Medtech M&A 2026: What Hospital CFOs and Supply Chain Directors Must Do Before the Contracts Change

Boston Scientific, Medtronic, and Stryker are reshaping your vendor landscape. Your GPO pricing may not survive the transition intact.

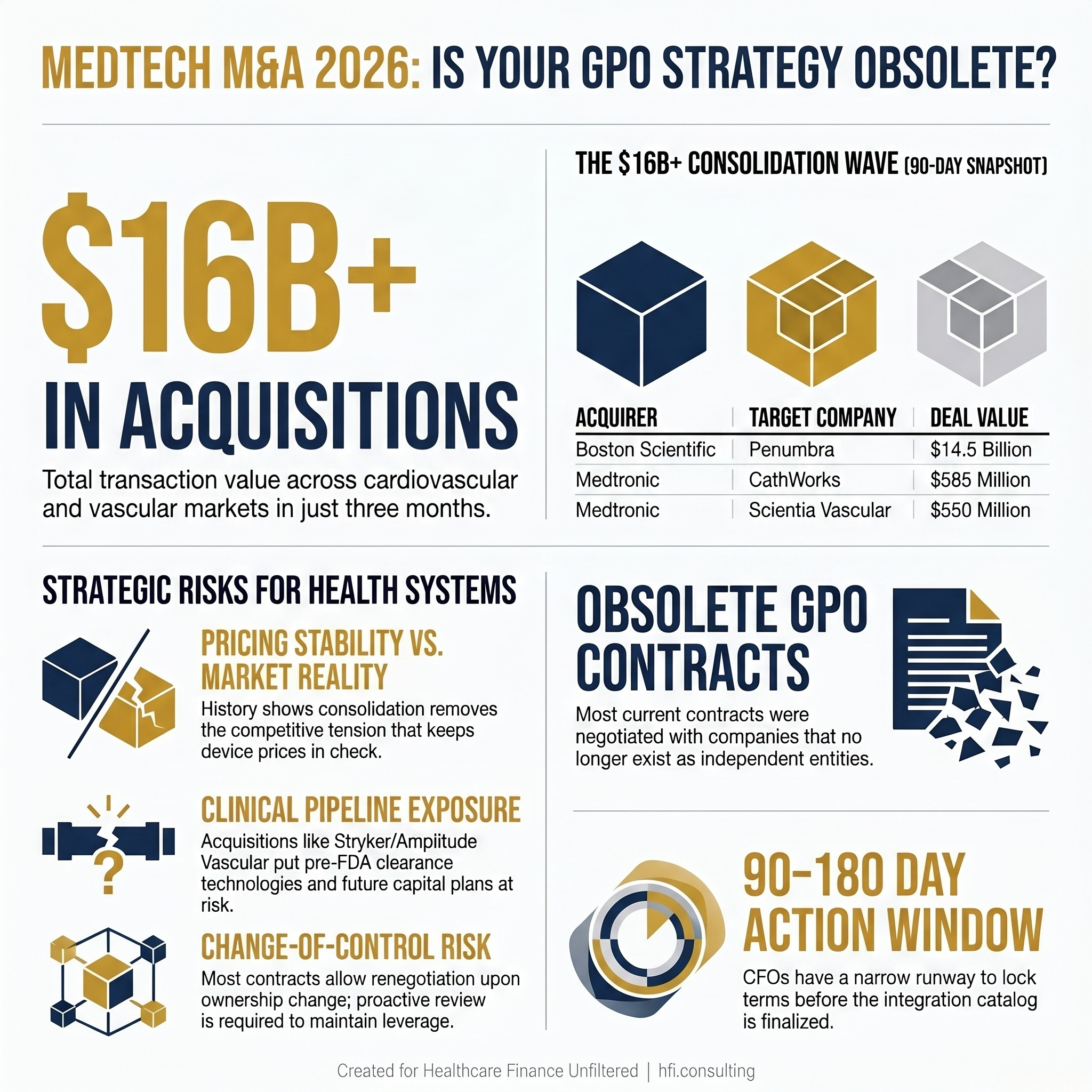

Four major medtech acquisitions have closed or been announced in the last 90 days, moving more than $16 billion in transaction value across the cardiovascular and vascular device markets. Your current GPO contracts were negotiated with companies that, in some cases, no longer exist as independent entities. The pricing, service terms, and device availability your supply chain team is counting on for the next budget cycle may be based on a vendor landscape that is already obsolete.

Graphic showing four 2025-2026 medtech acquisitions totaling over $16 billion, with company names, deal values, and a note that GPO contracts were written before the consolidation wave.

The Consolidation Is Not Slowing Down

Boston Scientific agreed to acquire Penumbra, a California-based mechanical thrombectomy and neurovascular device maker, for approximately $14.5 billion. The deal values Penumbra at $374 per share and adds a company generating roughly $1.4 billion in annual revenue. For health systems with vascular surgery programs and stroke intervention capability, the clinical implications are significant. But the financial implications for supply chain leadership may arrive first.

Medtronic has moved on two fronts simultaneously. Its acquisition of CathWorks, an Israeli company whose FFRangio system uses AI algorithms to assess coronary physiology from standard X-ray images, is valued at up to $585 million. Its separate acquisition of Scientia Vascular, a Salt Lake City-based stroke treatment device maker, carries a price tag of approximately $550 million. Medtronic has framed both deals as portfolio expansion moves in cardiology and neurovascular care. Supply chain leadership should frame them differently: as potential triggers for SKU consolidation, pricing renegotiation, and GPO tier restructuring.

Stryker entered the intravascular lithotripsy market by acquiring Boston-based Amplitude Vascular Systems, whose Pulse IVL platform is still in clinical trials and has not received FDA clearance. That deal has no disclosed price, but it positions Stryker directly against Shockwave Medical (now Johnson and Johnson MedTech), Boston Scientific, Abbott, and Philips in one of the most actively contested device categories in cardiology.

This is not a wave of small strategic tuck-ins. These are platform-defining acquisitions, and each one changes the negotiating position of the acquiring company in your service line budget conversations.

What Happens to Your GPO Contract When the Vendor Changes Hands

Group purchasing organizations exist to aggregate volume and extract pricing concessions from device manufacturers. That leverage depends on the assumption that the manufacturer values the contract relationship. Post-acquisition, that assumption requires verification.

When a large company like Boston Scientific acquires Penumbra, the integration team's first task is rationalizing the product portfolio. Devices that overlap with existing Boston Scientific offerings face discontinuation risk. Devices that compete with other GPO-contracted vendors face pressure to migrate volume. And contracts negotiated by Penumbra directly, whether GPO-routed or independently sourced, are subject to the acquiring company's review.

Health systems that have relied on sole-source or dual-source contracting arrangements with any of the acquired companies should pull those agreements now and review the assignment and change-of-control provisions. Most healthcare device contracts include language that allows either party to trigger renegotiation upon an ownership change. The question is whether your supply chain team is reading that language proactively or waiting until a price change notification arrives.

The GPO relationship also shifts. If Penumbra devices were purchased through Vizient, Premier, or HealthTrust contracting vehicles, Boston Scientific may honor existing tier pricing for a transition period and then restructure the catalog entirely. That transition period is your window for action. It typically runs 90 to 180 days post-close, which in Boston Scientific's case means CFOs have a narrow runway to lock favorable terms before the integration catalog is finalized.

Decision tree diagram showing four parallel post-acquisition review tracks for hospital supply chain teams responding to medtech M&A, including contract language review and GPO transition pricing steps.

Pricing After Consolidation: The History Is Not Encouraging

The medtech consolidation of the past decade has not produced broadly lower device prices for health systems. The research on this is consistent enough that supply chain leaders should treat pricing stability post-acquisition as a risk assumption, not a baseline expectation.

When a large acquirer absorbs a competitor, the competitive tension that kept prices in check disappears. If Boston Scientific now controls Penumbra's thrombectomy devices and also holds its own competing line, the internal incentive to discount either product diminishes. If Stryker's Pulse IVL platform eventually reaches FDA clearance and commercial launch, the pricing conversation in that category will involve fewer independent competitors than it did 18 months ago.

The antitrust review process exists precisely to evaluate these dynamics. Several of the deals announced in early 2026 have or will face Federal Trade Commission review. The FTC's posture on medtech consolidation has tightened in recent years, and deals that create dominant market positions in specific clinical categories face longer review timelines and potential divestitures. For CFOs, government scrutiny is not irrelevant to financial planning. A deal that is blocked or required to divest a specific product line changes the integration calculus in ways that affect your service line cost structure.

In my work supporting finance teams managing capital-intensive service lines, the pattern I see most often is this: the contract risk is identified during the due diligence phase of the acquisition by the acquirer's team, not by the health system's. By the time supply chain leadership is notified of pricing changes, the negotiating leverage has already shifted. The window for favorable terms had closed during the transition period while institutional attention was elsewhere.

Innovation Access and the Device Pipeline Question

One argument in favor of large-scale medtech consolidation is that it accelerates innovation by giving smaller companies access to global distribution and deeper R&D investment. That argument has merit in some cases. The Medtronic-CathWorks deal is a reasonable example. FFRangio has strong diagnostic accuracy data and has been in limited commercial deployment. Medtronic's distribution network could accelerate access for cardiology programs that have not yet adopted noninvasive FFR assessment.

But the opposite outcome is also well-documented: acquired products that compete with the acquirer's existing portfolio get deprioritized, under-invested, or quietly discontinued. A device that had a viable commercial roadmap under independent ownership becomes a legacy product under a large parent whose priorities lie elsewhere. For health systems that have built clinical protocols around specific technologies, that discontinuation risk is a real operational exposure.

The Stryker acquisition of Amplitude Vascular Systems is worth watching specifically because the Pulse IVL platform is pre-FDA clearance. Stryker is betting on a clinical trial outcome and a regulatory pathway that has not yet materialized. If the trial data disappoints or the FDA review extends significantly, Stryker's competitive entry into IVL may be delayed or restructured. The health systems most exposed are those that have built capital planning assumptions around expanded IVL access in a more competitive market.

Supply chain leadership and clinical operations need to be in the same room for this analysis. A device acquisition that looks like a vendor consolidation from the finance side may represent a significant clinical workflow change from the cardiology or vascular surgery team's perspective. That coordination rarely happens early enough.

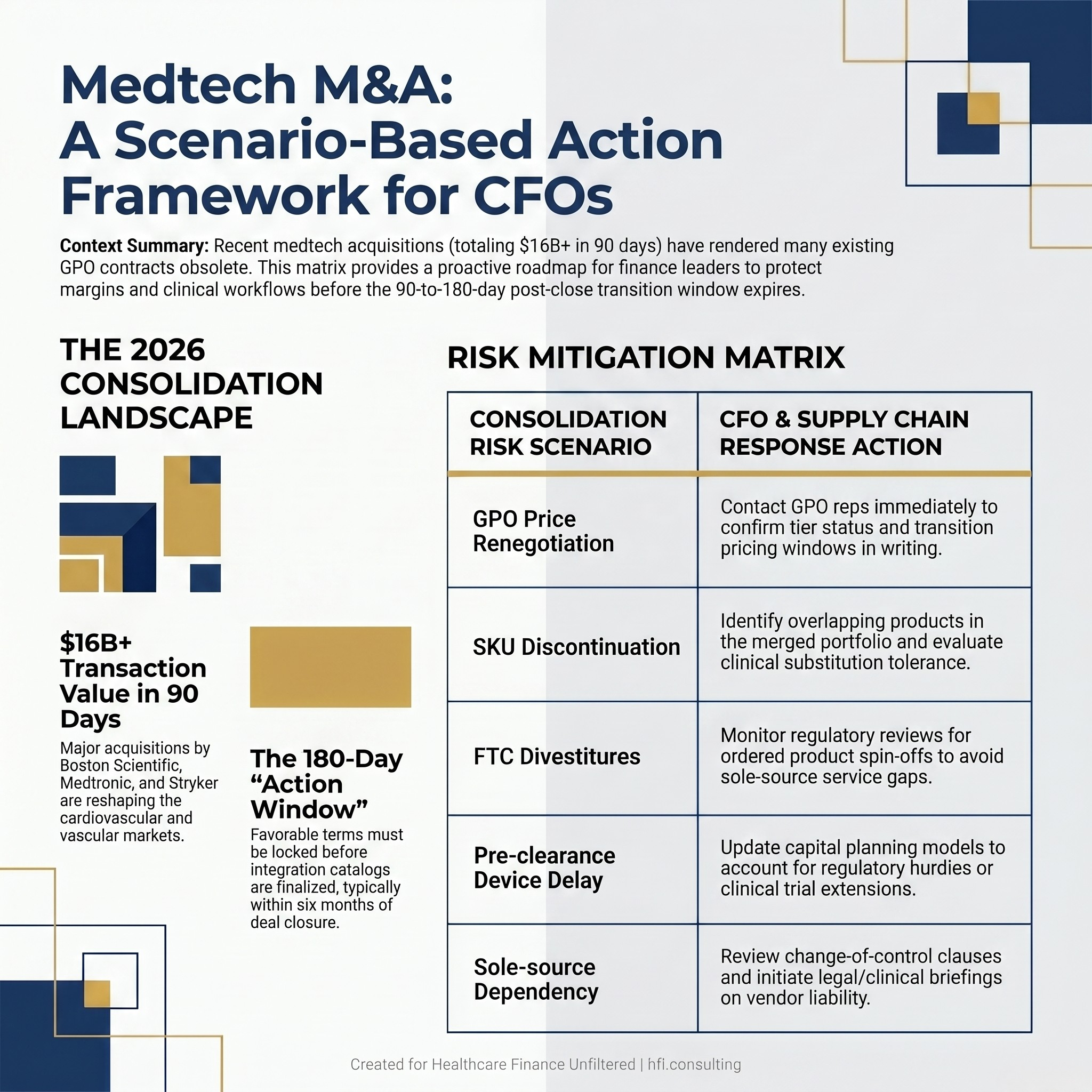

Comparison table showing five medtech M&A consolidation risk scenarios on the left and corresponding CFO response actions on the right, for hospital supply chain and finance leadership teams.

The Regulatory Scrutiny Variable

Not all of these deals will close unchanged. The FTC and Department of Justice have both indicated increased willingness to challenge healthcare sector consolidations that reduce competition in defined clinical markets. The Boston Scientific and Penumbra deal, given its scale and the breadth of Penumbra's device portfolio, will receive careful review.

The practical implication for health systems is that some devices you are counting on to be integrated into a single vendor relationship may instead be divested to a third party or held as a separate commercial entity. Contracts signed with the acquiring company may not transfer cleanly if a divestiture is required. Supply chain teams that are already mapping their medtech vendor dependencies have a significant planning advantage over those waiting to see how the regulatory process concludes.

This is also a moment where the CFO and the General Counsel's office need a shared briefing. The change-of-control provisions in device contracts, the implications of an FTC-ordered divestiture on a sole-source arrangement, and the liability exposure if a critical device becomes commercially unavailable mid-contract are all questions that require legal review alongside financial analysis. I have seen that coordination happen reactively, after a disruption, far more often than proactively. The cost differential between those two approaches is not abstract.

If your supply chain or finance team is mapping medtech vendor exposure right now and you want a structured framework for doing that analysis, Healthcare Finance Unfiltered has a practical workbook designed for exactly this kind of contract risk review. Visit hfi.consulting to learn more, or subscribe below to get the next piece in this series on device cost management and service line margin protection.

What Finance Leadership Should Be Doing Right Now

The action framework is not complicated, but it requires discipline to execute before the transition period closes.

First, pull a complete list of device vendors across your high-cost service lines: cardiovascular surgery, vascular surgery, orthopedics, and neurology are the highest-priority categories given the current deal flow. Map each vendor against the recent acquisition announcements. Any vendor that has been acquired, is in the process of being acquired, or operates in a category where a competitor has recently been acquired needs individual contract review.

Second, contact your GPO account team directly. Do not assume the GPO will proactively notify you of pricing changes triggered by an acquisition. Ask specifically whether the acquired company's products remain on contract, at what tier, and for what transition period. Get the answer in writing.

Third, identify your sole-source clinical dependencies. A device that has been sole-sourced because a surgeon prefers it or because no clinical equivalent has been validated is a different risk profile than a GPO-contracted commodity item. Both need review, but the clinical engagement required is different. Sole-source dependencies need a conversation with clinical leadership about substitution tolerance before the supply chain disruption forces that conversation.

Fourth, flag any capital planning assumptions that include devices currently in the pre-clearance pipeline. The Stryker-Amplitude Vascular deal is one example. If your cardiology capital plan assumes expanded IVL access in a more competitive, lower-cost market, the Stryker acquisition changes that assumption in ways that need to be modeled.

In my experience working across multi-hospital systems, the supply chain disruption risk from medtech M&A almost never shows up on the finance team's risk register in advance. It shows up in the variance report six months after a pricing change that nobody caught in time. The current consolidation wave is visible enough and large enough that proactive action is both feasible and warranted.

A Note on the Talent Side

The Medtronic acquisitions in particular involve companies with specialized technical talent in AI-enabled diagnostic imaging and neurovascular device engineering. Post-acquisition workforce integration is rarely clean. Engineers and clinical specialists who were central to the acquired company's product development sometimes exit rather than integrate into a large corporate structure.

For health systems that rely heavily on vendor clinical specialists for device training, credentialing support, and intraoperative guidance, workforce volatility at a newly acquired company is a service risk. The clinical specialist who has been in your OR every Thursday may not be there after the acquisition closes. Ask your device vendor contacts directly about post-acquisition staffing plans. That question is uncomfortable but necessary.

Healthcare Finance Unfiltered publishes practical analysis for CFOs and finance leaders navigating the operational and contractual complexity of a changing healthcare market. If this piece was useful, subscribe to receive new articles directly. If you are managing a specific supply chain or vendor contract challenge, visit hfi.consulting to explore how I work with health system finance teams on targeted cost and contract risk reviews.

P.S. For the supply chain and finance leaders reading this: which of your current device vendors are you most concerned about as the consolidation wave continues? Is it a sole-source dependency, a GPO contract question, or something in your capital plan that is now based on an assumption that may not hold? Hit reply and tell me where the pressure point is. I am tracking these scenarios across reader feedback to inform the next piece in this series.