Medicare GLP-1 Bridge 2026: The CFO Financial Planning Guide for Payer and Provider Leaders

CMS's $50/month GLP-1 demonstration launches July 2026. Here's what health plan and hospital finance leaders need to model now.

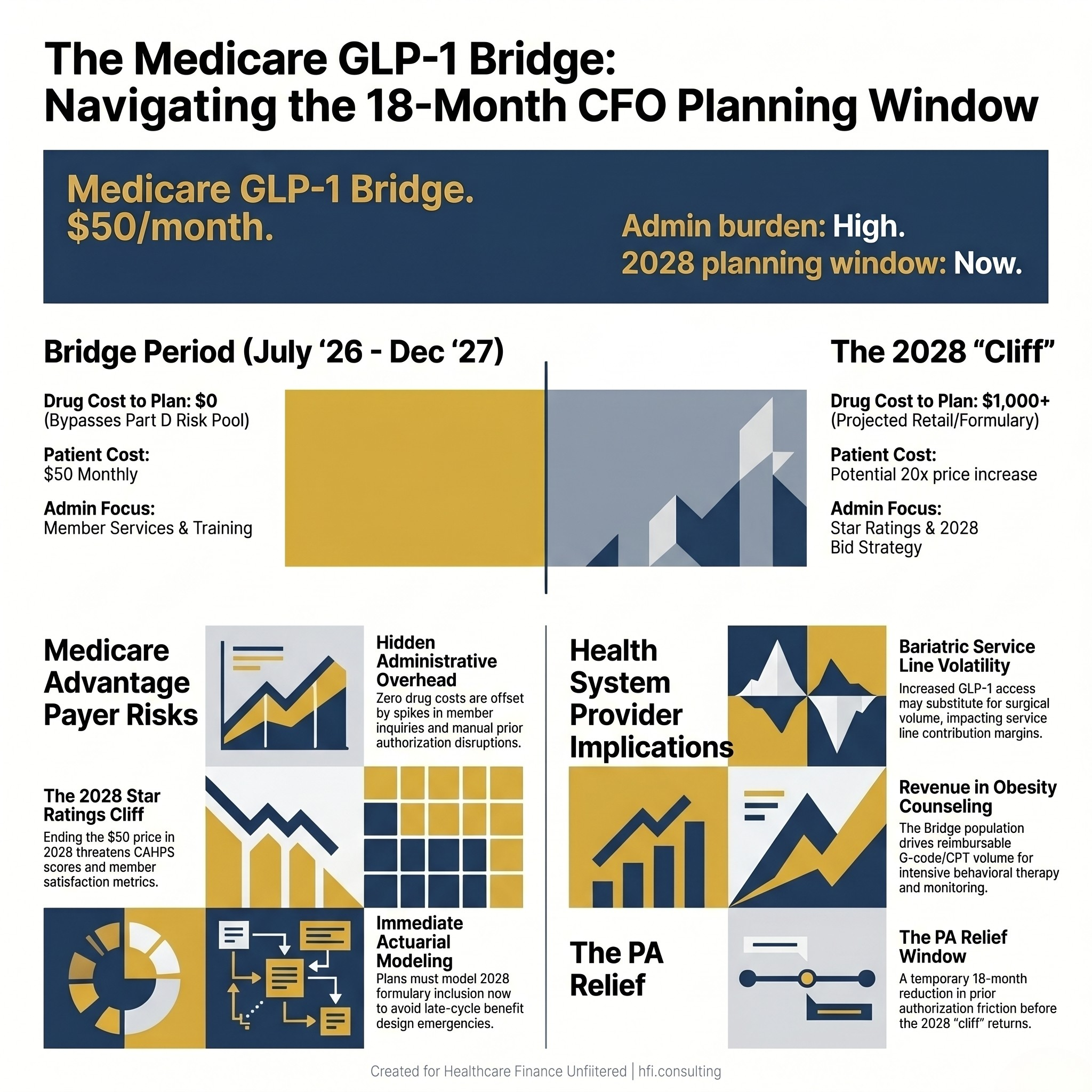

CMS just announced that starting July 1, Medicare beneficiaries with Part D coverage can access GLP-1 medications for $50 per month through December 2027. The drug cost for health plans: zero. The operational and strategic exposure on both the payer and provider sides is not.

This is a demonstration program, not a permanent benefit. That distinction is exactly what makes the financial planning window so narrow.

Split-panel stat card showing CMS GLP-1 Bridge program dates and the dual financial exposure for payer and provider CFOs.

What the Medicare GLP-1 Bridge Is and What It Is Not

The Medicare GLP-1 Bridge is a time-limited CMS demonstration program, operating under the Secretary's authority to test new care delivery approaches. Starting July 1, 2026, eligible Medicare Part D enrollees can access specific GLP-1 medications at $50 per month through December 31, 2027.

The critical structural detail for finance leaders: CMS is using a centralized claims processor to pay pharmacies directly. This program bypasses the standard Part D benefit administered by Medicare Advantage plans entirely. Health plans are not adjudicating these claims. They are not carrying the drug cost in their Part D risk pool.

What CMS is covering includes Wegovy, Zepbound, and Foundayo. What it does not cover is the clinical infrastructure required to support patients on these medications: office visits, lifestyle counseling, monitoring, and the downstream management of adherence and side effects. That cost lands on providers and plans in different ways depending on how their contracts are structured.

The other structural fact worth flagging: this program is a demonstration. There is no permanent coverage authorization in place. The 18 months from July 2026 through December 2027 are a test period, not a policy commitment. Finance leaders on both sides need to plan accordingly.

Why Payer CFOs Are Underestimating This Program

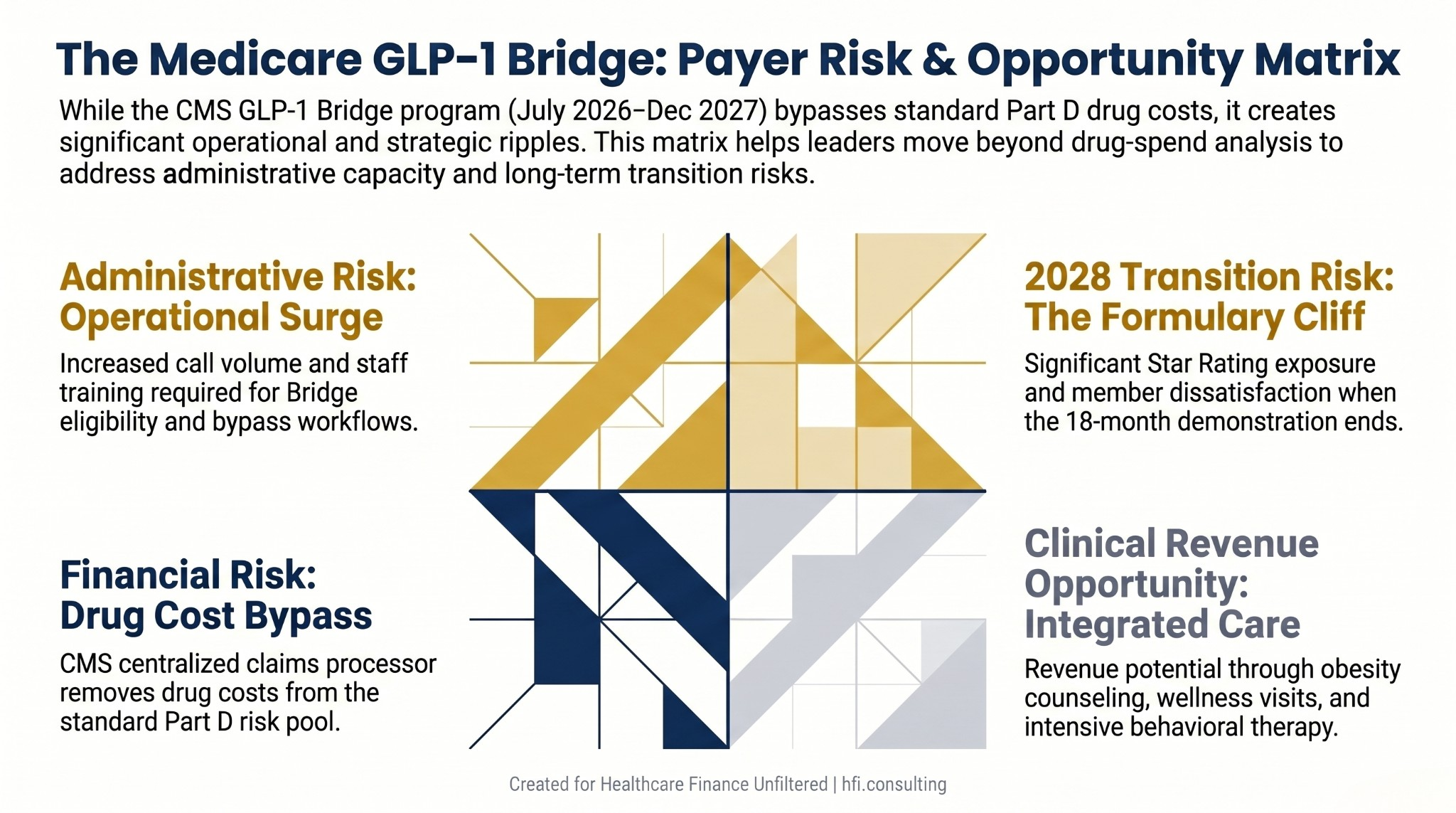

The zero drug cost creates a blind spot. Health plan CFOs who see the bypass structure and conclude there is no financial exposure are missing the four places where this program creates real budget pressure.

Member services volume. When a member sees a $50 GLP-1 program in a news headline, the first call goes to the plan. Not to CMS. Not to the pharmacy. Your call center will absorb the inquiry volume, the eligibility questions, and the confusion about why the standard formulary benefit looks different from the Bridge benefit. This is a staff training and capacity problem, and it will arrive fast.

Prior authorization workflow disruption. Plans have existing PA processes for weight-loss medications. The Bridge bypasses those processes for covered drugs. Finance leaders need to model the cost of re-training staff, updating member-facing materials, and fielding the appeals that will come when members expect the Bridge price on a drug that isn't covered under it.

Star Ratings exposure at the cliff. If the program ends December 31, 2027 without a permanent coverage solution, thousands of members will lose access to a $50 drug that costs $1,000 or more at retail. Member satisfaction scores, CAHPS results, and Star Ratings all carry momentum from quarter to quarter. A coverage cliff in early 2028 lands squarely in your 2028 plan year performance metrics. The time to model that scenario is now.

2028 formulary positioning. The 18-month demonstration period is also a data collection effort. CMS is watching whether lower-cost GLP-1 access reduces downstream cardiovascular events, hospitalizations, and total cost of care. If the data supports positive outcomes, the pressure on MA plans to include these drugs in standard formularies for 2028 will be significant. Plans that wait until 2027 to start the actuarial modeling will be late to the benefit design conversation.

From my time on the payer side at Florida Blue Medicare, one consistent pattern held across every new program rollout: the plans that built their member service capacity before launch managed the first 90 days at a fraction of the cost of plans that reacted to volume after it hit. The GLP-1 Bridge launches July 1. The operational readiness window is closing.

Four-quadrant risk matrix showing GLP-1 Bridge financial, administrative, clinical, and transition risk for Medicare Advantage plan CFOs.

What the Bridge Means for Provider CFOs

Hospital and health system finance leaders are looking at a different set of implications. The zero-cost drug structure removes one of the most common patient-side barriers to GLP-1 initiation. That access expansion does two things simultaneously: it increases the volume of patients seeking obesity management services, and it puts real pressure on your bariatric service line's contribution margin story.

Bariatric surgery volume and GLP-1 substitution. Surgical weight loss and medical weight management are not interchangeable, but patients and payers increasingly treat them as a sequence, not a binary choice. The Bridge will accelerate GLP-1 initiation among Medicare patients who previously could not afford the medication. Some will achieve outcomes that eliminate bariatric surgery from their care path. Finance leaders need to model the downside scenario for bariatric volume without assuming it. The data is not settled.

Wellness and monitoring visit volume. The Bridge requires what CMS describes as lifestyle support. For providers with integrated primary care or weight management programs, this is a revenue opportunity. Medicare reimburses obesity counseling visits (G0447, G0473) and intensive behavioral therapy. The Bridge population is a direct referral source for these services. The finance question is whether your care delivery infrastructure can absorb the volume increase at a margin that justifies the investment.

The prior authorization relief window. GLP-1 approvals for Medicare patients have historically required significant documentation for medical necessity. The Bridge program's centralized adjudication removes that friction for covered drugs during the demonstration period. Revenue cycle teams that have been managing GLP-1 prior auth denials should anticipate a shift in workload during the Bridge period, and should document current denial and appeal rates as a baseline for what returns when the program ends.

For health systems operating in high-Medicare-density markets, the Bridge program effectively functions as a 18-month pilot for medical weight management at scale. The systems that use this period to build clinical protocols, billing workflows, and contribution margin benchmarks will be better positioned for permanent coverage when it arrives. The ones that treat it as a temporary disruption will have to rebuild that infrastructure later.

I covered the coverage expansion implications of GLP-1 decisions for a younger Medicare-adjacent population in an earlier piece on GLP-1 coverage decisions and the financial planning considerations for finance leaders. The Bridge program accelerates many of the same downstream dynamics for the Medicare population directly.

The 2028 Cliff: Why 18 Months Is Not Enough Time to Plan Slowly

The Bridge ends December 31, 2027. That is 18 months from launch. It is not 18 months of planning time. By the time plans finalize their 2028 benefit designs, complete actuarial filings, and submit bids to CMS, the Bridge will already be in its final quarter of operation.

The scenario finance leaders need to model is not complicated: what happens to your member satisfaction scores, your Star Ratings, and your network relationships when patients who have been on a $50 GLP-1 for 18 months suddenly face either $1,000+ monthly retail costs or plan formulary access that their physician hasn't navigated before?

Plans that build a glide path now, including formulary modeling, manufacturer contracting strategy, and member communication timelines, will absorb the transition at lower cost than plans that wait for permanent CMS guidance. Permanent guidance may not arrive before the benefit design window closes.

For provider CFOs, the 2028 cliff signals something different: the potential return of prior authorization friction and patient cost barriers that suppress GLP-1 adherence. If you have built clinical protocols and care team capacity around the Bridge population, model the volume drop scenario for 2028 and build it into your service line financial projections.

The CY 2027 MA Final Rule already signaled CMS's direction on MA formulary design and supplemental benefits. The planning framework for MA finance leaders provides useful context for how the Bridge fits into the broader MA policy trajectory.

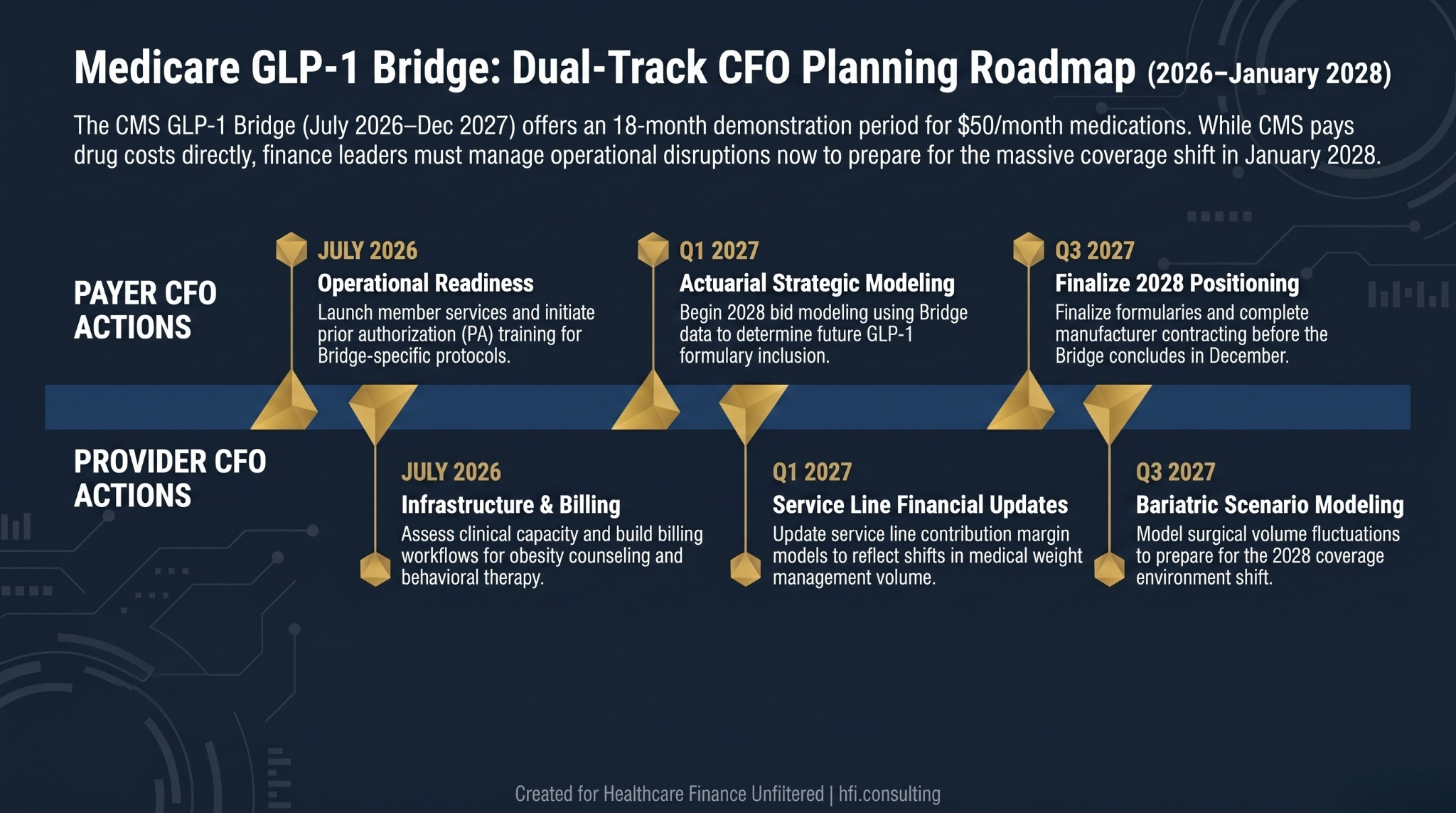

What CFOs Should Do in the Next 60 Days

For payer CFOs:

Quantify member services call volume projection. Use your current GLP-1 PA inquiry rate as a baseline and apply a multiplier for Bridge enrollment volume. Staff and train before July 1, not after.

Pull your current Part D formulary and map it against Bridge-covered drugs. Identify where members may seek non-Bridge GLP-1s that do carry plan cost, and prepare your PA team for that distinction.

Start the 2028 actuarial modeling for GLP-1 formulary inclusion. The data CMS collects during the demonstration will inform your competitive positioning. Do not wait for that data to begin your own scenario analysis.

Engage your Star Ratings team on the transition risk. Member experience metrics that drop in Q1 2028 will affect plan year 2028 performance. Build the scenario into your risk register now.

For provider CFOs:

Assess your obesity management infrastructure against projected demand. Medicare beneficiaries who can access GLP-1s at $50 per month will seek clinical support for initiation, monitoring, and lifestyle integration. Is your capacity built for that volume?

Review your bariatric service line contribution margin model and add a GLP-1 substitution scenario. The range of outcomes is wide. Quantify both the downside and the case where surgical volume is unchanged because GLP-1 patients still progress to surgery.

Build a billing workflow for obesity management and intensive behavioral therapy visits. These are reimbursable services with existing CPT and G-code infrastructure. The Bridge population creates a direct referral pathway.

Document current GLP-1 prior auth denial and appeal rates as a baseline. When the Bridge ends, this is what your revenue cycle team returns to managing.

If your organization is evaluating integrated care models or payvider arrangements that include weight management, the CFO financial playbook for provider-sponsored health plans covers the structural considerations for organizations building risk-bearing capability around this population.

Dual-track planning timeline for payer and provider CFOs showing GLP-1 Bridge action steps from July 2026 through the January 2028 coverage transition.

The Demonstration Is the Data

CMS is calling this a Bridge because it is designed to span the gap between current access and a permanent coverage decision. The 18 months of program data will inform whether GLP-1 access reduces hospitalizations, cardiovascular events, and total Medicare cost of care at the population level.

That data will also inform every benefit design, formulary, and network conversation through 2028 and beyond. Finance leaders who treat the Bridge as a temporary administrative disruption are reading it wrong.

The CFOs who use this period to build clinical infrastructure, model actuarial scenarios, and develop operational protocols will enter 2028 with real data and built capacity. The ones who wait will be negotiating vendor contracts and building member communications under deadline pressure, in a coverage environment that may change rapidly.

The Bridge is 18 months. Your planning window is now.

If your organization is working through the actuarial or operational implications of the GLP-1 Bridge on your MA plan or provider service line strategy, HFI Consulting works with payer and provider finance teams on exactly these questions. Visit hfi.consulting to connect.

The 2028 Coverage Cliff Is a Finance Decision, Not a Policy One

Permanent GLP-1 coverage for Medicare beneficiaries is not guaranteed. CMS has made clear this is a demonstration. The legislative and regulatory pathway to permanent inclusion in Part D or MA supplemental benefits involves timelines that may not resolve before your 2028 benefit design is finalized.

Plan CFOs who wait for regulatory certainty before modeling GLP-1 coverage will be making 2028 benefit design decisions with 2027 data in a compressed timeline. That is a worse position than modeling multiple scenarios now with the information available.

The question is not whether to include GLP-1s in your 2028 plan. The question is what your financial model says under each scenario: full formulary inclusion at standard Part D cost-sharing, narrow formulary inclusion with step therapy, or exclusion with a communication strategy for the member population that used the Bridge. Build the model now so the decision is a business judgment, not a timeline emergency.

P.S. Payer and provider finance leaders: are you already modeling the 2028 formulary and service line implications of the GLP-1 Bridge, or is this still in the "watch and wait" category at your organization? Hit reply and tell me where your team stands. I'm tracking what's actually happening in the field and plan to follow up on this topic as the July 1 launch approaches.

Healthcare Finance Unfiltered is published by Rachel Barksdale, MHA, CHFP. Rachel's background spans provider finance at UF Health Jacksonville and Ascension, and payer operations at Florida Blue Medicare. HFI Consulting works with health systems and health plans on margin improvement, revenue cycle strategy, and finance infrastructure.