340B Drug Pricing 2026: The CFO's 90-Day Action Plan and Long-Term Stability Framework

Eli Lilly's 45-day ultimatum, HRSA's rebate model threat, and a 2027 OPPS cut. Your CFO action guide.

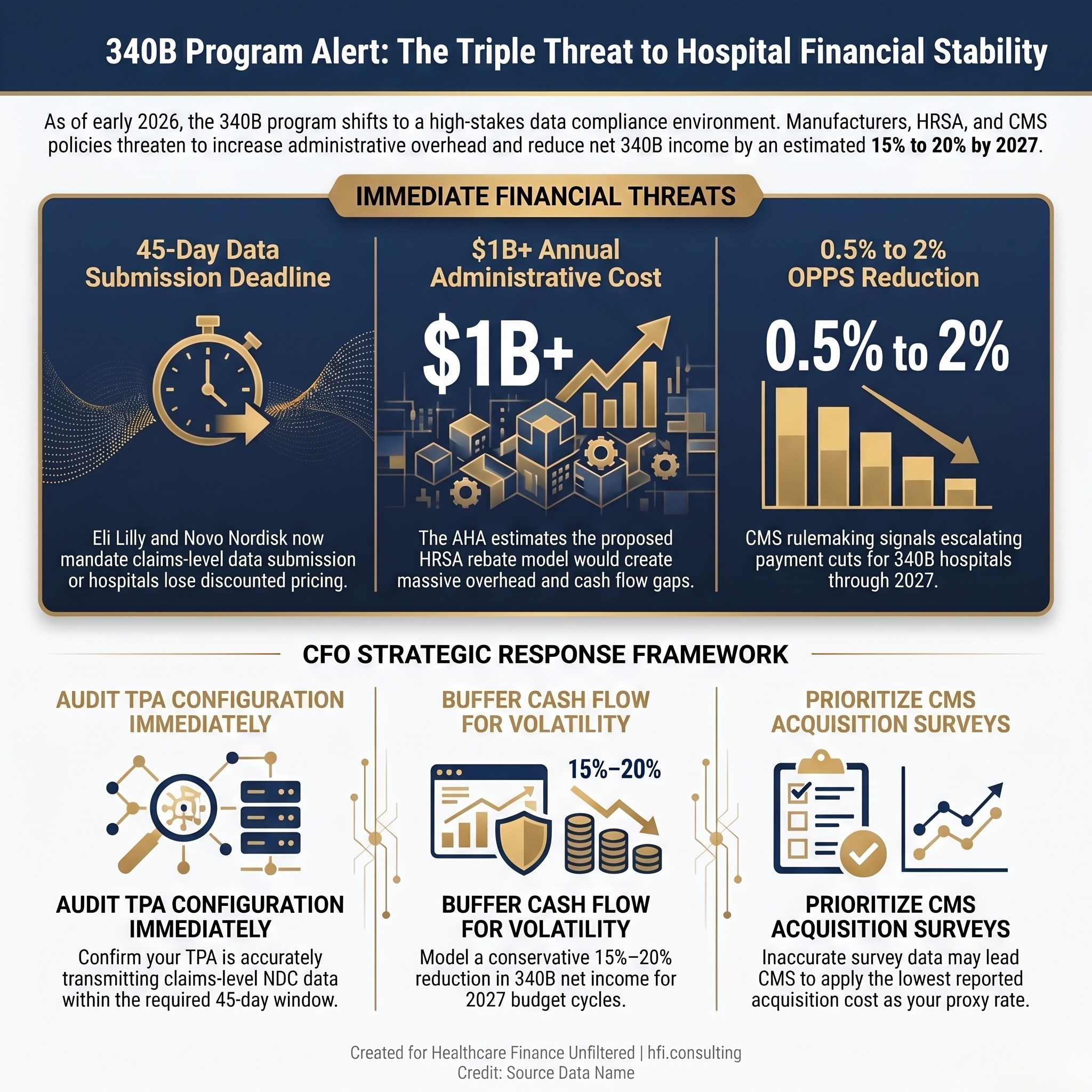

Eli Lilly sent hospitals a letter in late April warning of the "imminent loss" of 340B discounted pricing for any facility that failed to submit claims-level data without further delay. The American Hospital Association has pressed HRSA about this practice for months. As of late April 2026, HRSA has not publicly acted. Meanwhile, the agency is reconsidering a rebate model pilot that a federal court already vacated once, and CMS language in the most recent OPPS Final Rule hints at a payment reduction that could climb from 0.5 percent to 2 percent in future rulemaking. If your 340B program has not been reviewed in the past 90 days, the exposure is building faster than the policy process.

Three-panel stat card showing 340B financial threats: 45-day data ultimatum, $1B+ rebate model cost, and OPPS reduction risk.

The New Battlefield: Data, Not Dispensing

For years, the central 340B controversy was about contract pharmacy. Manufacturers wanted to limit which dispensing sites qualified for program discounts. Courts, state legislatures, and HRSA all weighed in with varying results. As covered in our earlier analysis of the rebate pilot and contract pharmacy litigation, these disputes have been grinding through the regulatory and legal system since 2021.

That battle has not ended. But a second front has opened.

The current pressure is about claims-level data transparency. Eli Lilly and Novo Nordisk have both announced policies requiring hospitals to submit detailed claims data for every 340B dispense within a 45-day window. Non-compliance means loss of front-end discounted pricing. Not a warning. Not a cure period. A direct financial consequence, effective immediately.

The AHA characterized these policies as unlawful and has asked HRSA to prohibit them outright. In its April 2026 letter, the AHA noted that HRSA's inaction stands in stark contrast to the speed with which the agency moved in 2024 when manufacturers first announced rebate policies. Hospitals have shared that the data mandates are creating both operational strain and financial uncertainty, and the longer HRSA stays silent, the harder it becomes to make a compliance decision with confidence.

For finance leaders, HRSA's silence is not a reason to wait. The operational and financial exposure is compounding now.

The HRSA Rebate Model: Vacated But Not Gone

In February 2026, HRSA issued a Request for Information exploring a new 340B rebate model pilot. The AHA responded in April with detailed opposition, arguing that any rebate mechanism is "flawed in both conception and design." For a full background on the original rebate pilot and the lawsuit that stopped it, see our February 340B program update.

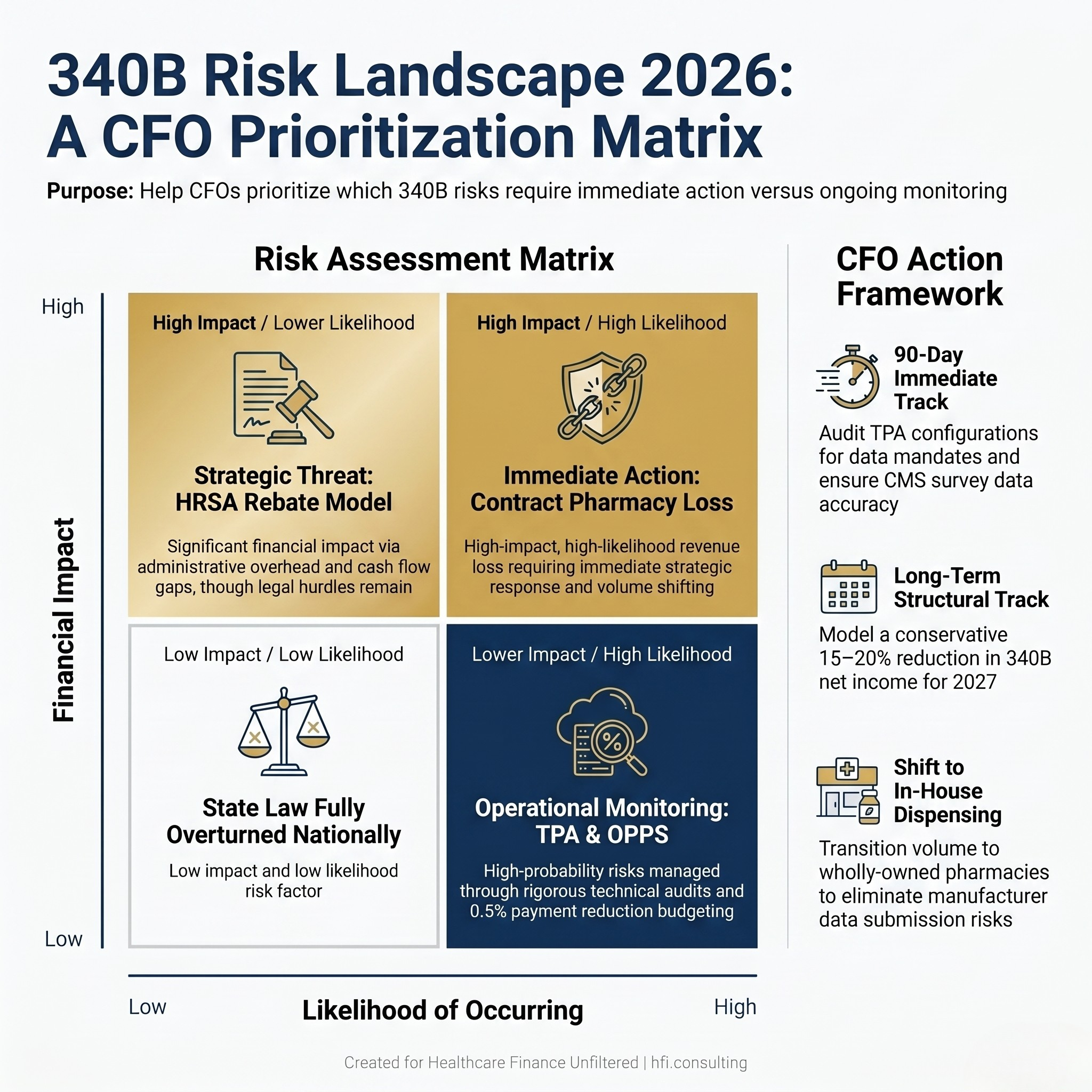

This is not the first iteration. HRSA previously attempted a similar pilot, abandoned following a lawsuit brought by the AHA, the Maine Hospital Association, and four safety-net health systems. The agency is now reconsidering whether it has authority to move forward with a modified structure. A third-party vendor, Second Sight Solutions, is the beneficiary of the proposed mechanism. The AHA estimates the rebate model would cost 340B-eligible hospitals more than one billion dollars annually in new administrative overhead.

The mechanics matter here. Under a rebate model, hospitals would pay full acquisition cost at the point of purchase, then wait for a rebate reimbursement. That cash flow gap is not academic for organizations operating on 2 to 3 percent margins. Even if a new pilot is delayed or blocked by litigation again, the underlying policy pressure will not disappear. Finance leaders should model both scenarios in their 3-to-5-year planning assumptions.

The 90-Day Action Plan

Your most immediate exposure sits in three areas. Address them in this order.

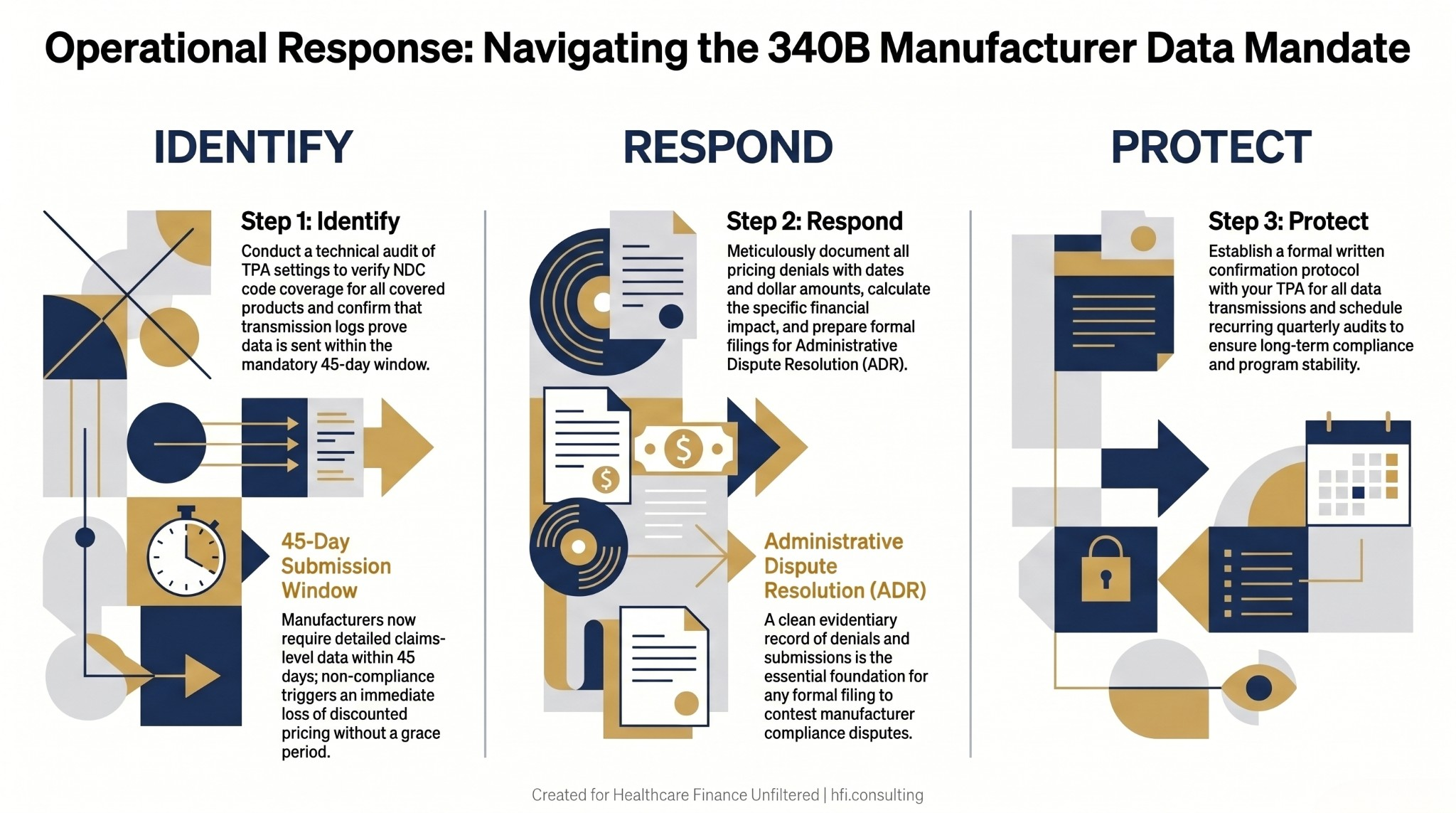

1. Audit Your TPA Configuration for Lilly and Novo Products

The 45-day data submission window is not a future risk. Hospitals have already reported pricing denials from April 2026. Your third-party administrator should be capturing and transmitting claims-level data for Eli Lilly and Novo Nordisk products accurately and on time. If you have not confirmed this with your TPA in writing, that conversation needs to happen this week.

Specifically: verify that your TPA's system settings are pulling the correct NDC codes for covered products, that the transmission is occurring within the 45-day window, and that you have logging in place to document submission dates. If your organization has already experienced pricing denials, document each one meticulously with dates and dollar amounts. Administrative Dispute Resolution is the formal channel for contesting these manufacturer compliance disputes, and a clean evidentiary record is the foundation of any filing.

Three-column process flow diagram showing identify, respond, and protect steps for 340B TPA compliance with manufacturer data mandates.

2. Prioritize the CMS Drug Acquisition Cost Survey

CMS is using the 2026 OPPS Drug Acquisition Cost Survey to inform future payment rate adjustments. The stakes are direct: CMS has signaled it may use the lowest acquisition cost reported by any respondent as the proxy rate for non-responding hospitals.

Treating this survey as a routine compliance task is a financial risk that is easy to underestimate until the 2027 OPPS Final Rule arrives. Finance teams that submit incomplete or inaccurate data may find their 340B acquisition cost assumptions replaced by the floor reported by a different health system with a different contract structure. Assign a named owner for the survey response and build quality review into the submission process before it goes out.

3. Buffer Cash Flow for OPPS Volatility

The $7.8 billion in lump-sum remedy payments issued to 340B hospitals in 2024 are being offset through ongoing OPPS payment reductions. The current reduction rate is 0.5 percent. CMS language in the most recent Final Rule signals the possibility of escalation to 2 percent in future rulemaking. That language matters for treasury and budget planning, not just policy tracking.

Model both scenarios now. A 0.5 percent reduction is manageable for most health systems. A mid-year or 2027 adjustment to 2 percent requires a meaningfully different cash position and budget revision. If your current 2027 projection does not include a 340B OPPS sensitivity analysis, add one.

If your 340B program has not been reviewed against the current manufacturer mandates and regulatory pressures, HFI Consulting can help you assess your exposure and build a planning framework for both near-term compliance and long-term program stability. Visit hfi.consulting to learn more or schedule a conversation.

The Long-Term Framework: Planning for a Structurally Different Program

The 340B program as it was structured five years ago no longer exists in practice. Finance leaders who continue to budget based on historical assumptions are carrying unpriced risk. This is the same dynamic we identified in our analysis of healthcare cost containment strategies: when the operating environment shifts faster than the planning cycle, the variance does not show up until it is too late to absorb cleanly.

Shift from Discount to Rebate Thinking in Your Planning Model

Even without a formal HRSA rebate model, manufacturers are effectively forcing rebate-style workflows through data submission policies. The operational difference is significant: instead of receiving a discount automatically at the point of purchase, your team must now proactively capture, validate, and transmit claims data to maintain pricing access your organization was previously entitled to by statute.

Plan for a permanent increase in administrative overhead tied to this data exchange. Whether that means additional TPA capability, in-house staffing, or a technology investment depends on your volume and product mix. What it cannot mean is assuming the old process still works without verification. In my work with health system finance teams navigating high-volume drug programs, the most consistent gap I encounter is not awareness of these mandates. It is the assumption that the TPA is handling it without anyone actively confirming that it is.

Model a 15 to 20 Percent Reduction in 340B Net Income for 2027

The combination of OPPS payment reductions, potential rebate model administrative costs, and manufacturer-imposed compliance overhead represents a material reduction in 340B net contribution. A conservative planning posture applies a 15 to 20 percent reduction to 340B net income projections for fiscal 2027 and beyond.

If the regulatory environment stabilizes, your budget variance is positive and you have room to reallocate. If deterioration continues, you have not overexposed your operating assumptions. This is not pessimism. It is the same scenario planning discipline that belongs in any high-uncertainty revenue stream.

Dual-column planning framework comparing optimistic and conservative 340B budget scenarios across five financial variables.

Do Not Rely on State Laws to Protect Contract Pharmacy

The 4th Circuit upheld a preliminary injunction blocking West Virginia's 340B contract pharmacy protection law in March 2026 and denied en banc review in April. Mississippi's law was separately upheld by the 5th Circuit. The legal landscape across states is inconsistent and continues to shift.

Finance leaders who have built state-level contract pharmacy protections into their planning assumptions should revisit those assumptions now. The more durable strategy is shifting volume to wholly-owned retail pharmacies where your organization controls both the dispensing data and the pricing relationship. This eliminates the manufacturer data policy issue for in-house dispensing and removes reliance on legal protections that may not hold.

Run a Worst-Case Contract Pharmacy Scenario

Model your 340B net income as if contract pharmacy is fully unavailable. If that scenario produces a material impact on your overall margin, you have a concentration risk that belongs in your strategic planning conversation, not only in your pharmacy operations review.

2x2 risk matrix plotting four 340B financial risks by likelihood and financial impact to guide CFO prioritization.

What This Means for Payer Organizations

For payer organizations, the 340B pressure plays out differently. As manufacturers restrict contract pharmacy access and layer on data compliance requirements, cost-of-care dynamics for high-volume drug categories will shift. PBM contracts that rely heavily on 340B spread pricing are worth reviewing in this environment. If 340B providers are carrying more administrative overhead, those costs will eventually show up in rate negotiations.

From my time at Florida Blue Medicare, data flow disruptions between health systems and payers rarely appeared as a single, identifiable event. They materialized as quiet cost creep in categories where the pricing assumptions had not been revisited since the last contracting cycle. The instinct is to wait for regulatory resolution before updating models. The more useful posture is to model the range of outcomes now and identify which produce cost exposure outside your tolerance.

The Bottom Line for Finance Leaders

The 340B situation requires two parallel tracks. The 90-day track addresses immediate compliance exposure: TPA configuration audit, CMS survey quality, and cash flow buffering for OPPS volatility. The long-term track addresses structural planning assumptions: rebate workflow overhead, contract pharmacy risk quantification, and a conservative posture on 340B net income.

Neither track is optional. Compliance failures produce immediate financial impact. Strategic planning failures show up in 2027, when the rulemaking and court outcomes still pending today have settled into your rate structure and your budget has no room to absorb them.

The AHA is actively advocating for 340B hospitals on both the manufacturer data policies and the HRSA rebate model. But regulatory and legal timelines are uncertain. Finance leaders cannot build their planning cycle around an outcome that may take 12 to 18 months to resolve. Build the framework now, and update it as the landscape changes.

Are you modeling 340B as a stable revenue stream in your current budget? The frameworks above are a starting point. For a more tailored review of your program's exposure and a scenario planning approach built for your specific drug mix and pharmacy structure, visit hfi.consulting.

P.S. How is your organization currently handling the Eli Lilly and Novo Nordisk data submission requirements? Are you relying entirely on your TPA, building in-house review capability, or taking another approach? Hit reply and let me know. I read every response.