs aren't leveraging it at budget time.

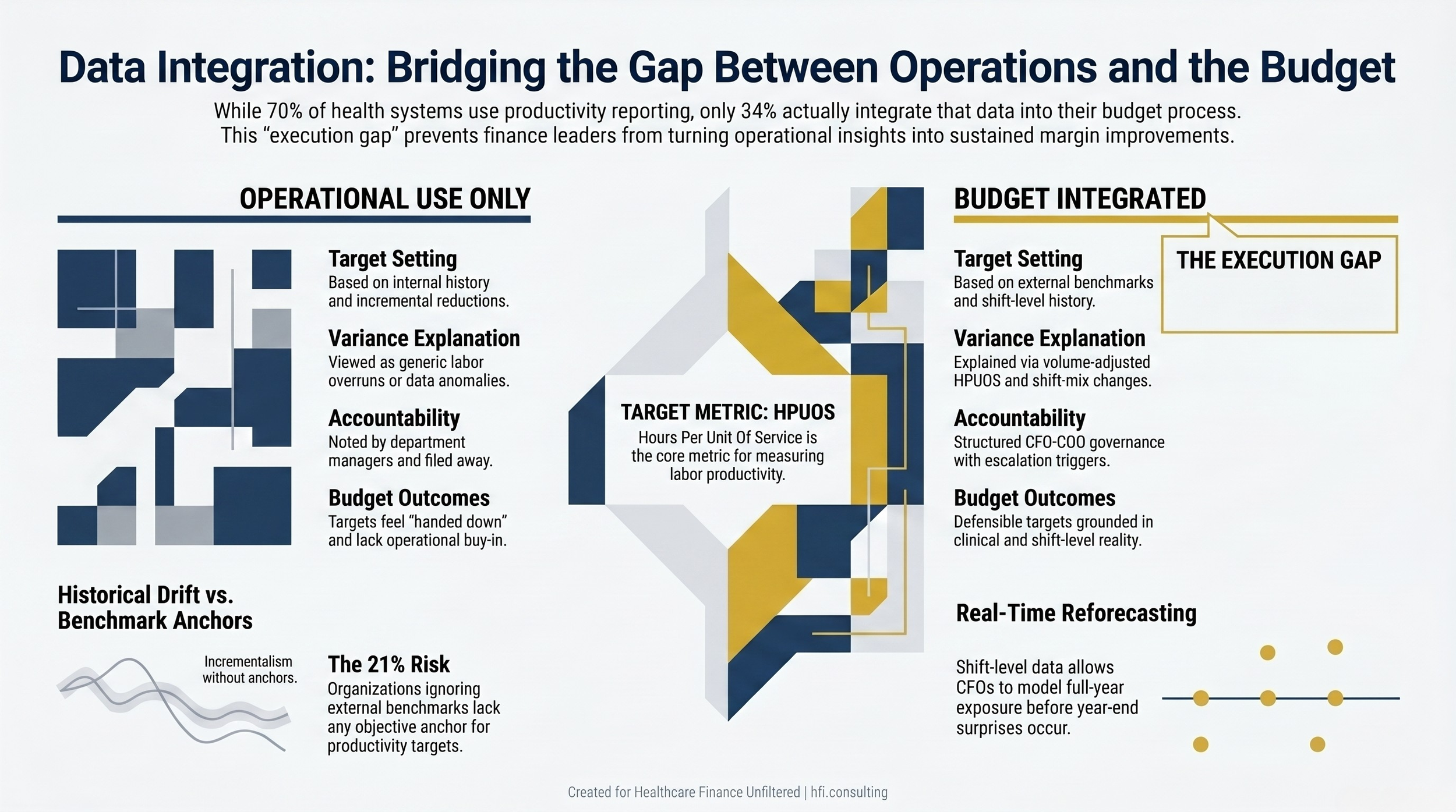

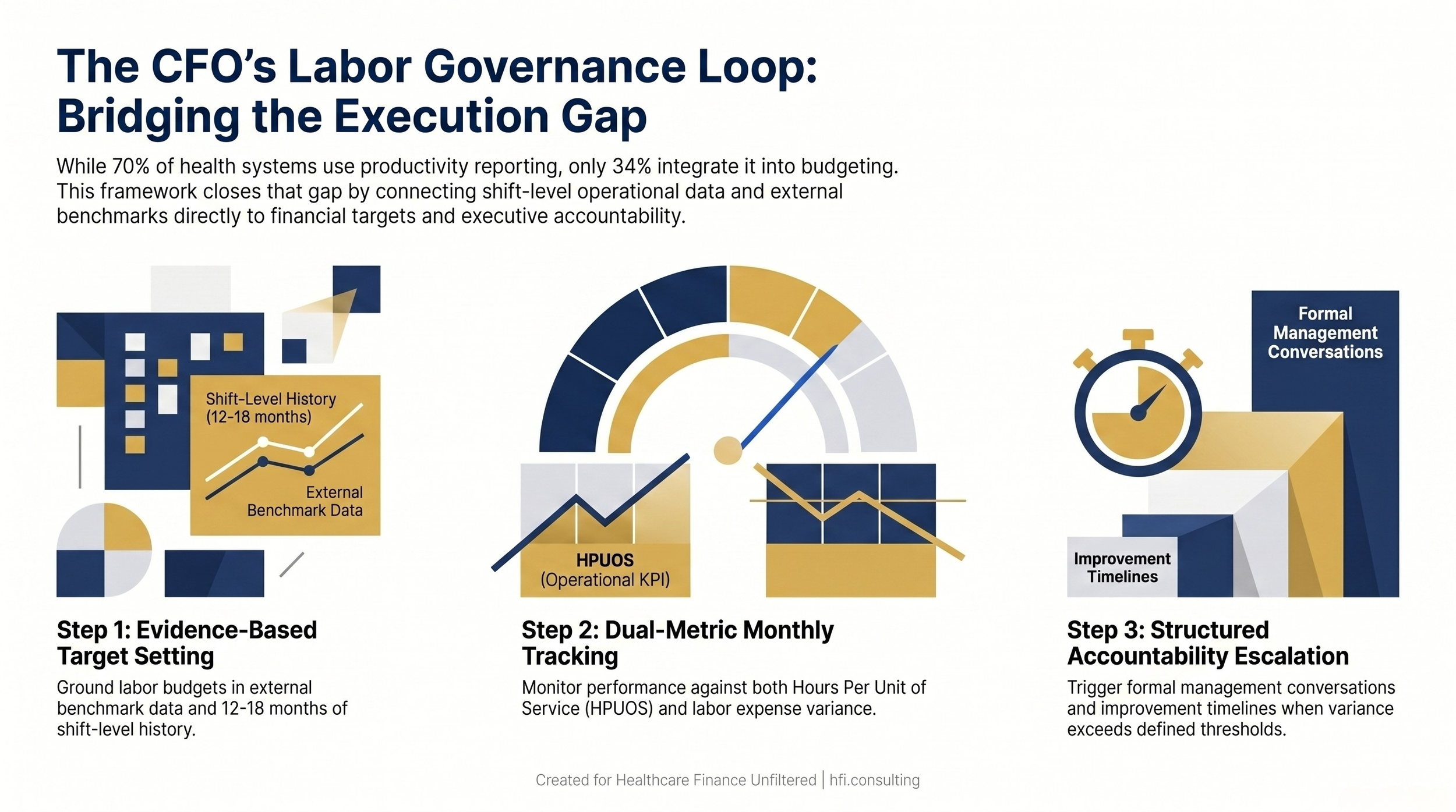

Strata Decision Technology's 2026 Healthcare Financial Outlook Report dropped this week, and one finding deserves more attention than the headline numbers: 70% of finance leaders now cite productivity reporting as their top strategy for controlling labor costs, but only 34% are using it in their actual budget and forecasting process. That gap is not a data problem. It is an execution problem, and it is costing health systems real margin.

Three Strata 2026 survey statistics on healthcare labor productivity reporting and budget integration gaps

The Data Gap Nobody Is Talking About

The Strata report surveyed finance leaders across health systems, medical groups, and single hospitals. Respondents named government funding and Medicaid cuts as their leading concern at 66%, followed by labor expense at 48%. Those two pressures are related. When reimbursement shrinks, the first conversation in the boardroom is always about the labor line.

What stands out in this year's data is how clearly finance leaders have diagnosed the problem while struggling to close the execution loop. Fifty-seven percent said reducing costs is their top priority for 2026. Forty-three percent named productivity management as a core organizational focus. And 51% admitted that executing and tracking margin initiatives is still their biggest challenge in actually managing margins.

That last number is the one worth sitting with. It is not that health systems lack strategies. It is that the strategies are not translating into sustained operational change.

What Finance Leaders Are Actually Using

The survey asked respondents which strategies they are prioritizing to drive better labor expense outcomes. Productivity reporting ranked first at 70%. Effective use of labor benchmarks ranked second at 64%. Real-time, shift-level analysis came in third at 54%.

Those three tools are often thought of as COO tools. And in daily operations, they are. A nursing director reviewing shift-level hours per unit of service, a department manager getting a weekly benchmark comparison against peer institutions — that is operational territory.

But here is where the CFO perspective changes the frame: these tools do not only measure past performance. When built into the right structure, they become the forward-looking inputs that make a labor budget defensible.

In my work at Ascension across seven hospitals, one of the most consistent problems at budget time was that labor targets felt like numbers handed down from above rather than targets grounded in operational reality. Directors would push back because they could not see how the numbers were built. When you start from benchmark data and shift-level historical productivity, the conversation changes. You are not arguing about a percentage reduction. You are reviewing whether the target HPUOS is aligned with the external benchmark and whether the prior year's performance supports achieving it.

That is a fundamentally different budget process.

What Real-Time Shift-Level Data Actually Gives You

For the COO, shift-level productivity data is about making adjustments in real time. Are nurses working above or below target HPUOS today? Is the ED volume spike being staffed appropriately without triggering unnecessary overtime? These are operational decisions happening at the shift level.

For the CFO, that same data becomes retrospective evidence and prospective modeling material. Here is what I mean:

At budget time, the CFO needs to answer a question that most finance teams struggle with: what is an achievable but rigorous labor budget for this department, given its patient mix, service intensity, and staffing model? The answer lives in the shift-level data from the prior 12 to 18 months.

If a medical-surgical unit has been running at 8.2 HPUOS over the past year while the external benchmark for similar organizations is 7.6, you have a specific, documented gap. You know it is not a data anomaly because you can see it at the shift level. You can also see whether the gap is consistent or concentrated in certain shifts, certain days of the week, or following certain clinical events. That context is what makes the budget number defensible.

Side-by-side comparison of operational-only versus budget-integrated use of healthcare productivity reporting data

Benchmarks as Change Management Infrastructure

The Strata data shows that 66% of organizations now use external benchmarks in productivity analysis. That is the highest adoption rate of any benchmark use case surveyed. But benchmark adoption and benchmark effectiveness are not the same thing.

Ninety percent of healthcare finance leaders in the survey said their organizations should be doing more to leverage financial and operational data to inform strategic decisions. That is a striking figure given how broadly benchmarks are now being used. It suggests that the problem is not access to comparative data. The problem is operationalizing it.

This is where the change management dimension of benchmarks matters, and it is something that does not get enough attention in finance circles.

A benchmark without a conversation is just a number on a report. When a CNO reviews a dashboard showing her unit is running 12% above external benchmark for HPUOS, one of two things happens: either that number triggers a structured accountability conversation with a clear improvement timeline, or it gets noted and filed away until next month's report.

The difference between those two outcomes is not a data problem. It is a governance problem. The CFO's role in that governance loop is to make sure the benchmark data is connected to the financial plan, not just the operational report. When benchmark gaps show up in the budget as explicit targets with variance expectations and accountability milestones, department leaders know that operational performance has financial consequences. The monthly review becomes a budget conversation, not just a productivity conversation.

I have seen this work and I have seen it fail. It fails when productivity reporting is owned entirely by the COO function with no connection to how the finance team builds targets or tracks variance. It works when the CFO and COO are using the same data set, speaking the same language about HPUOS targets, and presenting a unified accountability structure to department leaders.

The 21% Problem

One data point from the Strata report that should give finance leaders pause: 21% of respondents report that their organizations do not use external benchmarks in any planning processes.

That is a significant share of the industry operating without comparative context for any of their financial or operational decisions. For those organizations, the labor budget is built primarily from internal history. There is no external anchor. And without an external anchor, there is no way to know whether a productivity target is ambitious, achievable, or already being comfortably exceeded by peer institutions.

The risk is not just leaving margin on the table. It is that budget processes built entirely on internal history tend to drift toward incrementalism. Each year, the new target is a small percentage reduction from last year's actual. There is no structural mechanism to question whether the baseline itself is misaligned with external performance norms.

If your organization is in that 21%, the first step is not adopting a new platform. It is determining which external benchmark data sets are relevant to your clinical mix and service lines, and then building a structured process for how that data enters the budget conversation.

Finance-Operations Alignment: Still a Work in Progress

The survey also asked respondents how familiar their finance team is with the data and metrics used by the strategy team. The average was 64%. That moderate alignment score reflects something that many CFOs recognize from experience: finance and strategy often have visibility into the same general priorities but are not operating from the same data definitions.

This matters for labor management specifically because productivity benchmarks and service line financial targets often live in separate systems, reported through separate channels, owned by separate teams. When a service line review happens, the operational productivity data and the financial margin data may not even be reconciled to the same time period.

Three-step CFO governance loop connecting benchmark-based budget targets to monthly performance tracking and accountability escalation

What This Means for Your Budget Process

The Strata data points to a clear pattern: health systems have built significant capability in productivity reporting and benchmark access, but have not yet completed the integration work that would make those tools drive sustained margin improvement.

For CFOs preparing for the next budget cycle, there are three specific places where this integration pays off:

Target-setting: Use shift-level historical data and external benchmarks together to set department-level labor targets. A target built from both internal history and external context is harder to push back on and more likely to reflect actual operational potential.

Variance analysis: When budget variance is explained through the lens of productivity metrics — volume-adjusted HPUOS deviation, shift-mix changes, registry utilization above plan — the finance conversation becomes more specific and more actionable. Generic labor overruns are much harder to address than identified productivity gaps.

Mid-year reforecasting: Real-time shift-level data gives the CFO a leading indicator for labor expense trends, not just a lagging report. If a department's daily HPUOS starts trending above benchmark in the second quarter, the CFO and COO can model the full-year exposure before it becomes a year-end surprise.

Decision tree for healthcare CFOs assessing and improving labor benchmark integration into the hospital budget process

If your team is working through how to build these connections between productivity data and the budget process, or if you are trying to make the case internally for why the labor benchmark conversation needs to happen at the finance level and not just in operations, I would be glad to dig into the specifics with you. Reply to this email or reach out directly through hfi.consulting

The Bottom Line

The Strata 2026 Healthcare Financial Outlook Report confirms what most finance leaders already feel: the industry has more data than it is effectively using, and the gap between insight and execution is where margin improvement initiatives stall.

Productivity reporting and labor benchmarks are not new concepts. Health systems have been tracking HPUOS and comparing to national databases for years. What is newer — and what the data points to — is the expectation that these tools need to operate at the intersection of operations and finance, not just within one function.

The COO uses shift-level data to manage today's labor expense. The CFO uses that same data to build next year's budget, hold this year's performance to account, and identify where operational execution is trending before it becomes a financial problem.

That integration is not automatic. It requires a shared data framework, agreed-upon definitions of performance targets, and a governance structure that makes the finance team a participant in the productivity conversation, not just a recipient of the variance report.

The 70% of health systems using productivity reporting as their top labor strategy have the raw material. The question for 2026 is whether finance leaders build the governance structure that turns that raw material into sustained margin improvement.

The full Strata 2026 Healthcare Financial Outlook Report is available directly from Strata Decision Technology. If you are building out your benchmark integration framework or working through how to structure the CFO-COO accountability conversation around labor targets, more resources and frameworks are available at hfi.consulting

P.S. How is your organization currently using productivity benchmarks in the budget process — are they built into your targets from the start, or do they show up primarily in the variance conversation after the fact? Hit reply and let me know where you are in that integration.