Hospital at Home After the 2030 Extension: Finance Leaders' 12-Month Planning Guide

The waiver is locked in. Florida programs are expanding. What providers and payers must model in the next 12 months.

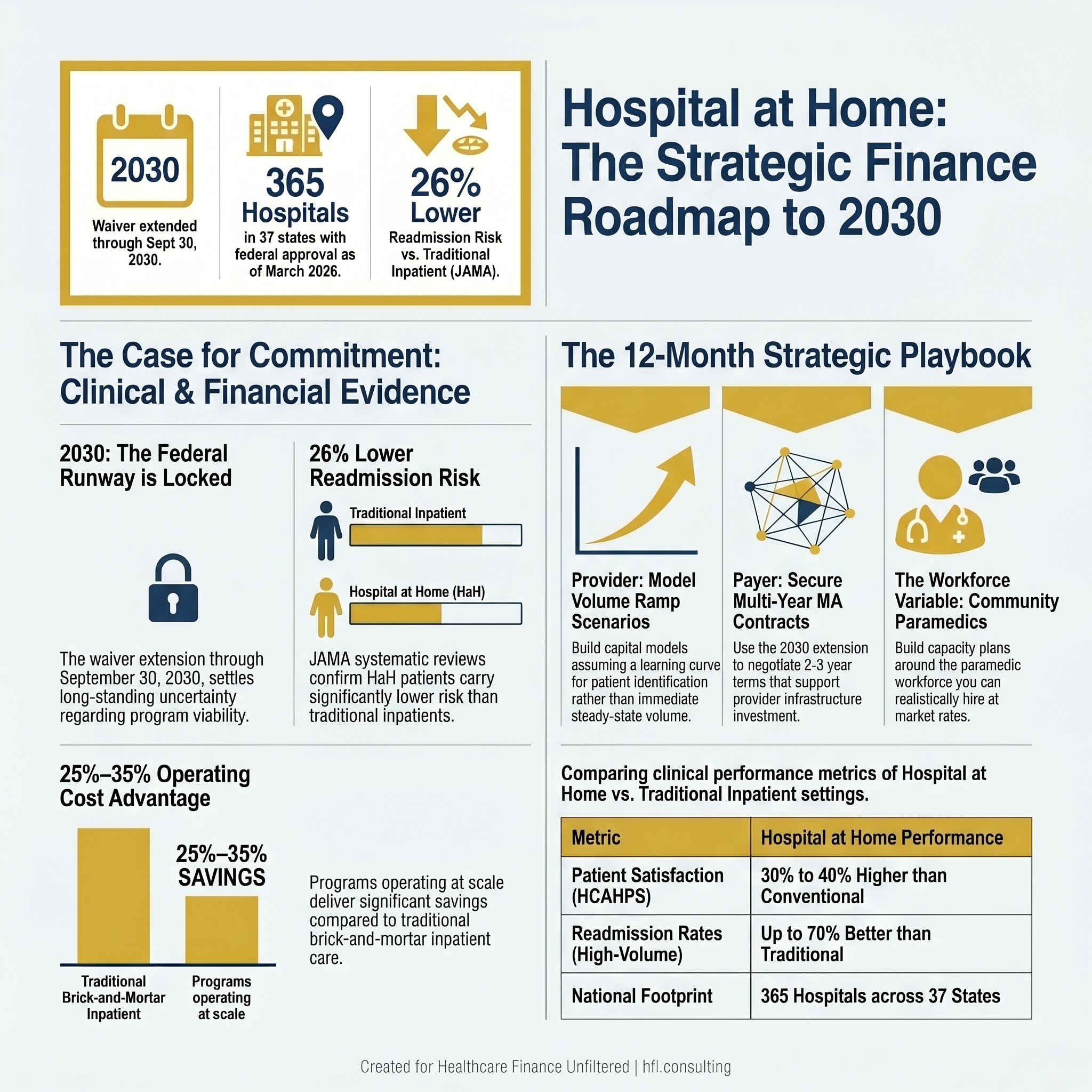

The five-year waiver extension settled the existential planning question that had been stalling Hospital at Home investment for years. Finance leaders who deferred capital commitments pending Congressional action now have their answer: the Acute Hospital Care at Home program runs through September 30, 2030, and Florida health systems are moving.

Tampa General Hospital expanded its Hospital at Home program to Citrus County in March 2026, building on a flagship campus program at Davis Islands that has served more than 2,500 patients since 2022. Baptist Health Jacksonville operates a program treating pneumonia, COPD, cellulitis, and urinary tract infections. BayCare and Health First are among the broader Florida systems with federal approval to participate, alongside 138 systems and 365 hospitals across 37 states as of the most recent CMS data release.

The question is no longer whether Hospital at Home is a viable care model. The question is how finance leaders on both the provider and payer sides translate a five-year federal runway into 12-month operating decisions.

Three-panel stat card showing Hospital at Home federal extension date, national hospital participation count, and JAMA readmission reduction data

What the CMS Data Release Actually Tells You

CMS released a second tranche of Acute Hospital Care at Home data in March 2026, covering April 2023 through September 2025. Combined with the initial release, researchers and finance teams now have access to nearly five years of program data including admission volumes, care escalations, and unanticipated mortality rates.

For finance leaders, this matters because five years of data closes the "insufficient evidence" argument that had been used to justify conservative capital planning. The clinical track record from high-volume programs like Tampa General's, which reported a 30-day readmission rate approximately 70% better than its brick-and-mortar facility, now has enough methodological depth to support serious financial modeling.

JAMA's systematic review of nine studies found Hospital at Home patients carried a 26% lower risk of readmission compared to traditionally hospitalized patients. Patient satisfaction data from TGH shows 30% to 40% higher HCAHPS scores than conventional inpatient settings. These are not pilot numbers. They are repeatable results from programs operating at scale.

The Provider-Side Finance Case for the Next 12 Months

Health system CFOs evaluating Hospital at Home investment in 2026 are working in a different environment than they were 18 months ago. The waiver extension removes the program viability uncertainty. The question now is whether your organization has the infrastructure to build a financially sustainable program before competitors capture the patient volume.

The cost structure for Hospital at Home differs meaningfully from inpatient care. Staffing models rely on community paramedics, telehealth nursing visits, and remote monitoring equipment rather than 24/7 bedside nursing. Baptist Health's program delivers at least two daily in-person visits from a community paramedic, a daily virtual physician visit, and 24/7 remote monitoring. Tampa General's Citrus County program uses the VSee telehealth platform to maintain continuous physician access.

The operating cost advantage over traditional inpatient care runs roughly 25% to 35% per admission when programs are operating at volume. Getting to volume is where most health system finance teams underestimate the ramp timeline.

Four-stage Hospital at Home program launch timeline for health system finance leaders covering infrastructure, volume ramp, and contribution margin tracking milestones

Programs need patient volume to justify the technology infrastructure, staffing model, and care coordination overhead. Early volume shortfalls are not evidence that Hospital at Home does not work. They are evidence that patient identification, care team education, and admission criteria clarity were not tight enough during launch. Finance leaders should build ramp scenarios into their capital models rather than assuming steady-state volume within the first two quarters.

Contribution margin tracking for Hospital at Home admissions requires the same discipline as any service line. What payer mix is generating these admissions? What are the contracted rates for Medicare fee-for-service versus Medicare Advantage versus commercial plans? Are readmission costs being attributed back to the Hospital at Home episode for full-cycle margin analysis?

In my work at Ascension across seven hospitals in Florida, service line contribution margin analysis consistently surfaced assumptions about program profitability that did not hold when readmission costs and overhead allocation were properly assigned. Hospital at Home is not different from any other service line in that respect.

For the foundational financial modeling discussion, the 2025 Florida health system finance guide covers the original program economics. The 2030 extension changes the capital recovery timeline assumptions but not the underlying contribution margin framework.

The Florida Medicaid Expansion Adds a Planning Variable

Florida's 2026 state provision directing the Agency for Health Care Administration to seek federal approval for Hospital at Home coverage under Medicaid adds a materially different payer population to the planning equation. Medicaid patients typically carry higher acuity comorbidities and more complex social determinants of health than Medicare fee-for-service populations.

If federal approval comes through, health systems will need to model Hospital at Home contribution margins for a Medicaid population separately from Medicare. The care coordination requirements may differ. The monitoring intensity may be higher. And the reimbursement rates will almost certainly be lower than Medicare.

Finance leaders should not assume Medicaid Hospital at Home economics mirror Medicare Hospital at Home economics. Separate scenario models, separate staffing assumptions, and a clear understanding of which patient populations will actually meet the clinical eligibility criteria once AHCA defines them are essential before committing capital to Medicaid-serving capacity.

The Payer-Side Planning Equation

For Medicare Advantage plans operating in Florida, the waiver extension through 2030 resolves a different planning question. MA plans that had been reluctant to formalize Hospital at Home network requirements in provider contracts because of uncertainty about program permanence now have a five-year window to build those contractual structures.

The contracting framework covered in January in Hospital at Home from the MA Plan Side remains the right starting point: base rates tied to provider cost structure by market, volume minimums with clawback provisions, and quality performance adjustments tied to readmission benchmarks. What changes with the 2030 extension is the multi-year contract duration that now makes sense.

A one-year Hospital at Home contract term does not give providers enough runway to invest in staffing infrastructure and return to profitability. With a five-year federal extension, MA plans can negotiate two and three-year contract terms that give providers financial confidence to build capacity while giving plans cost savings that compound over multiple years.

Florida's MA penetration at 55% to 60% of Medicare beneficiaries means every major plan is negotiating Hospital at Home terms with the same provider systems simultaneously. The race-to-the-bottom dynamic on rate negotiations does not resolve itself with a longer waiver extension. If anything, it will intensify as more systems launch programs and more plans attempt to capture savings.

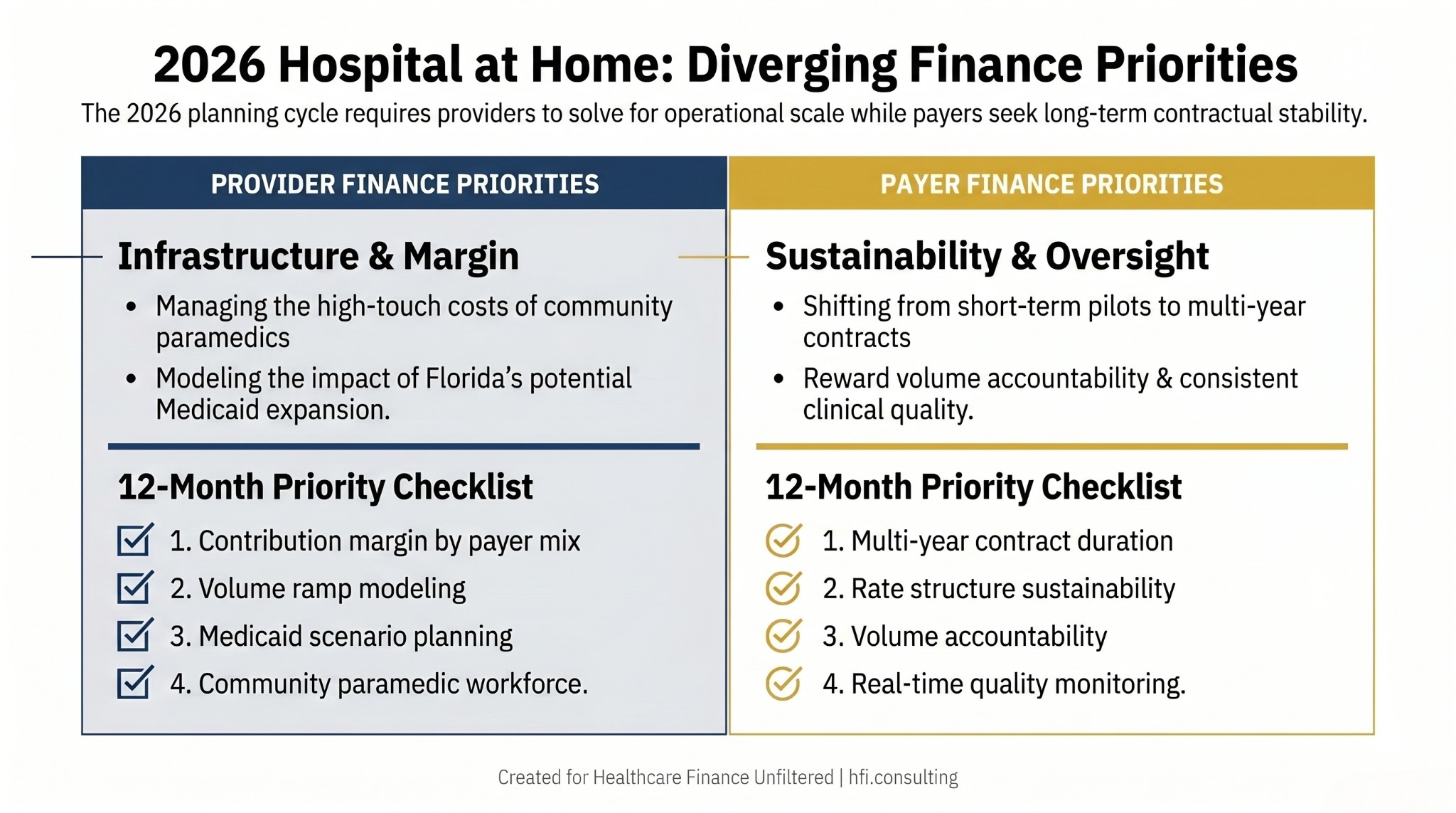

Side-by-side comparison of Hospital at Home finance planning priorities for health system CFOs versus Medicare Advantage plan finance leaders

The plans that get this right in 2026 are the ones that build collaborative provider relationships rather than aggressive rate negotiations. Providers with financially sustainable Hospital at Home programs deliver better clinical outcomes, sustain higher volumes, and generate the readmission performance that actually produces plan savings.

The CY 2027 Medicare Advantage Final Rule planning guide covers the broader MA rate environment for 2026 planning. Hospital at Home cost reduction is one of the few remaining levers available to plans managing margin pressure in a tightening rate environment.

The Telehealth Infrastructure Question Both Sides Share

Hospital at Home is functionally a telehealth-enabled care model. The daily virtual physician visits, continuous remote monitoring, and care team communication platforms all require reliable digital infrastructure at the patient's home. That means broadband access, compatible devices, and patient and family technology competency.

The patient eligibility criteria at Tampa General's Citrus County program include a requirement that patients live within 30 minutes of a TGH hospital or emergency department. This geographic constraint reflects both the clinical need for rapid escalation capability and the practical reality that technology-dependent care models require local team response capacity.

Finance leaders on both the provider and payer sides need to model Hospital at Home eligibility conservatively. Not every patient who meets the clinical criteria will have the home environment, technology access, or family support structure to succeed in the program. Overestimating eligible volume is the most common financial planning error in Hospital at Home business cases.

The telehealth reimbursement and capital planning framework covers the broader infrastructure investment context that Hospital at Home programs build on.

The Staffing Model Is the Variable That Breaks Plans

Community paramedics are the operational backbone of Hospital at Home programs. They deliver in-person care, conduct physical assessments, administer medications, and escalate to higher-level care when clinical status changes. The supply of trained community paramedics in most Florida markets is not unlimited.

Health systems expanding Hospital at Home programs in 2026 will compete for the same community paramedic workforce. Programs that launch with understaffed in-person visit capacity will generate safety incidents, regulatory attention, and patient satisfaction problems that undermine the entire program's financial case.

Finance leaders should model Hospital at Home staffing costs at realistic market rates, including the premium required to attract and retain community paramedics away from traditional roles. Labor cost assumptions built on current base pay without accounting for program-specific premium pay will produce operating cost projections that do not hold.

Build your program capacity plan around the community paramedic workforce you can actually hire and retain, then model your volume targets accordingly. Starting with volume targets and working backward to staffing requirements is the planning sequence that produces programs that look profitable on paper and fail operationally.

Four-quadrant feasibility matrix for hospital CFOs assessing Hospital at Home program viability based on workforce availability and payer rate sustainability

Where to Focus in the Next 12 Months

For provider finance leaders, the immediate priorities are building financial modeling infrastructure that separates Hospital at Home contribution margin by payer, running realistic volume ramp scenarios that account for the patient identification learning curve, and establishing readmission attribution protocols before the program goes live.

For payer finance leaders, the immediate priorities are auditing current Hospital at Home contract language against the three-part framework of base rates, volume minimums, and quality adjustments, and assessing whether contract durations are now appropriate for multi-year terms given the 2030 extension.

If your organization is evaluating Hospital at Home program design, financial modeling, or payer contract structure for 2026 and 2027, HFI Consulting brings direct operational experience on both the provider and payer sides of these programs. Visit hfi.consulting to connect.

The Regulatory Clarity You Actually Have

The extension through 2030 gives finance leaders something they have not had since the program launched in November 2020: a defined planning horizon. The waiver does not make Hospital at Home permanent, but it gives organizations enough time to build, iterate, and optimize programs before the next legislative cycle.

Hospital at Home's patient satisfaction data is among the strongest in modern care delivery. TGH's 30% to 40% HCAHPS improvement over traditional inpatient settings, combined with 70% better 30-day readmission rates, represents clinical performance that finance leaders can build durable business cases around.

The programs that have produced these results share common financial characteristics: realistic volume ramp assumptions, sustainable reimbursement rates that give providers operational margin, and continuous quality monitoring that catches problems before they compound. For healthcare finance leaders on both sides, the 2030 extension is an invitation to build something designed to last rather than to hedge against regulatory discontinuation. That design decision starts with the financial framework you establish in the next 12 months.

For a deeper look at how Hospital at Home fits within the broader value-based care strategy your organization is navigating, the value-based payment models planning guide covers the overlapping financial frameworks that CFOs are managing simultaneously in 2026.

Healthcare Finance Unfiltered is published by Rachel Barksdale, MHA, CHFP. Connect with HFI Consulting at hfi.consulting.

P.S. Is your organization currently operating a Hospital at Home program, in the planning stages, or still in a holding pattern? Hit reply and let me know what's blocking or enabling the decision.