Healthcare Price Transparency for Insurance CFOs: Managing Rate Convergence and the End of the Black Box

Your negotiated rates are now public. PBM reform under CAA 2026 is live. Here is how payer finance leaders rebuild their strategy from the ground up.

Series Note: This is Part 2 of a two-part series on healthcare price transparency. Part 1 covers the hospital and health system CFO perspective.

Transparency in Coverage mandates have turned your negotiated rate schedule into a public dataset, and CAA 2026 is unwinding the PBM rebate model simultaneously. This payer CFO framework covers TiC compliance evolution, rate convergence pressure from self-insured employers, PBM reform impact on pharmacy cost models, zombie rate elimination requirements, and the strategic pivot from network aggregator to value-based plan designer. Part 2 of 2.

Healthcare Finance Unfiltered featured image for payer CFO price transparency article covering TiC compliance, rate convergence, PBM reform under CAA 2026, and value-based plan design.

For years, the health insurance CFO's most defensible competitive asset was the rate schedule negotiated at scale with local provider networks. The secrecy surrounding those rates was not incidental. It was the product. Large carriers used volume to extract deep discounts, then sold access to those discounts as the core value proposition to self-insured employers and brokers.

Federal transparency mandates have turned that asset into a public utility.

Your Transparency in Coverage filings are now accessible to any employer with a benefits consultant and a data aggregator subscription. The Consolidated Appropriations Act of 2026 is unwinding the PBM revenue model that funded a significant portion of your pharmacy cost management infrastructure. And the structural reality your commercial strategy was built on, that you negotiated better rates than competitors and kept that fact confidential, is no longer operationally viable.

This is Part 2 of a two-part series on healthcare price transparency. What follows is the payer CFO framework for managing rate convergence, the new TiC compliance obligations, PBM reform under CAA 2026, and the strategic transition from proprietary discount aggregator to value-based plan designer.

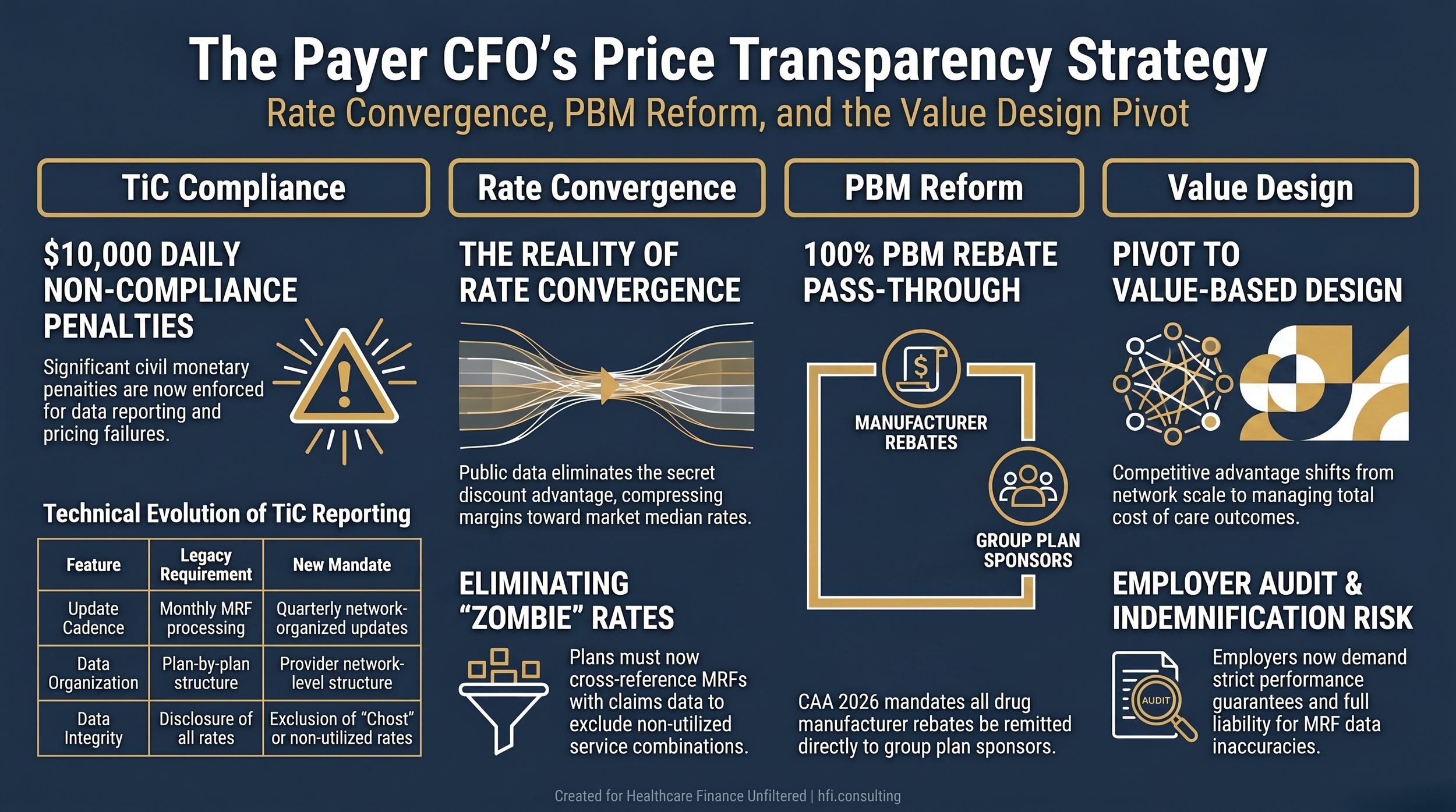

What the TiC Overhaul Actually Changed for Your Finance Team

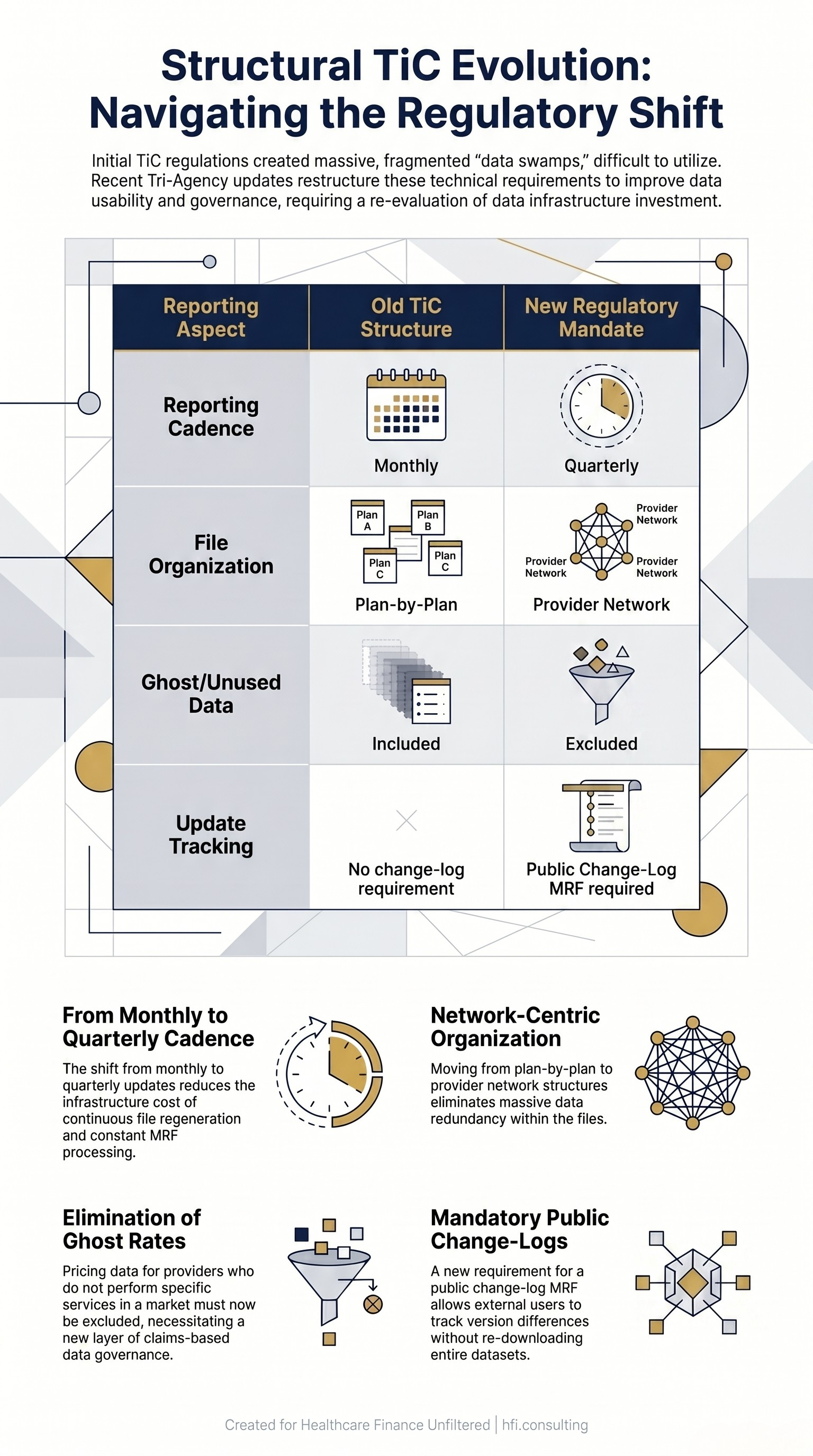

The initial Transparency in Coverage regulations created what the industry started calling data swamps. Insurers were required to publish monthly machine-readable files covering every negotiated rate for every covered service, organized at the plan level rather than the network level. The resulting files were measured in terabytes, updated continuously, and so fragmented that even large employers with sophisticated analytics teams found them difficult to use.

Tri-Agency regulatory updates from HHS, the Department of Labor, and Treasury have restructured the technical requirements in ways that carry direct finance and operations implications.

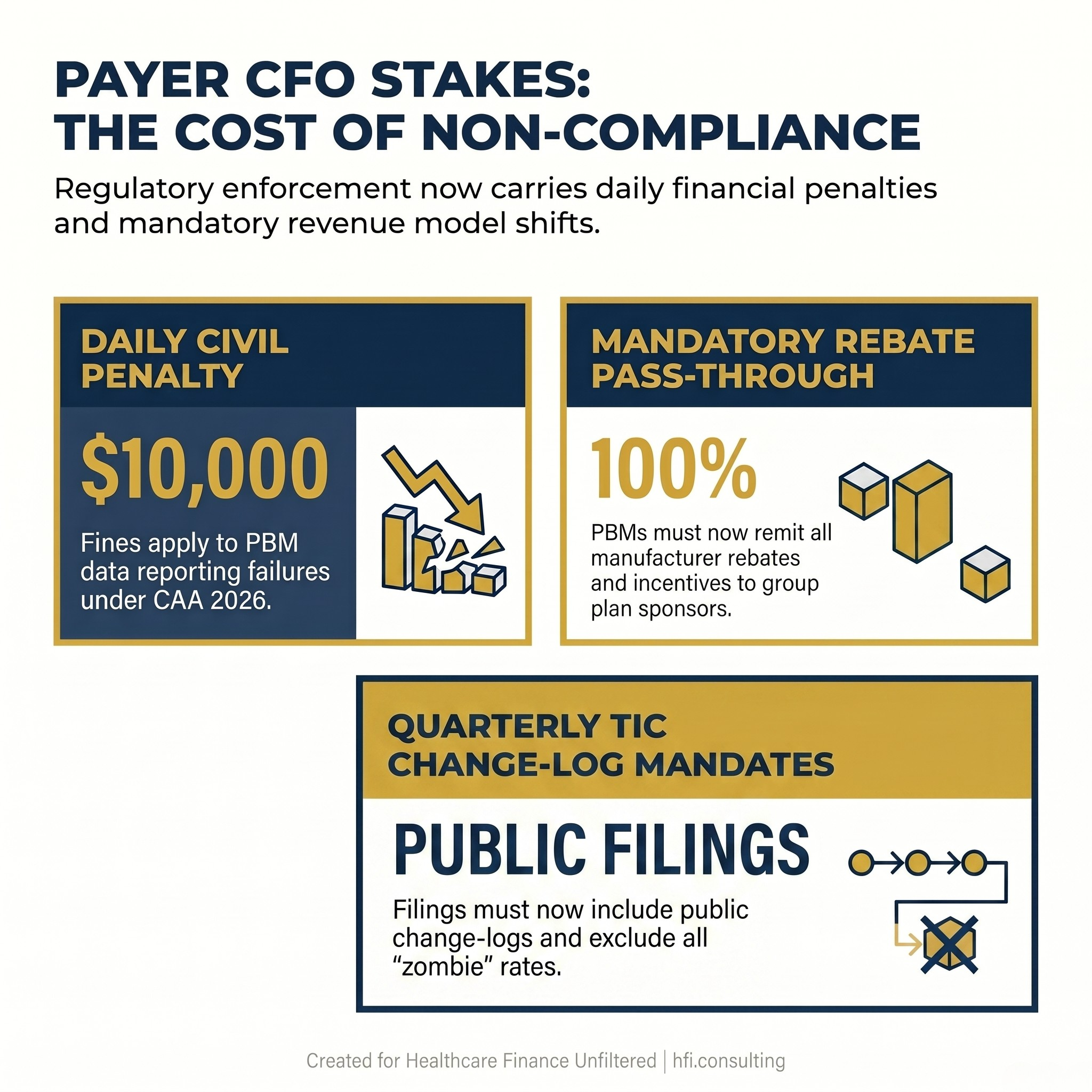

The monthly update cadence that forced continuous MRF processing has shifted to quarterly updates, reducing the infrastructure cost of continuous file regeneration. File organization has moved from a plan-by-plan structure to a provider network structure, which eliminates significant data redundancy. Ghost rates, pricing data published for providers who do not actually perform that service in that geographic market, must now be excluded rather than simply disclosed. And a public change-log MRF is required so external users can track exactly what changed between file versions without re-downloading the entire dataset.

For insurance finance teams, these structural changes do not reduce the operational burden of TiC compliance. They redirect it. The quarterly cadence reduces continuous processing overhead. But the taxonomy and utilization filing requirements, proving which providers actually delivered specific services over the prior twelve months, add a new data governance layer that most insurer IT architectures were not designed to support at launch.

The capital allocation decision here is significant. Building or licensing the data infrastructure to produce compliant, accurate, usable TiC files is not optional, and underinvesting in it creates both regulatory exposure and the commercial liability that follows when employer clients discover your published files are inaccurate or incomplete.

Three regulatory data points for insurance CFOs on CAA 2026 PBM reform and Transparency in Coverage requirements, including $10,000 daily penalty for non-compliance.

Rate Convergence: When Your Secret Discount Is Everyone's Benchmark

The single most consequential competitive shift created by payer MRF transparency is rate convergence. Your large-scale volume negotiation produced discounts that smaller regional plans and startup insurers could not match. That negotiating advantage was real. It created sustainable margin spread in your commercial book of business.

With every insurer's rates public, that structural advantage has narrowed. Regional plans and tech-forward startup insurers can query exactly what your contracts pay local hospitals by procedure code. They can see where you negotiated a strong rate and where you did not. They can price their own products accordingly.

The squeeze is coming from the employer side simultaneously. Self-insured corporate clients are pairing your published MRF data with third-party data aggregators to audit their Administrative Services Only agreements. If your plan is paying $4,500 for a procedure that a competing plan is paying $2,000 for at the same facility, the employer's benefits consultant will find that differential. The conversation that follows is not a routine renewal negotiation. It is a mid-cycle contract challenge or a threat to move the business.

This dynamic is producing a macro-trend that payer CFOs need to model explicitly: rate convergence across commercial markets. The high-margin rate spread that large carriers historically commanded over smaller competitors is compressing as the data becomes publicly legible. Modeling your commercial margin trajectory without accounting for rate convergence risk is incomplete scenario planning.

The Employer Audit Problem and the Indemnification Risk

A substantial portion of health plan revenue comes from acting as a Third-Party Administrator for self-insured employers. Under ERISA and the Consolidated Appropriations Act, the legal obligation to publish accurate MRF files technically belongs to the employer sponsoring the plan. Because employers lack the technical infrastructure to generate terabyte-scale data files, they delegate this obligation to their TPA insurer through administrative contracts.

That delegation arrangement has become a significant source of legal and financial exposure for insurance CFOs.

Comparison table showing four key structural changes to Transparency in Coverage requirements for insurance CFOs, from monthly filing to quarterly network-organized MRF with change logs.

Employers are now demanding absolute indemnification clauses and strict performance guarantees in their TPA agreements. If your plan fails to format a data dictionary field correctly, drops a file link, or publishes rates that do not match current provider contract terms, and that failure results in the employer facing federal compliance audits or shareholder class-action lawsuits for breach of ERISA fiduciary duty, the financial liability follows the indemnification language. For most current TPA agreements, that means it lands on your balance sheet.

From the payer side at a Medicare Advantage plan, the fiduciary pressure was already a consistent undercurrent in employer and broker conversations before TiC mandates formalized it. What has changed is the legal precision of the exposure. An employer can now produce a specific data file, a specific field error, and a specific date to establish that your plan failed its TPA obligation. That is a materially different legal situation than the pre-transparency era, when disagreements about network performance or pricing were difficult to document at that level of specificity.

For insurance CFOs, the implication is twofold. First, TPA contract language needs to be reviewed with specific attention to the MRF accuracy guarantees you are providing and the indemnification scope you are accepting. Second, the data governance infrastructure that supports TiC compliance is not just a regulatory cost center. It is a liability management function.

CAA 2026 and PBM Reform: What the Rebate Pass-Through Means for Your Drug Cost Models

The Consolidated Appropriations Act of 2026 includes the most consequential federal PBM statutory reform to date, and its financial implications for insurance CFOs extend well beyond the PBM contracting relationship.

The core mandate is a 100 percent rebate pass-through requirement. PBMs must now remit all manufacturer rebates, administrative fees, alternative discounts, and financial incentives back to the group plan sponsor on a quarterly basis. The practice of retaining a portion of manufacturer rebates as PBM margin, which has historically been a foundational revenue mechanism for the three large PBMs, is now federally prohibited for group plan arrangements.

The CAA also effectively outlaws spread pricing in its traditional form. Under the new pass-through pricing and fee transparency requirements, plan sponsors pay exactly what the dispensing pharmacy is reimbursed plus a flat, visible administrative fee. The historical PBM model of billing the employer a higher drug price than the pharmacy reimbursement and retaining the spread as profit no longer complies with the statute.

Non-compliance penalties are structured to be operationally consequential. Civil monetary penalties of $10,000 per day for data reporting failures, and up to $100,000 for knowingly providing false pricing information, are calibrated to make non-compliance expensive in real time rather than in periodic settlement negotiations.

For Medicare Part D specifically, PBM compensation has been legally delinked from drug list prices. PBMs managing Part D plans may only be compensated through a flat-dollar bona fide service fee at fair market value. Percentage-based compensation tied to list price or utilization is prohibited, and any manufacturer discounts received must be fully passed through and documented via Direct and Indirect Remuneration reporting.

The finance implication for insurance CFOs is this: the drug cost models your actuarial team built on the assumption of PBM rebate offsets need to be re-examined. How much of your current pharmacy trend management depends on rebate income that will now flow through to your employer clients? What is the net impact on your medical loss ratio projections once that revenue stream is reclassified? These are budget questions that cannot wait for the next planning cycle.

If you are working through the actuarial and operational implications of CAA 2026 PBM reform for your plan's financial model, this is the kind of analysis HFI Consulting supports. You can connect directly through hfi.consulting or reply to this email.

Eliminating Zombie Rates and What the Taxonomy Mandate Costs You

One of the most operationally demanding components of the updated TiC requirements is the mandate to eliminate what regulators call ghost or zombie rates from published MRF files.

Ghost rates are pricing data published for providers who do not actually perform a specific service in a given geographic market. These rates accumulate over time in large carrier files because it is easier to publish every provider in a network against every covered service than to validate which providers actually delivered which services in which locations during a defined period.

The updated Taxonomy and Utilization Filing requirement forces insurers to verify and document, using actual claims data from the prior twelve months, which providers performed which specific services. Rates for provider-service combinations that do not appear in the utilization data must be excluded from the published file.

For large commercial carriers with national networks, this is a significant data engineering problem. The clean-up process requires cross-referencing your entire published rate schedule against your claims database, flagging every combination where no utilization appears, and removing or flagging those entries before each quarterly file submission. That is a continuous data operations task, not a one-time remediation project.

The business case for investing in this infrastructure goes beyond regulatory compliance. Accurate, utilization-validated rate files make your published data more credible to the employer clients and data aggregators who are auditing it. Zombie rates create noise that inflates apparent network size and confuses price benchmarking analysis. Employers who discover your published network is significantly larger than your actual claims-supported network will question the accuracy of your other reported data.

Three-stage diagram showing the strategic shift for insurance CFOs from proprietary network scale and rate secrecy to value-based plan design under price transparency requirements.

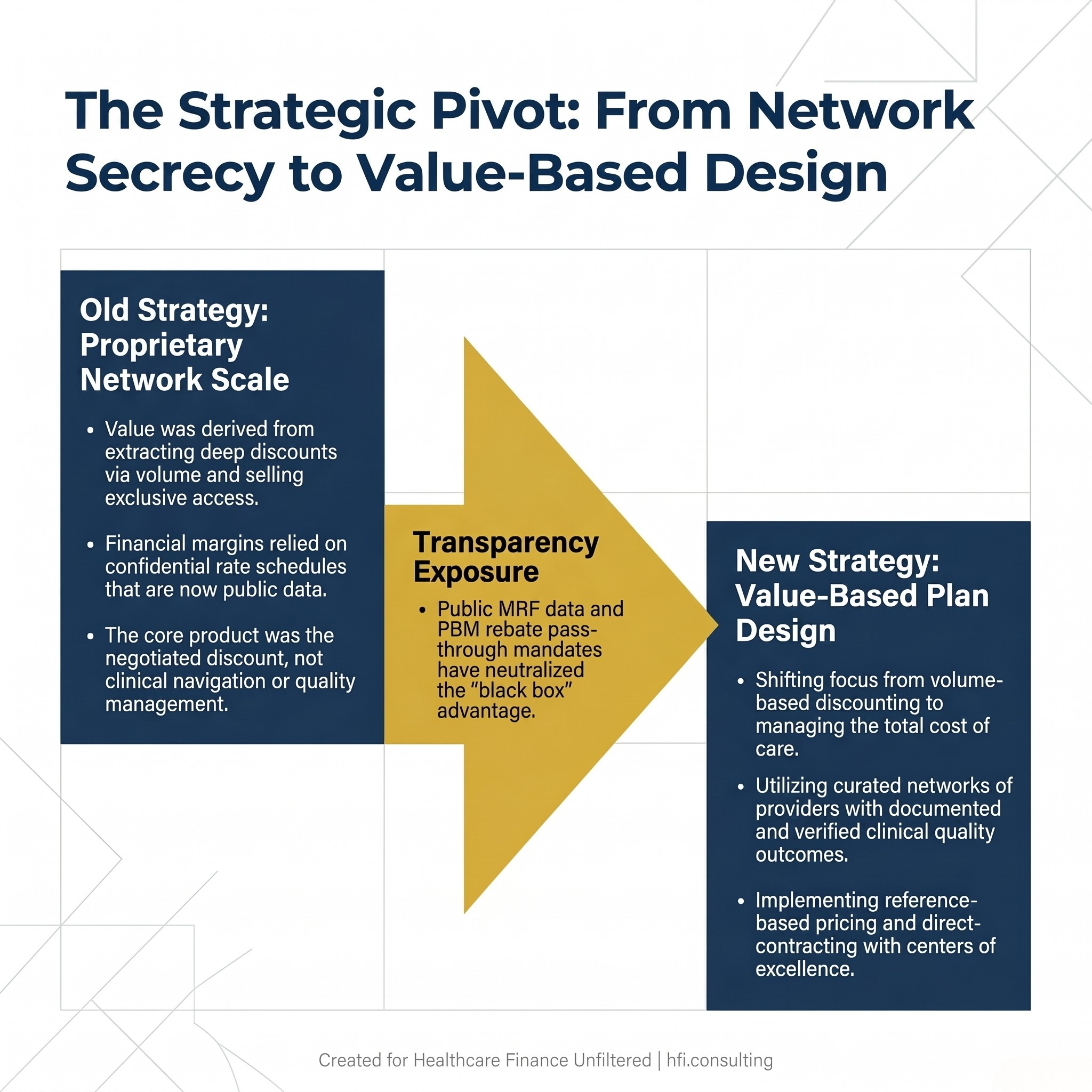

From Network Aggregators to Value Designers: The Strategic Pivot

The competitive moat that large insurance carriers built on proprietary rate data is now public domain. The strategic implication for payer CFOs is not to defend a moat that no longer exists. It is to build a different kind of competitive advantage.

The insurers that are repositioning most effectively are shifting their value proposition from volume-based rate discounting to managing total cost of care. Because the negotiated price is now visible to every employer client, the insurer's value must come from what it does with the clinical risk, the utilization data, and the care navigation infrastructure that the price alone cannot provide.

Practically, this is translating into three structural investment priorities for forward-thinking payer CFOs.

Narrow, verified networks paired with documented quality outcomes. Rather than competing on the breadth of a network that includes thousands of providers the plan's members rarely use, leading plans are building curated networks of verified high-value providers with documented clinical outcome data. The network value proposition shifts from "we have everyone" to "we have selected for quality and verified it with your claims data."

Reference-based pricing and direct-contract hybrids. Because the price is public, consultants and benefit managers can design plans that pay a defined multiple of Medicare rates, verify that rate against the published MRF data, and present that structure to hospital systems as a market-defensible benchmark. Insurers that develop expertise in designing and administering these hybrid structures will capture employer clients who are moving away from traditional ASO arrangements.

Digital navigation and chronic disease cost management. The insurers whose value proposition survives the transparency era are those who can demonstrate, with data, that their care management infrastructure produces measurable cost reductions that justify their administrative fees. Pricing is now a commodity input. Member navigation, utilization management, and chronic disease program ROI are the differentiators that will remain proprietary.

What This Means for Your 2026 Planning Assumptions

For payer CFOs building next-year financial models, price transparency creates several scenario variables that need explicit stress-testing.

Rate convergence pressure on commercial margins. Model a scenario where your highest-margin commercial contracts migrate toward market median rates over a 24-month period as employer clients use MRF data to benchmark and renegotiate.

PBM rebate recapture impact on pharmacy cost management. Quantify how much of your current pharmacy trend management depends on rebate offsets that will now pass through to employer clients under CAA 2026, and model the MLR impact of that reclassification.

TiC data infrastructure ongoing operating cost. Build the quarterly MRF production, taxonomy validation, and change-log management into your IT and data operations budget as a recurring line item, not a one-time project.

Employer TPA indemnification exposure. Review your current TPA agreement portfolio with legal for MRF accuracy guarantee language and establish the maximum exposure under your current indemnification commitments.

The structural reality is the same one provider CFOs are navigating from the other side of the negotiating table. The era of hiding margin inside data opacity is closing. For the payers whose business models depended most heavily on rate secrecy and PBM rebate offsets, the transition will require genuine strategic reconstruction. For the payers who have been building toward value-based differentiation already, the transparency era accelerates a competitive advantage they were building anyway.

For more on how payer-provider financial dynamics are shifting across Medicare Advantage and commercial markets, see the CY 2027 Medicare Advantage Final Rule analysis and The Payer-Provider Blame Game in Healthcare Costs on Healthcare Finance Unfiltered.

Healthcare Finance Unfiltered covers the financial and operational dynamics that affect both sides of the payer-provider relationship every week. If this analysis was useful, subscribe at hfi.consulting or forward it to a colleague in actuarial, managed care finance, or plan operations.

Part 1 of this series covers the hospital and health system CFO perspective on price transparency, including payer contract negotiation strategy, front-end revenue cycle integration, and MRF compliance governance.

P.S. For the payer CFOs reading this: which of these three pressure points is hitting your 2026 financial model hardest right now: the TiC data infrastructure cost, the PBM rebate pass-through impact on pharmacy trend, or the employer benchmark pressure on commercial rates? Hit reply and tell me what you are seeing.